Jean Boivin, Head of the BlackRock Investment Institute together with Wei Li, Global Chief Investment Strategist, Alex Brazier, Deputy Head, Vivek Paul, Deputy Head of Portfolio Research and Scott Thiel, Chief Fixed Income Strategist, all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points:

A new regime – We see a new era of volatile inflation and growth sweeping aside a period of moderation. We downgrade equities and upgrade credit in this new regime.

Market backdrop – U.S. jobs data last Friday reinforced the supply shock causing persistent inflation. Yields resumed their rise as markets priced higher odds of rate hikes.

Week ahead – U.S. inflation is in laser focus this week. Persistently high monthly inflation rates could cement the case for a 75-basis point Fed rate hike later this month.

We think the Great Moderation is over. What’s replaced this era of steady growth and inflation? A new regime of increased macro volatility and higher risk premia. Central banks appear set on reining in inflation by crushing growth. We cut most developed market (DM) equities to a tactical underweight as a result, while we lean into credit. In strategic portfolios, we still prefer stocks over bonds. Why? We see policymakers ultimately living with some inflation.

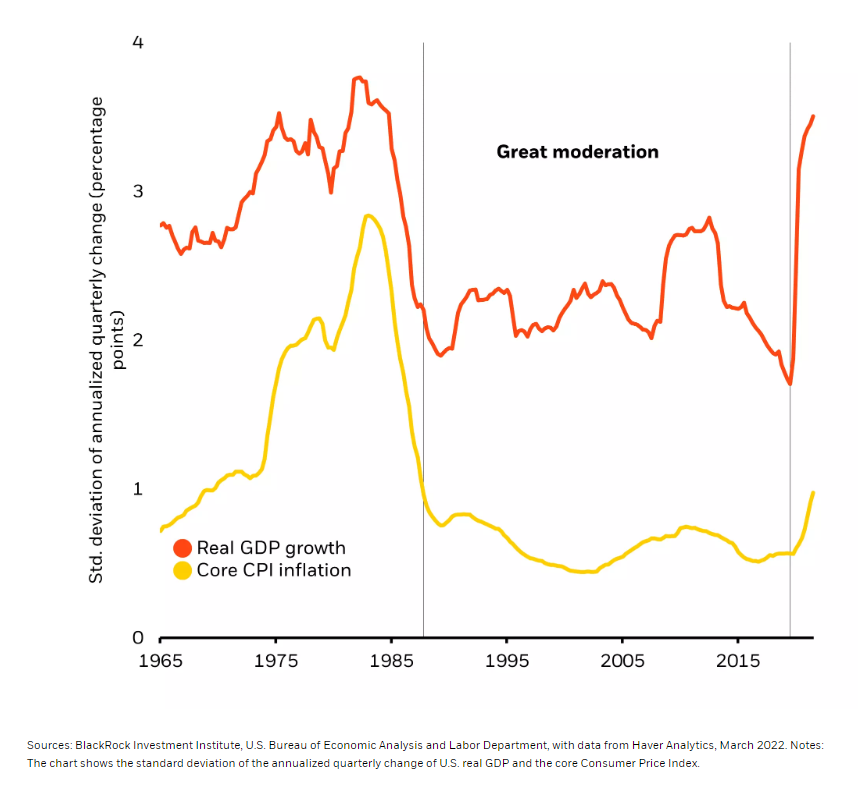

The end of the Great Moderation

Volatility of U.S. GDP growth and core inflation

What happened to the Great Moderation anyway? It got flipped upside down. Key features of the era were steadily expanding production capacity and demand shocks. Central banks could easily nudge spending by cutting or hiking rates. But now that’s flipped (see chart). Why? Production constraints. The pandemic triggered a huge sectoral shift in spending from services to goods as well as labor shortages. The restart and war in Ukraine added an energy crunch. These are tough problems to solve. A pile-up of global debt to buffer the Covid shock limits the wiggle room of central banks – and makes it more tempting to live with inflation. And the politicization of everything means policy debates are oversimplified when nuanced solutions are needed. All this makes trade-offs between growth and inflation harder, we believe, and leads to worse outcomes.

Three investment themes guide us in new era

Three investment themes guide us in the new era. First – Bracing for volatility. Macro volatility drives market volatility. The end of the Great Moderation is now causing fierce market gyrations. In this structurally more volatile environment, investors will demand higher risk premia, or compensation for holding both stocks and bonds. What do we think this means? Both tactical and strategic allocations have to adapt more quickly. Portfolios have to get more granular at the sector level. Traditional 60/40 stock-bond portfolios and models won’t work as well anymore. And “buying the dip” is unlikely to be as effective as it was before. The inertia behind those kind of behavioral biases must be overcome, we believe.

Our second theme is as relevant as ever – Living with inflation. Right now, we think the Fed has boxed itself in by responding to political pressures to rein in inflation. In other words, the politics of inflation rule. This implies downside risks to growth and company earnings. Eventually, the damage to growth and jobs from fighting inflation will become obvious, in our view, and central banks will live with higher inflation. Production constraints rooted in the pandemic and exacerbated by the war in Ukraine have led to 40-year highs in inflation. The spike in commodities is a prime example of how these factors have collided into an inflation explosion. And we see an era of structurally higher commodities prices ahead.

The bumpy transition to net-zero emissions also fuels the new regime’s volatility. This makes for our third theme – Positioning for net zero. We believe markets haven’t fully priced in fast-changing societal preferences for sustainability and technological innovation. We like “already-green” companies and carbon-intensive ones with credible transition plans.

What this means for investments

More frequent tactical changes – like spotting a turning point for stocks when markets eye a dovish pivot by central banks. In the short term, we’ve cut DM equities except Japanese stocks as central banks appear set to overtighten policy. We upgrade credit to overweight as part of an up-in-quality adjustment to portfolios. We still like inflation-linked bonds, and now prefer the euro area. And we like UK gilts as we see the Bank of England turning dovish.

Strategically, we believe our stance is positioned for the new regime. We prefer equities over bonds in the long run as yields rise and inflation trends higher. We think central banks will live with higher inflation, pause and then change course on their rate rises– a boon for stocks. Private markets are not immune in this new regime of higher volatility but opportunities exist for selective investors, especially in private credit.

Market backdrop

Last week’s U.S. jobs update underscores the ongoing supply shock that will cause higher inflation to be more persistent. Non-farm payrolls were a little higher than expected, allowing for downward revisions in earlier months. But the participation rate – capturing those in or looking for work – fell on the month. Bond yields resumed their rise as markets priced in higher chances that the Fed will raise rates by 75-basis points at its policy meeting later this month.

U.S. CPI will be key this week. A continuation of the pattern of persistently high monthly inflation rates would likely cement the case for a 75-basis point Fed hike later this month. We see the Fed continuing with hikes up to restrictive levels by the end of the year. In China, second quarter GDP will help gauge the economic impact of strict Covid lockdowns earlier this year.

Week Ahead

July 12: Germany ZEW survey

July 13: U.S. CPI inflation

July 15: U.S. University of Michigan Sentiment, China GDP

July 11-18: China total social financing

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 11th July, 2022 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Investor Information Document (KIID), which may be obtained from MeDirect Bank (Malta) plc.