Wei Li, Global Chief Investment Strategist of the BlackRock Investment Institute, together with Alex Brazier, Deputy Head Vivek Paul, Head of Portfolio Research and Kurt Reiman, Senior Strategist for North America all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Recession Looms: The recession we see from Federal Reserve rate hikes eclipses any impact from U.S. midterm elections. We stay underweight developed market (DM) stocks.

Market backdrop: Yields rose and stocks rallied off lows as markets mulled the scope of central bank rate hikes amid a “whatever it takes” campaign to curb high inflation.

Week ahead: Markets are pricing another 0.75% rate hike by the European Central Bank this week. U.S. PCE inflation will be in focus before the Fed’s meeting next week.

Equities usually do well after U.S. midterms. Why? Gridlock is common and prevents policy change that could spook stocks. We don’t see that past playbook working this time due to the recession we expect from the Fed ratcheting up rates. Gridlock dims any prospect of fiscal stimulus that only works at cross-purposes with monetary policy in the new regime – take the UK. We stay underweight DM stocks but see the politics of higher rates taking over from the politics of inflation.

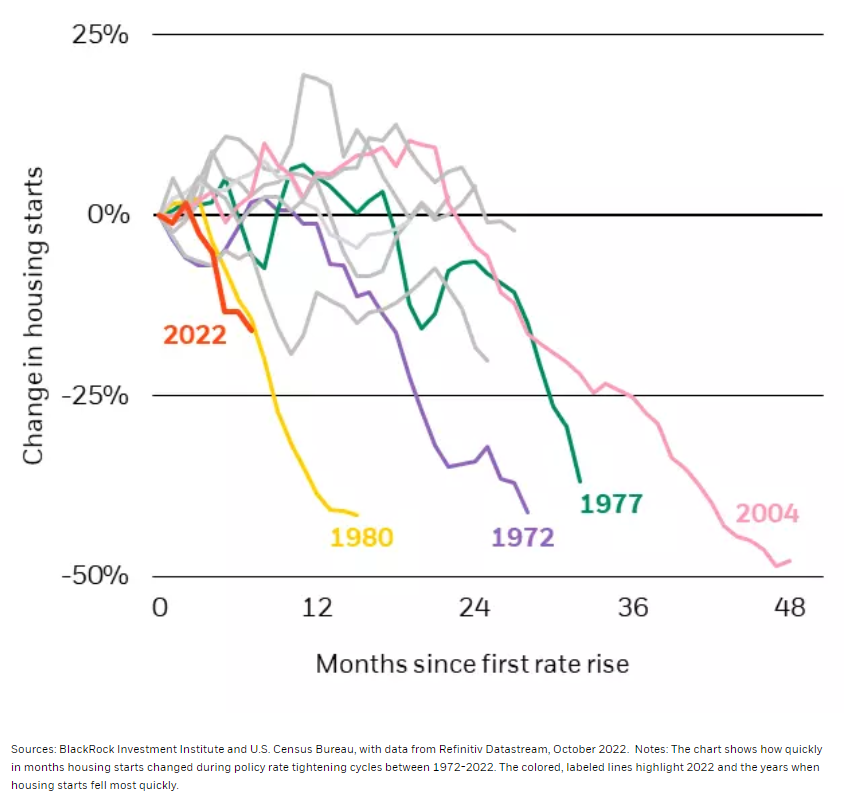

Housing Stops

U.S. housing starts during policy rate tightening cycles, 1972-2022

We see a bigger problem for stocks than any potential positives from the midterm election outcome: a looming recession. We have argued how central banks rushing to hike policy rates to get inflation back to target would need to crush interest rate-sensitive parts of the economy first. That’s because higher inflation is driven by production constraints. Recession will pressure other sectors in time, but we’ re already seeing damage in important rate-sensitive sectors like housing. As mortgage rates soar along with the Fed’s aggressive rate hikes, the number of new housing starts is falling quickly. The slide in housing starts this year (see orange line in the chart above) is already steeper than past mega Fed rate-hike cycles such as in the 1970s and early 1980s – as well as the unwind of the mid-2000s U.S. housing boom (other colored lines).

We’ve said the playbook from the Great Moderation, a four-decade period of steady growth and inflation, won’t work in this new regime of heightened macro volatility. Recession outweighs factors in previous U.S. midterm elections that were seen as positive for stocks, such as resulting policy gridlock. Gridlock typically meant lower odds of change that could affect stocks. Equities also have yet to fully reflect recession and earnings risk, we think. We’re not chasing bear market rebounds.

Midterms hold no sway

The midterms won’t sway our view. Recession matters more and any resulting fiscal stimulus can only work at cross purposes when inflation and debt levels are high, and rates are rising. We’ve seen how it can threaten a fragile equilibrium and revive bond vigilantes. Case in point: the UK. The episode of historic long-term gilt volatility shows what can happen when governments try to respond to high inflation with unfunded fiscal spending. We’ve moved to neutral on UK gilts from underweight as perceptions of fiscal credibility have improved after the U-turn on the fiscal mini-budget. We think the Bank of England will have to hike rates less than we assumed immediately after the plan. Still, political turmoil and the resignation of Prime Minister Liz Truss, warrant caution. Fiscal policy can’t save the day, we think – it’s a recession foretold. Production constraints mean the only way to get inflation down to target would be to curb the level of activity to what the economy can comfortably produce now. We don’t think fiscal stimulus would result in stronger growth but just higher interest rates and debt servicing costs.

We see political focus increasingly shifting to the economy. We expect inflation to come down, but stay above target – and recession will still hit. We then think the politics of inflation could switch to the politics of higher interest rates. We see the politics of rates creeping into the politicization of everything with more voices beginning to decry the aggressive rise in interest rates that is causing recession. We see the Fed stopping its hikes amid the economic damage and pressure to ease up on tightening, but price pressures will persist. That’s why we think it will eventually have to live with some inflation.

Our bottom line

We’re underweight DM equities. We see rising rates causing recession as inflation persists. The Fed is responding to the politics of inflation, or the pressure to tame it, we think. We see the Fed pausing but only after the economic damage of rate rises is clear. All this outweighs any expected boost for stocks after the midterms, in our view. We also think any resulting fiscal stimulus would only work against monetary policy in this new regime. We eventually see the politics of rates overtaking the politics of inflation as political focus sharpens on the economy into the 2024 elections.

Market backdrop

U.S. and German bond yields hit new multi-year highs as markets brace for more central bank rate hikes. That has kept equities pinned near two-year lows despite occasional bear market rallies. Major central banks are expected to deliver big rate rises at upcoming meetings as they pursue a “whatever it takes” approach to curb inflation, starting with the European Central Bank next week. We expect them to carry on until the economic damage caused becomes clear.

We expect the European Central Bank to stick to an aggressive tightening path and raise rates on Thursday. The Fed’s preferred metric for inflation – the PCE for – comes out on Friday, a week before markets see it lifting policy rates 0.75% to 3.75-4.0%. Manufacturing September data around the world could also give early signs of the recessions we expect.

Week Ahead

Oct. 24: Global flash PMIs

Oct. 25: U.S. consumer confidence

Oct. 27: European Central Bank policy decision; U.S. GDP

Oct. 28: U.S. PCE; Bank of Japan policy decision

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 25th October, 2022 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Investor Information Document (KIID), which may be obtained from MeDirect Bank (Malta) plc.