Liontrust GF High Yield Bond Fund is manufactured by Liontrust Fund Partners LLP and represented in Malta by MeDirect Bank (Malta) plc.

Market review

The global high yield Q3 market return of -1.0% (US dollar terms) masks two six-week periods marked by ‘risk on’ then ‘risk off’. At the start of the quarter, indeed from 1st July, markets began to rally based mainly on the idea of a ‘dovish pivot’ from the US Federal Reserve. The tumultuous high yield markets in the first half of the year had mainly been about the impact of rising interest rates/ monetary tightening on market liquidity. Rates markets had then begun to reflect a view of the world where inflation was under control, growth was slowing and central banks would be cutting by the end of next year. Risk markets liked the idea of future looser monetary policy.

Yet stubborn inflation data ruined the party, and, from the middle of August, high yield sold off as the ten-year US treasury gradually moved to 4% and higher. By mid-August, the global high yield market had produced a quarter-to-date return of 6.8% in US dollars, only for that to be lost (and some more) by the end of the quarter. A game of two halves. Equity markets had followed a similar path – the correlation between all types of assets, or lack of diversification, remains clear.

Those sectors that are perceived to be longer duration, e.g. telecoms and real estate, were the best performing sectors in the first six week period, and amongst the worst in the second. The high yield market, for now, is like a yoyo under the control of the US rates curve. CCCs have again outperformed, albeit marginally, suggesting to me that the high yield market continues to be more concerned about duration than any recession coming down the line.

Fund review

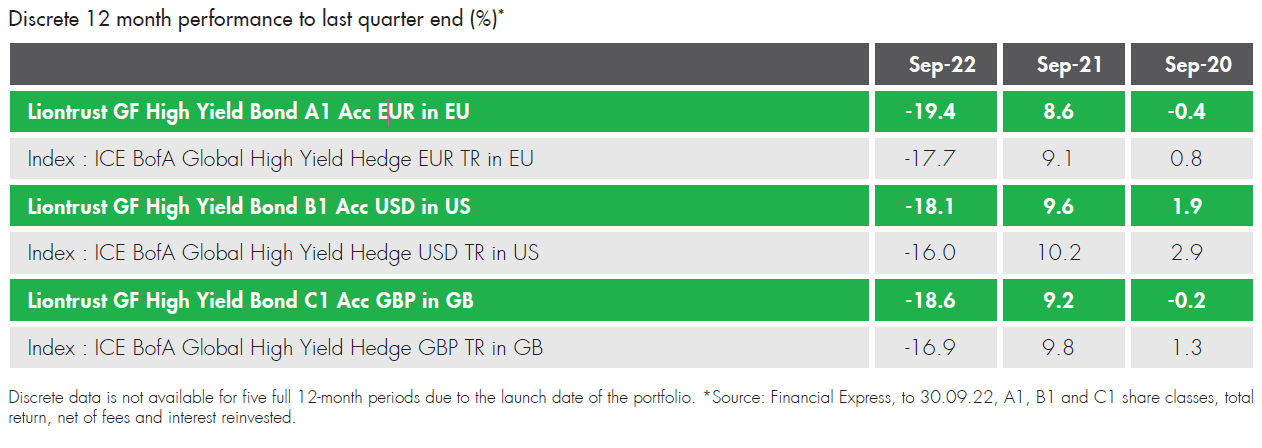

Over the quarter, the Liontrust GF High Yield Bond Fund (A1, accumulation class, total return in euros) produced a return of -1.5% versus the ICE BAML Global High Yield index’s (euro hedged) -1.7%*.

In our last quarterly update, we wrote at length about the Fund’s holdings in the real estate sector. At the beginning of this period, Heimstaden announced a bond tender and CPI Property bought bonds back in the secondary market. Both of these holdings held up relatively well during the sell-off in the latter half of this period. Castellum has not yet bought back any of its bonds and its bond underperformed in the risk-off period. Between mid-August and the end of the period, the real estate sector cost the Fund around 30bps relative to index. However, over the full quarter the sector made a significant positive contribution to absolute and relative performance.

