Jean Bovin – Head of BlackRock Investment Institute, together with Wei Li – Global Chief Investment Strategist, Alex Brazier – Deputy Head, and Kurt Reiman – Senior Strategist for North America all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

More volatility ahead: We think the U.S. debt limit showdown will spark renewed volatility in markets. That risk reinforces why we stay invested and cautious by going up in quality.

Market backdrop: Stocks were flat last week after U.S. data confirmed core inflation staying high. We think sticky inflation makes Federal Reserve rate cuts later this year unlikely.

Week ahead: U.S. industrial production and business survey data due this week should gauge how the Fed’s rate hikes have hurt industrial and business activity.

Negotiations to lift the U.S. debt ceiling are heating up. The Treasury hit the $31.4 trillion “ceiling,” or cap on how much debt it can issue, in January. It may be unable to pay its bills in early June. Even if a deal is struck before then, we expect the debt showdown to stoke market volatility. The bigger story on a six- to 12-month horizon: We think central banks must damage growth to cool inflation in the new regime. We stay invested but cautious as a result, and favor quality assets.

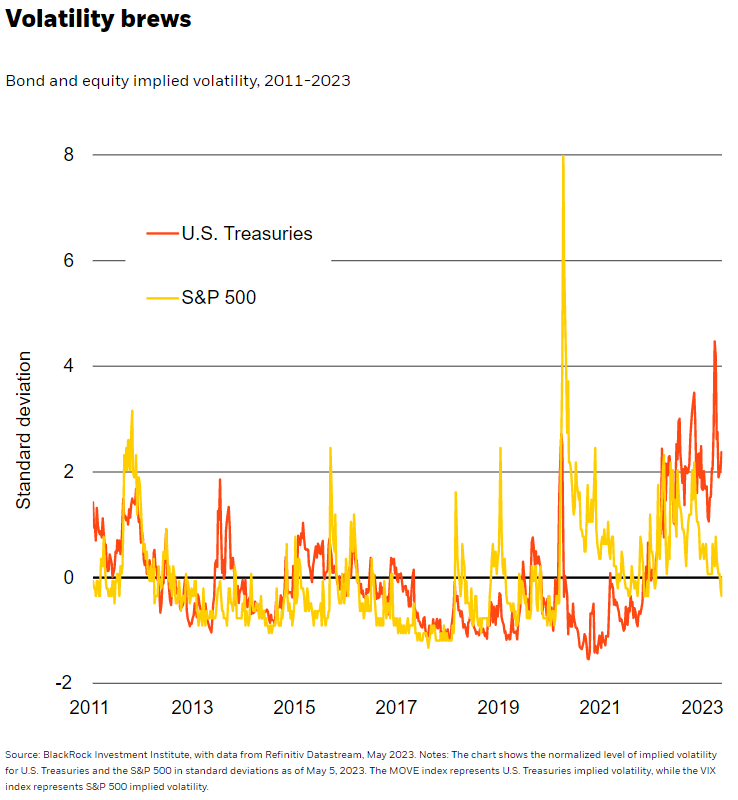

A delay in lifting the U.S. debt limit, as well as the euro area debt crisis, spurred a bout of market volatility in 2011. See the chart. U.S. Treasury bill yields seen as the most vulnerable to late payment jumped, and the S&P 500 fell about 17% between July and August 2011. Policy rates were near zero back then, deflation risks were emerging and the Fed balance sheet was expanding. All that provided a cushion. The backdrop is very different today. Bond market volatility has already surpassed the 2011 level (dark orange line) as markets grapple with central banks’ trade-off: either live with some inflation or crush economic activity. Equity volatility is more muted (yellow line). Yet we don’t think stocks have been immune – just a few major tech stocks account for almost all S&P 500 returns this year. Our conclusion: Brace for higher volatility because of the combined effect of debt ceiling concerns and financial cracks from rate hikes.

Invested but cautious

It’s uncertain when exactly the U.S. Treasury will run out of funds to meet its financial obligations – known as the “X date.” Treasury Secretary Janet Yellen has warned that could happen as soon as early June. Conversations about a last-minute deal to raise or suspend the debt ceiling, meaning eliminate it for a brief period, are ongoing as Democrats have so far rebuffed Republicans’ push for spending cuts and other concessions. The Treasury risks a technical default when it temporarily fails to make its bond payments if policymakers don’t strike a deal in time. The Treasury may prioritize paying bondholders over others, but it’s unclear if the Treasury can do so: There is no precedent, and the Treasury lacks the legal authority. Yet there is precedent for credit rating agencies trimming the U.S. top-notch credit rating like S&P did in 2011 – even if a technical default doesn’t happen. That could cause investors to demand more compensation for holding U.S. assets amid higher risk.

Yields for some Treasury bills maturing just after the X date have already started to rise, but risk assets have yet to fully react. Yields for the affected Treasury bills could march higher, and volatility may keep cycling through assets if the debt ceiling is repeatedly suspended.

We stay invested but cautious against this backdrop. We had already been going up in quality and focused on building resilient portfolios as the Fed rapidly hiked rates. We see opportunities to earn attractive income in short-term debt if yields rise more. Investors who don’t need to quickly sell assets can earn attractive income during the debt showdown, in our view, by holding on to at-risk Treasury bills until they mature. Persistent inflation makes inflation-linked bonds attractive, too. Notably, demand for gold has picked up via exchange-traded funds and foreign exchange reserve managers.

Developed market equities remain the bulk of portfolio allocations, even as we underweight them slightly in the short term. We prefer emerging market (EM) stocks in the short term as they benefit from China’s economic restart, EM central banks nearing the end of their hiking cycles and a broadly weaker U.S. dollar. We could consider leaning more into equities overall if debt ceiling volatility and recession create a sharp fall in equity prices.

Our bottom line

The debt ceiling showdown is set to increase the volatility in financial markets that has defined the new regime. Any selloff may cause risk assets to better price in the economic damage we expect from interest rate hikes. We’re ready to shift our views on a six- to 12-month horizon to take advantage of opportunities that may appear.

Market backdrop

Global stocks were largely unchanged last week and bond yields stayed within their range since mid-March. U.S. CPI data showed that core services inflation, excluding shelter, is easing, but core goods prices surprisingly ticked higher. Core inflation still doesn’t look on track to settle near the Fed’s 2% target, making Fed rate cuts this year unlikely, in our view. The Bank of England hiked policy rates to 4.5% as it carries on with its fight against stubborn inflation while growth stagnates.

We’re watching industrial production and business survey data in the U.S. to gauge the damage to activity as higher interest rates tighten financial conditions and cause financial cracks, as seen in bank turmoil. We’re also looking for signs of a sustained rise in Japan inflation that we think may eventually spur a change in ultra-loose policy – and bond volatility.

Week Ahead

May 16: U.S. industrial production, retail sales; Germany ZEW economic sentiment

May 18: U.S. Philly Fed Index

May 19: Japan CPI

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 15th May, 2023 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.