Wei Li – Global Chief Investment Strategist of BlackRock investment institute, together with Alex Brazier – Deputy Head, Kurt Reiman – Senior Strategist for North America, and Nicholas Fawcett – Macro research all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Favoring fixed income: We don’t see major central bank rate cuts this year, so we prefer to earn income in short-term bonds, high-grade credit and agency mortgage-backed securities.

Market backdrop: U.S. stocks rose and Treasury yields were mostly steady. U.S. Q4 GDP was resilient but declining consumer spending suggests growth is slowing quickly.

Week ahead: The Fed and the European Central Bank anchor policy decisions this week. We see them hiking and holding rates higher for longer than markets expect

Major central banks are set to hike policy rates again this week and keep them higher, counter to market views for cuts this year. We see this disconnect resolving and favoring higher rates. That’s because we think inflation will fall fast but stay above target. Rates staying high plus the political tussle over raising the U.S. borrowing limit are market risks. We prefer to earn income and like short-term government bonds, high-grade credit and mortgage-backed securities.

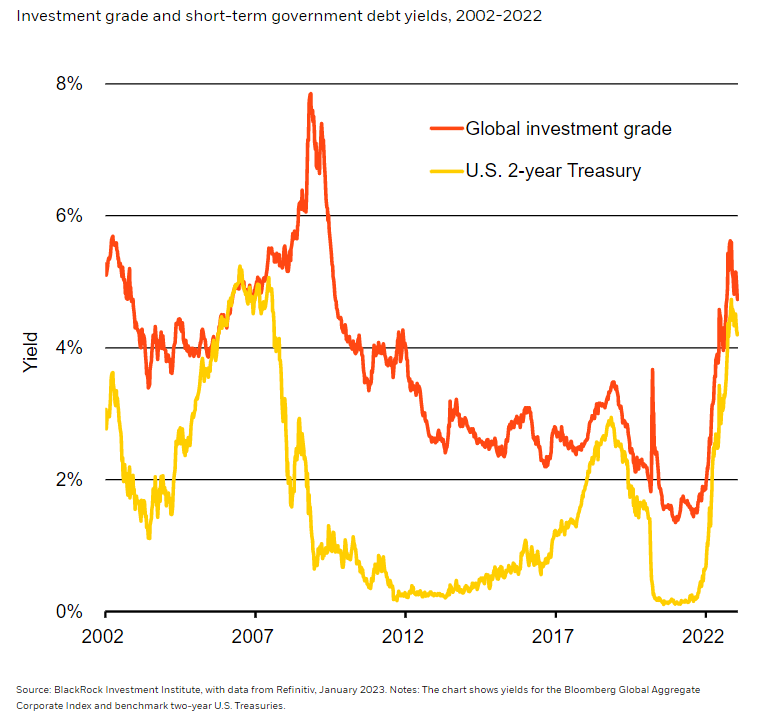

Yield is back

Income is finally back in fixed income thanks to higher yields and coupons. Short-term government bonds and investment grade (IG) credit now offer some of the highest yields in the last two decades. See the chart. We prefer to earn income right now from these high-quality fixed income assets as rates rise and stay high. Fixed income’s appeal remains intact the longer central banks keep rates near their peak. The lack of duration – or the sensitivity of bond prices to interest rates – in short-term paper also helps preserve income even if yields rise anew. Global IG credit offers high-grade, liquid income – and we think the strong balance sheets of high-quality companies that refinanced debt at lower rates can weather the mild recession we see ahead. We also like agency mortgage-backed securities (MBS) to diversify income.

We see major central banks on a path to overtighten policy because they’re worried about the persistence of underlying core inflation, excluding food and energy prices. PCE data in the U.S. confirmed the outlook for core inflation hasn’t improved, and it’s tracking to be well above policy targets into 2024. Core services inflation is proving sticky even as goods prices fall. That stickiness is tied to wage pressures in the labor market that we see remaining tight. We think central banks will want more evidence that core inflation and wage pressures are sustainably subsiding before they declare victory on inflation and think about easing policy. This will take a long time – and is unlikely to happen this year, in our view.

This week, the Fed and ECB are set to push rates further up again. We see the Fed hiking 0.25% and the ECB raising 0.5%, with more hikes likely to follow. Then we see them keeping rates high. But markets are pricing rate cuts in 2023 even as both central banks insist they will stay the course. That disconnect needs to be resolved, and we think it will be in favor of higher rates as inflation persists above central banks’ 2% target. Rates staying high is one reason we prefer earning income with shorter duration paper.

Term premium’s return

Another reason is term premium – the compensation investors demand for holding long-term government bonds. We see investors seeking more term premium with higher inflation and other near-term risks on the horizon. Political pressure on the Bank of Japan to change its yield curve control policy is likely to ramp up with inflation running at a four-decade high. The risk: a global spillover from higher Japanese government bond yields to global yields. We think moving away from yield curve control would be like a move away from a currency peg – even tweaks could lead to abrupt market dislocations.

Risks over raising the U.S. borrowing cap are also in focus now after the U.S. hit its debt ceiling this month – this reinforces our view that investors will once again demand term premium. Negotiations are likely to go down to the wire this summer and could be as fraught as 2011, when S&P Global downgraded the U.S. triple-A credit rating. We ultimately expect a resolution. If a U.S. default were to occur, it would likely be technical in nature, meaning the U.S. would prioritize debt payments over other obligations. We would expect only a temporary rise in selected Treasury bill yields as the default date nears. Another debt ceiling impasse could also pressure risk assets as in past episodes – this keeps us cautious on U.S. equities.

Our bottom line

Rates staying high and the political tussle over the U.S. debt ceiling are market risks. We take a granular view on fixed income at this juncture. We tactically like short-term government bonds, high-grade credit and agency mortgage-backed securities for attractive income.

Market backdrop

U.S. stocks climbed and bond yields were mostly steady, with European and emerging market shares outperforming the U.S. on investor inflows. U.S. GDP was resilient in the last quarter of 2022. Consumer spending helped prop up growth, but we see signs of weakness beneath the surface. The U.S. PCE data showed consumer spending was losing momentum at the end of the year and suggests that growth is slowing more quickly than we expected.

The Fed and the European Central Bank anchor this week’s central bank decisions. We see them both pushing up rates further and pushing back against market expectations for rate cuts. The U.S. services PMI and payrolls data will give the latest view on recession risks. We think further resilience in activity and the labor market could embolden the Fed.

Week Ahead

Jan. 31: Euro area flash Q4 GDP; U.S. consumer confidence

Feb. 1: Fed policy decision; U.S. job openings; euro area inflation

Feb. 2: European Central Bank, Bank of England policy decisions

Feb. 3: U.S. payrolls, U.S. ISM services PMI; China services PMI

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 30th January, 2023 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.