Jean Boivin, Head of the BlackRock Investment Institute together with Wei Li, Global Chief Investment Strategist, Alex Brazier, Deputy Head of the BlackRock Investment Institute and Nicholas Fawcett, Macro Research all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points:

No wage-price spiral: We don’t see a wage-price spiral. Companies are actually paying less in labor per unit of output, we find. We think wages can rise more without adding to inflation.

Market backdrop: The S&P 500 plunged to new 2022 lows last week. We remain overweight equities in the inflationary backdrop but acknowledge mounting challenges.

Week ahead: The Fed is set to raise its policy rate by 0.5% this week in an attempt to rein in inflation. We think the eventual sum total of rates hikes will be historically low.

Inflation and hawkish central bank talk have spooked investors and led to bond losses not seen since the U.S. wages are growing at the fastest clip since the 1980s. Is this the start of a “wage-price spiral” – a vicious cycle of companies funding higher pay by raising prices, causing employees to ask for even higher wages? We don’t think so. In reality, we find companies are paying less in labor costs per unit of output than before the pandemic thanks to higher productivity and prices. We believe wages can rise further without adding to inflation – and help normalize the labor market.

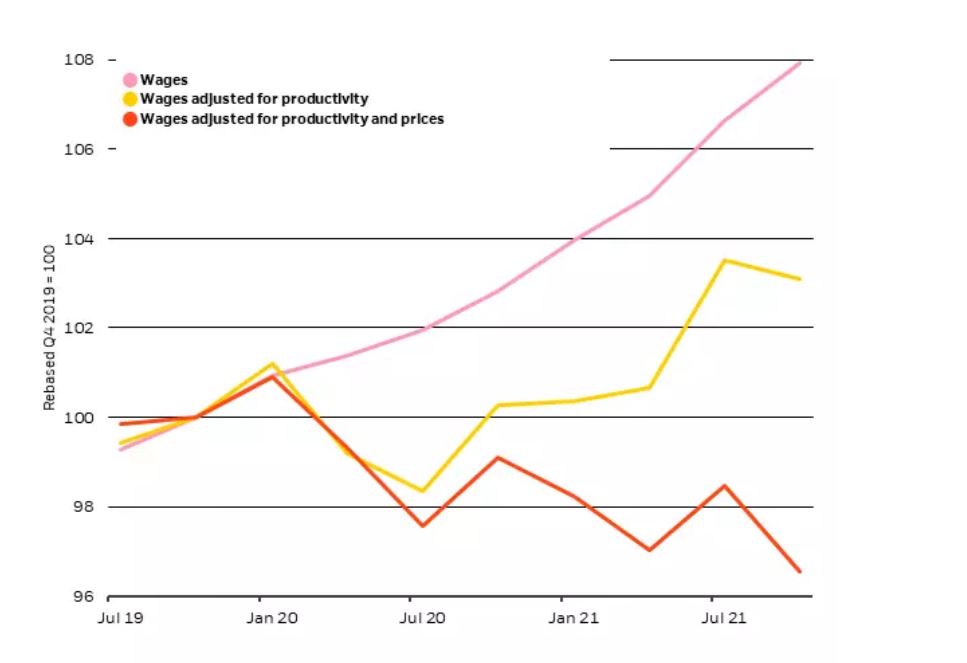

Real wages have room to rise

U.S. labor costs, 2019-2021

Past performance is not a reliable indicator of current or future results. Indexes are unmanaged and not subject to fees. It is not possible to invest directly in an index. Sources: BlackRock Investment Institute, with data from Haver Analytics. Notes: The chart shows the level of U.S. private wages and salaries (in pink) from the U.S. employment cost index measure of hourly labor costs. The yellow line shows this measure of wages adjusted for productivity, by dividing by the level of output per hour. The red line shows this productivity-adjusted series adjusted for inflation by dividing by the U.S. personal consumption expenditure headline price index.

Wages measured by the Employment Cost Index jumped 5% last year – the fastest pace since the 1980s (pink line in the chart). Some argue this is evidence of an overheating job market and a precursor to spikes in consumer prices. But higher wages don’t necessarily mean higher inflation. What matters for companies is the real unit labor cost: how much a company pays workers to produce a unit of output relative to that unit’s selling price. U.S. workers are 4.5% more productive than before the pandemic, according to Bureau of Labor Statistics data. Wages have actually fallen since then (the red line), after adjusting for those productivity gains (the yellow line) and higher prices. Our conclusion: Wages have room to rise as they catch up with productivity and price gains, rather than drive more inflation pressure.

Not overheating

How about other ostensible signs of an overheating labor market? The U.S. unemployment rate is at a pre-pandemic low. The ratio of vacancies to unemployed is at the highest level on record. We believe this is caused by a labor market still healing from the pandemic, rather than excessive demand for labor. People are quitting at record rates to improve their compensation (the “Great Renegotiation”), and the unemployed are reluctant to fill job openings. This means ballooning vacancies are a sign of people switching jobs, rather than new jobs being created. At the same time, many have left the workforce for health, lifestyle or other reasons (the “Great Resignation”). Labor force participation – the share of the working-age population with a job or actively looking for work – is 1 percentage point below its pre-pandemic level. This is very much a U.S. problem. In Europe, the quit rate is lower, and furlough programs helped participation recover quickly.

