MeDirect, Malta’s first digital bank, is supporting the 2023 theatre programme of the Soċjetà Filarmonika La Stella in Gozo. The donation was presented to Andrea Camilleri, Director of Musicals at the Society’s Teatru Astra in Victoria, by Amanda Dimech, Wealth Manager at MeDirect’s Gozo investment centre and will help deliver a wide-ranging programme of productions.

Among the productions scheduled for 2023 is The Sound of Music. This much anticipated musical, taking place on 17th, 18th, 19th and 25th March, will star Jasmine Farrugia as Maria alongside West End idol Anthony Edridge as Captain Von Trapp.

Speaking at the presentation, Ms. Dimech said: “MeDirect has established a presence in the heart of Gozo and we are committed to playing a positive role in the cultural and social life of the island. The Soċjetà Filarmonika La Stella is among the leaders in bringing world class theatre and music to Gozo and we are confident that MeDirect’s support will continue to strengthen their efforts.”

Mr. Camilleri said: “2023 is going to be a very busy year for Teatru Astra with preparations for The Sound of Music, the much-loved story of the Von Trapp family, already well underway. The theatre relies on the support of patrons and corporate donations to operate, and we are always heartened to see companies like MeDirect stepping forward to contribute.”

Teatru Astra was inaugurated in 1968, establishing itself as one of Gozo’s leading cultural centres. Since 1978 it has become almost synonymous with the annual production of Opera as well as hosting a range of international singers, plays and musicals.

MeDirect b’appoġġ għall-programm teatrali tat-Teatru Astra matul l-2023

MeDirect, l-ewwel bank diġitali f’Malta, qed jappoġġja l-programm teatrali tal-2023 tas-Soċjetà Filarmonika La Stella f’Għawdex. Id-donazzjoni li se tgħin biex jitwassal programm wiesa’ ta’ produzzjonijie,t ġiet ippreżentata lil Andrea Camilleri, Direttur tal-Musicals fit-Teatru Astra minn Amanda Dimech, Wealth Manager mill-fergħa ta’ MeDirect f’Għawdex.

Fost il-produzzjonijiet skedati għall-2023 hemm The Sound of Music, il-musical tant antiċipat, li se jsir fis-17, 18, 19 u 25 ta’ Marzu. Fost il-parteċipantise jieħdlu sehem Jasmine Farrugia bħala Maria flimkien mal-idolu tal-West End Anthony Edridge bħala l-Kaptan Von Trapp.

Matul il-preżentazzjoni, is-Sa Dimech qalet: “MeDirect stabbilixxa preżenza fil-qalba ta’ Għawdex u aħna mpenjati li jkollna rwol atttiv fil-ħajja kulturali u soċjali tal-gżira. Is-Soċjetà Filarmonika La Stella hija fost l-organizzazzjonijiet ewlenin fil-preżentazzjoni ta’ teatru u mużika ta’ klassi dinjija f’Għawdex u ninsabu fiduċjużi li l-appoġġ ta’ MeDirect se jkompli jsaħħaħ ix-xogħol tant siewi li twettaq is-Soċjetà.”

Is-Sur Camilleri qal: “L-2023 se tkun sena impenjattiva ħafna għat-Teatru Astra bi preparamenti għal The Sound of Music, l-istorja tant maħbuba tal-familja Von Trapp, li diġà mexjin sew. It-teatru jiddependi fuq l-appoġġ tal-benefatturi u d-donazzjonijiet korporattivi biex jopera, u aħna dejjem inkunu mħeġġa meta naraw kumpaniji bħal MeDirect jimxu ‘l quddiem biex jikkontribwixxu.”

It-Teatru Astra kien inawgurat fl-1968 u stabilixxa lilu nnifsu bħala wieħed miċ-ċentri kulturali ewlenin f’Għawdex. Sa mill-1978 it-Teatru kien kwaċi dejjem sinonimu ma’ produzzjonijiet annwali tal-Opra, filwaqt li jospità numru ta’ kantanti internazzjonali, plays u musicals.