The insurance sector was a significant detractor. Each holding we have in the sector is a sterling denominated bond (hedged) and the material under-performance versus index occurred in the aftermath of the UK Chancellor’s ‘mini budget’ and the impact this had on UK government bonds. Two of our three holdings in the sector are issued by companies with investment grade ratings in the life insurance sector. A2 rated Rothesay bonds now yield 11.3% and we have conviction in the long-term prospects for this business. In total, the Fund has around 10% in sterling-dominated bonds.

Our preference towards higher quality bonds and less cyclical sectors skews us towards a slightly longer duration in our credit selection than our index and, likely, our peers. At the start of the year, we had interest rate futures offsetting some of this duration, but, with increasingly higher rates, we removed these hedges.

The Fund therefore feels somewhat higher beta to this rates-driven risk on/risk off dynamic. The bonds that were the strongest performers up until mid-August were amongst the weakest performers in the latter part. Chief amongst these was, for example, the likes of the UK’s Virgin Media, a business we deem to have strong credit fundamentals, or Millicom, a quality Latin American telecom with North European ownership and governance. When the market was rallying on this idea of a Fed pivot, the Fund was first in its UK peer group in July. By mid-August, we had all but closed the underperformance versus index in the year-to-date. However, in the latter half of the period, we gave most of this back.

Outlook

We are making lending decisions based on long-term fundamentals and value, not on short-term market sentiment. The Fund has a yield of around 11.5% for sterling investors (8.9% euro) and an average rating of BB-. Our ability to generate returns in line with this yield is entirely down to the underlying credit quality of the holdings and their ability to refinance in the future. The rates-driven volatility that sees Virgin Media as more volatile than many cyclical CCCs in our view is mark-to-market noise.

If the new issue market remains all but closed, then refinancing risk will increase as a risk to the asset class. In 2023, the European currency high yield market has a small €20bn of maturities, so time is on our side (there is ~€50bn of maturing in 2024). Even this year has seen €22bn of issuance to date (versus €150bn in 2021). Our conviction remains in the higher quality part of the high yield market and believe long terms returns will vindicate this.

Liontrust Key risks & Disclaimers:

Past performance is not a guide to future performance. Do remember that the value of an investment and the income generated from them can fall as well as rise and is not guaranteed, therefore, you may not get back the amount originally invested and potentially risk total loss of capital. The issue of units/shares in Liontrust Funds may be subject to an initial charge, which will have an impact on the realisable value of the investment, particularly in the short term. Investments should always be considered as long term.

Investment in the GF High Yield Bond Fund involves foreign currencies and may be subject to fluctuations in value due to movements in exchange rates. The value of fixed income securities will fall if the issuer is unable to repay its debt or has its credit rating reduced. Generally, the higher the perceived credit risk of the issuer, the higher the rate of interest. Bond markets may be subject to reduced liquidity. The Fund may invest in emerging markets/soft currencies and in financial derivative instruments, both of which may have the effect of increasing volatility.

Issued by Liontrust Fund Partners LLP (2 Savoy Court, London WC2R 0EZ), authorised and regulated in the UK by the Financial Conduct Authority (FRN 518165) to undertake regulated investment business.

This document should not be construed as advice for investment in any product or security mentioned, an offer to buy or sell units/shares of Funds mentioned, or a solicitation to purchase securities in any company or investment product. Examples of stocks are provided for general information only to demonstrate our investment philosophy. It contains information and analysis that is believed to be accurate at the time of publication, but is subject to change without notice. Whilst care has been taken in compiling the content of this document, no representation or warranty, express or implied, is made by Liontrust as to its accuracy or completeness, including for external sources (which may have been used) which have not been verified. It should not be copied, faxed, reproduced, divulged or distributed, in whole or in part, without the express written consent of Liontrust. Always research your own investments and (if you are not a professional or a financial adviser) consult suitability with a regulated financial adviser before investing.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from Liontrust Fund Partners LLP. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest should always be based upon the details contained in the Prospectus and Key Investor Information Document (KIID), which may be obtained from MeDirect Bank (Malta) plc.