Wei Li – Global Chief Investment Strategist of BlackRock Investment Institute together with Christopher Kaminker – Head of Sustainable Research and Analytics, Chris Weber – Head of Climate Research and Jessica Thye – Sustainable Research and Analytics all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Transition themes: We track the low-carbon transition to identify investment opportunities and risks. We’re eyeing three related themes at the annual UN climate conference.

Market backdrop: U.S. stocks last week hit their highest level of the year, and U.S. 10-year Treasury yields fell lower. We expect near-term volatility and rising yields in the long term.

Week ahead: U.S. payrolls data this week will show if jobs growth is still slowing. We think the U.S. can only sustain a fraction of recent job growth without inflation resurging.

The low-carbon transition is one of five mega forces, or structural shifts, we track for investment risks and opportunities. We’re following three investment themes at the UN climate conference (COP28) in Dubai. First, climate resilience – society’s ability to prepare for and withstand climate risks – is an underappreciated theme, we think. Second, we eye progress on unlocking climate finance in emerging markets. Third, we watch for new policy plans that could shape the transition path.

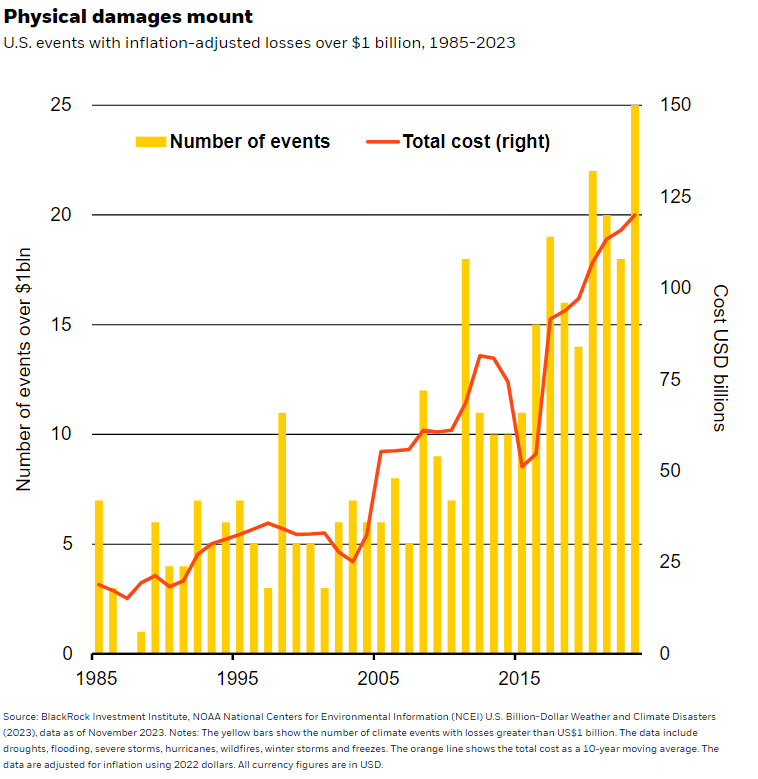

We highlight climate resilience first because it is an emerging theme not yet fully appreciated by investors. We think companies that create and adopt products and services that boost climate resilience will become a more widely recognized opportunity. Why? The number of U.S. climate events with damages above $1 billion has steadily climbed over the past roughly four decades. See the yellow bars in the chart. As such risks increase, we are seeing early signs of growing demand for climate resilience solutions. Case in point: Demand for home air-filtration appliances in the northeastern U.S. spiked during the Canadian wildfires in early 2023. Emerging markets (EMs) are set to bear some of these risks more acutely given greater exposure to physical climate damage. Yet they face difficulties in raising financing needed for the transition. We think this also offers an investment opportunity and is key to tracking the transition’s overall speed and shape.

The IPCC has reported persistent increases in average annual temperatures, precipitation and sea levels. The frequency and intensity of acute weather events, such as extreme heat and widespread floods, has also increased. We see policy and regulation driving the growth of the market for resilience products. Any COP28 agreement on a global plan for climate adaption could spur new policy. Some incentives to invest in resilience are already in place, including $50 billion from the Infrastructure Investment and Jobs Act and over $20 billion from the Inflation Reduction Act. Other support comes from building code updates in the U.S. and Europe explicitly focusing on improving climate resilience.

EM financing gap

We are closely watching policy developments that could unlock investment opportunities in EMs. They play a pivotal role in the global reduction in carbon emissions, in our view. Why? We estimate EM will account for over half of energy demand and carbon emissions by 2050. Yet transition-related investment in EMs will likely be lower than in DMs due to a higher cost of capital from greater perceived investment risk, and greater exposure to physical climate damage. We think closing the financing gap would require significant public sector reforms and private sector innovation, resulting in greater “blending” of public and private capital. We think successful reforms could see low-carbon investment in EMs rise on average by a further $200 billion a year – or $4 trillion overall – above our base view of a major increase in investment between 2030-2050.

Evolving energy use

We think COP28 will also provide further details about policies that are likely to influence how the mix of energy use evolves – and the investment opportunities. We see policy, technology and consumer preferences driving an accelerating shift to renewable energy in DMs. 2023 has seen record growth of about 50-70% for renewable energy, according to the International Energy Agency. Countries at COP28 look poised to agree to a goal to triple capacity by 2030. We think further policy support may make the goal achievable – and yet the S&P global clean energy index is down about 28% year to date, LSEG data show. Even with this growth in renewables, meeting global energy demand will rely on traditional energy for some time – and we think it can outperform at times, especially when there are supply-demand mismatches.

Our bottom line

We monitor COP28 for signs of growth in transition-related investment themes. We see granular opportunities in public companies that produce climate resilience solutions across sectors. Solutions like early monitoring systems to predict floods or retrofitting buildings to better withstand extreme weather make the technology and industrial sectors stand out to us. And we think reforms could make it easier for private market players to fill the EM financing gap.

Market backdrop

Last week, the S&P 500 closed at its highest level this year after rising roughly 9% in November – the largest monthly gain in 16 months. The U.S. 10-year Treasury yield slid lower to near 4.30%, with its November drop of more than 50 basis points marking the largest monthly fall in 12 years. We expect further volatility for bonds in the near term as policy rates peak. We think long-term yields will rise again as investors demand more compensation for the risk of holding long-term bonds.

The U.S. payrolls report for November is in focus this week. We are looking for signs that job growth is slowing further as the post-pandemic normalization runs its course. Structural labor shortages as the U.S. population ages means the economy will only be able to sustain a fraction of recent job growth without stoking inflation again, in our view.

Week Ahead

Dec. 5: Japan CPI; China PMI

Dec. 7: China trade data

Dec. 8: U.S. payrolls; University of Michigan consumer sentiment survey

Dec. 9: China CPI and PPI

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 4th December, 2023 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.