Jean Bovin – Head of BlackRock investment institute, together with Wei Li – Global Chief Investment Strategist, Alex Brazier – Deputy Head, and Ben Powell – Chief Investment Strategist for APAC all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Assets at risk: The Bank of Japan looks set to change its ultra-loose policy as inflation takes root. We see spillover risks to global yields, risk appetite and Japanese stocks.

Market backdrop: Global stocks fell last week and U.S. Treasury yields rose across the curve as markets partly priced out Federal Reserve rate cuts later in the year.

Week ahead: The U.S. CPI is due this week. The December core CPI was revised up sharply last week, showing it hadn’t slowed nearly as much as first reported.

Japan’s economy is starting to look like its developed market (DM) peers at least in one way: Inflation is beginning to take root after having been long missing in action for decades. Yet the Bank of Japan’s ultra-loose monetary policy remains, including a cap on bond yields that requires sizable bond purchases. We think a policy change could come at any moment – scrapping the cap risks pushing global yields higher and reducing risk appetite. We cut Japanese stocks to underweight.

Inflation comes to Japan

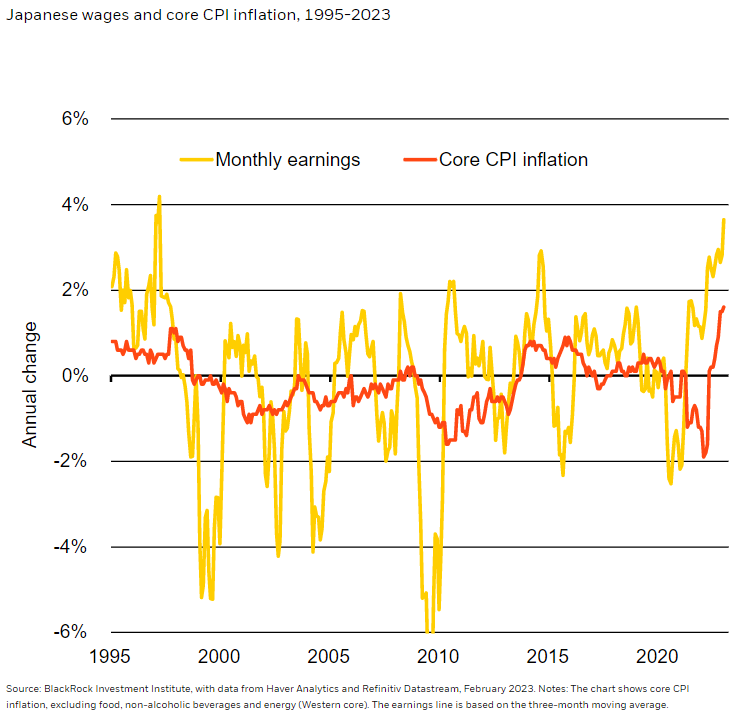

Inflation – long missing in Japan – has reached four-decade highs on a weaker yen and higher energy prices. Crucially, that’s now feeding into higher wages. See the chart. We think that paves the way for the BOJ to roll back policies that by its own measures may have achieved their goal: to foster a sustained rise in inflation toward its 2% target that is underpinned by wage growth. The BOJ’s monetary easing went further than other major central banks with relentless bond buying to cap yields and large-cap stock purchases. Governor Haruhiko Kuroda has led the effort as one part of former Prime Minister Shinzo Abe’s fight against deflation, dubbed “Abenomics.” With wages rising by the most in decades, the BOJ can start winding down these policies. Yet doing so is unlikely to be easy without stirring market volatility. We see any Japanese yield spike from scrapping yield curve control as a global risk that could drive other yields higher and hit risk appetite.