How to solve for the reduced labor supply in the U.S.? Further wage growth could entice the unemployed to fill job openings and entice employees to stay in their current jobs, rather than quit in search of better pay. Vacancies could come down and employment could rise by 1.5 million, or 1% of the U.S. work force, we estimate. And unemployment may not fall much further if higher wages induce those who left the workforce during the pandemic to return.

The labor market dynamics reinforce our belief that we are in a world shaped by supply, not excess demand. We see inflation cooling from 40-year highs as the economy heals. But we’re are not going back to the “lowflation” years before the pandemic, we believe, amid ongoing supply constraints. As a result, we expect the Fed to ultimately raise rates to a neutral level that neither stimulates nor decreases economic activity. Raising rates beyond neutral to try to squeeze out inflation even further would come at too high a cost to growth and employment, in our view. The result: We see the sum total of rate hikes at a historically low level given inflation. This reinforces our underweight to government bonds and overweight to equities. We favor developed market equities over emerging market stocks, with a preference for the U.S. and Japan over Europe. The reason: We see the energy shock emanating from Russia’s invasion of Ukraine hitting Europe hard.

Bottom line

We do not see a wage-price spiral building. Private sector wages in the U.S. have increased, but what matters for companies is that real unit labor cost have actually fallen thanks in part to productivity gains. This means there’s still room for wages to grow. Higher wages could help the U.S. labor market recover from pandemic-related worker shortages by encouraging people to return to the workforce or stay put in their jobs, rather than shopping around for more compensation.

Market backdrop

The S&P 500 plunged to new 2022 lows last week to clock its worst month since the pandemic’s sell-off in March 2020. We believe stocks can do well in the inflationary backdrop – but acknowledge other mounting challenges such as the energy shock and China’s growth slowdown. The U.S. economy unexpectedly contracted in the first quarter, but consumer and business spending showed strength. We believe the economic restart is still in full swing. See our Macro insights.

The Fed is likely to raise its policy rate by 0.5% this week to 0.75-1%, while the Bank of England is poised to hike another 0.25%. Fed Chair Jerome Powell may reiterate his tough talk talk on reining in inflation. We think the Fed will quickly lift policy rates through 2022 but ultimately will re-assess before going beyond neutral levels that destroy growth and jobs.

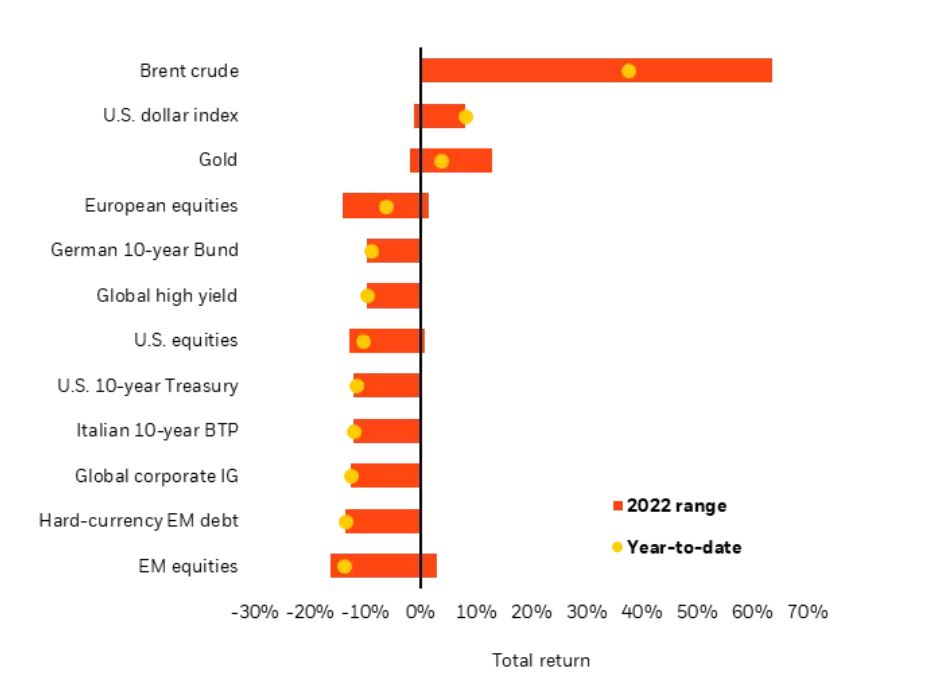

Past performance is not a reliable indicator of current or future results. Indexes are unmanaged and do not account for fees. It is not possible to invest directly in an index. Sources: BlackRock Investment Institute, with data from Refinitiv Datastream as of April 28, 2022. Notes: The two ends of the bars show the lowest and highest returns at any point this year to date, and the dots represent current year-to-date returns. Emerging market (EM), high yield and global corporate investment grade (IG) returns are denominated in U.S. dollars, and the rest in local currencies. Indexes or prices used are: spot Brent crude, ICE U.S. Dollar Index (DXY), spot gold, MSCI Emerging Markets Index, MSCI Europe Index, Refinitiv Datastream 10-year benchmark government bond index (U.S., Germany and Italy), Bank of America Merrill Lynch Global High Yield Index, J.P. Morgan EMBI Index, Bank of America Merrill Lynch Global Broad Corporate Index and MSCI USA Index.

Week Ahead

- May 3: Euro area unemployment rate; U.S. factory orders

- May 4: Fed policy decision

- May 5: Bank of England policy decision; China services PMI

- May 6: U.S. employment report; Japan CPI

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of April 25th, 2022 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Investor Information Document (KIID), which may be obtained from MeDirect Bank (Malta) plc.