Speculation is rising on what a BOJ leadership change in April will mean for policy. Kuroda’s last meeting as governor will be March 10. But we think who succeeds is less important than the fundamental issue: a nearing shift in policy. Regardless of who takes over, we think the wage and inflation dynamics at play mean the current policy stance has likely run its course. Policy changes could come in different forms. The BOJ could widen the band on its 10-year bond yield target again – market pricing not impacted by the cap is already up to 0.5% higher than that limit. We also think the BOJ could abandon its yield curve control at any moment. That would push yields higher and stoke interest rate volatility. It would put the BOJ on track to stop bond purchases – it owns over half of outstanding Japanese government bonds – potentially let its balance sheet shrink as bonds mature and push up policy rates.

Global ripple effects

We see global implications of a BOJ policy shift. A gravitational pull among developed market bond yields increases the risk of a global spillover, in our view – especially if Japanese investors cut their large foreign bond holdings. We see the jolt from a BOJ policy shift as another driver of higher term premium, or the compensation investors demand for holding long-term government bonds. We think the risk of further rises in global yields could dampen global risk sentiment. The policy change could put the BOJ on course with a larger trend by major central banks to boost yields rather than depress them. The BOJ would then join the quantitative tightening push, with the Federal Reserve doing so now and European Central Bank soon.

These risks prompt us to downgrade Japanese stocks to underweight. Monetary policy uncertainty and the sensitivity of Japan’s economy to the slowdown in other major economies spur the change. Declining earnings growth estimates already reflect some risks from slowing growth – we expect Japan’s export sector to suffer. But we do see the positive undercurrents of corporate reform, a result of one of the economic initiatives in Abenomics known as the “third arrow.” Japan has become a more shareholder-friendly market, in our view, with companies boosting share buybacks and dividends. We prefer unhedged Japanese equity exposures for foreign investors given the policy risks – and we also favor sectors that stand to benefit from automation, digitalization and tourism.

Bottom line

We see a BOJ policy shift driving the risk for higher global yields. That reinforces why yield is back – and why we tactically prefer short-term government bonds and credit for income. We downgrade Japanese stocks on policy uncertainty and a worsening economic environment. We prefer emerging market stocks on a relative basis to DM equities..

Market backdrop

Global stocks fell last week and U.S. Treasury yields rose across the curve as markets partly priced out Fed rate cuts later in the year. We think the risk asset pause shows we’re at a critical crossroads. The messages from Fed officials last week were more clearly about not being done in fighting inflation. Fed Chair Jerome Powell last week stressed the inflation fight will “take quite a bit of time.” We think policy rates could stay higher for longer than the market expects.

Week Ahead

Feb. 14: U.S. CPI inflation; UK jobs data

Feb. 15: UK inflation; U.S. retail sales; U.S. and euro area industrial production; Japan trade

Feb. 16: U.S. housing starts

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 13th February, 2023 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.

Love is in the air, and not just for humans. This Valentine’s Day, MeDirect staff have once again come together to show their love for animals who, despite everything, love us unconditionally. In what is becoming an annual tradition at MeDirect, the money collected was used to purchase pet food and treats for the cats and dogs being cared for by the MSPCA. The items donated were purchased from Borg Cardona & Co Limited who kindly offered discount prices and an additional donation towards this initiative.

The donation was presented by MeDirect’s Head of Products & Marketing Malta, Ingrid Micallef to the MSPCA’s shelter operations and fundraising manager, Mary Cassar Torregiani.

The MSCPA (Malta Society for the Protection & Care of Animals) has a history going back more than 120 years. In addition to caring for animals at its rehoming centre in St Francis Ravelin, Floriana, this independent NGO, which is fully funded through public donations, also works in advocacy and education to promote animal rights and wellbeing. In this regard, MSPCA recently became a full member of Eurogroup for Animals.

If you would like to make a donation to the MSPCA, you can do so here.

You can also speak to the MSPCA if you are looking to give one of the adorable dogs and cats they shelter a loving forever home.

We strive to ensure a streamlined account opening process, via a structured and clear set of requirements and personalised assistance during the initial communication stages. If you are interested in opening a corporate account with MeDirect, please complete an Account Opening Information Questionnaire and send it to corporate@medirect.com.mt.

For a comprehensive list of documentation required to open a corporate account please contact us by email at corporate@medirect.com.mt or by phone on (+356) 2557 4444.