MeDirect has renewed its sponsorship of Otters ASC, the only waterpolo club in Gozo. Through this new agreement, MeDirect will be supporting the club’s senior waterpolo team and its swimming academy. In addition, it will be sponsoring all of the teams playing in national competitions organised by the Aquatic Sports Association of Malta at under 11, under 13 and under 15 level.

Frances Zammit, Senior Officer at MeDirect’s investment centre in Gozo, said, “MeDirect has developed a strong partnership with Otters ASC over several years. Our commitment to Otters, which is not just a waterpolo club, but a key stakeholder in in the Gozitan community, particularly when it comes to helping young people develop in a healthy and active environment, is unwavering. We are looking forward to another great year of collaboration.”

Established in 1971, Otters ASC joined the Maltese waterloo league system on a permanent basis in 1982, as all other Gozitan clubs slowly became defunct. The Marsalforn based club continues to participate in national leagues despite the logistical and financial challenges of operating from Gozo.

Enzo Dimech, President of Otters ASC, said, “Our club needs the support of sponsors like MeDirect to continue offering its services to the community and to continue competing at all levels in Malta’s waterpolo competitions. We are grateful for the long-term commitment which MeDirect has shown towards Otters over many years and look forward to another successful summer for all our players, students, and members.”

Photocaption: Jessica Muscat, Senior Officer – Wealth at MeDirect’s Gozo investment centre presenting the sponsorship to Paul Dimech, Vice President of Otters ASC. Also present were Frances Zammit, Senior Officer at MeDirect’s investment centre in Gozo together with John Borg and Frank Said from Otters ASC.

MeDirect ikompli jappoġġja lil Otters ASC

MeDirect ġedded l-appoġġ tiegħu għal Otters ASC, l-uniku klabb tal-waterpolo f’Għawdex. Permezz ta’ dan il-ftehim, MeDirect se jkun qed jappoġġja lit-tim tal-kbar u l-akkademja ta’ l-għawm tal-klabb. Apparti minn hekk, MeDirect se jkun qed jisponsorja lit-timijiet kollha li qed jilgħabu fil-kompetizzjonijiet nazzjonali organizzati mill-Aquatic Sports Association of Malta ta’ taħt il-11-il sena, taħt it-13-il sena u taħt il-15-il sena.

Frances Zammit, Senior Officer mill-fergħa ta’ MeDirect f’Għawdex, qalet, “MeDirect żviluppa sħubija b’saħħitha ma’ Otters ASC matul is-snin. L-impenn tagħna lejn il-klabb, qed jgħin ħafna lill-komunità Għawdxija b’mod partikolari fl-iżvilupp taż-żgħażagħ f’ambjent b’saħħtu u attiv. Qed inħarsu l-quddiem lejn sena oħra ta’ kollaborazzjoni.”

Otters ASC ġie mwaqqaf fl-1971. Fl-1982, il-klabb ingħaqad mal-kampjonat Malti tal-waterpolo fuq bażi permanenti. Hekk kif il-klabbs l-oħra Għawdxin bil-mod il-mod ma baqawx jezistu, il-klabb Otters ASC, ibbażat f’Marsalforn, kompla jipparteċipa fil-kampjonati nazzjonali minkejja l-isfidi loġistiċi u finanzjarji tal-operat minn Għawdex.

Enzo Dimech, President ta’ Otters ASC, qal, “Il-klabb tagħna għandu bżonn l-appoġġ ta’ sponsors bħal MeDirect biex ikompli joffri s-servizzi tiegħu lill-komunità u jkompli jikkompeti fil-livelli kollha tal-kompetizzjonijiet tal-waterpolo. Aħna grati għall-impenn li MeDirect wera lejn Otters matul ħafna snin u qed nistennew bil-ħerqa sajf ieħor ta’ suċċess għall-plejers, studenti u l-membri kollha tagħna.”

Ritratt: Jessica Muscat, Senior Officer – Wealth tippreżenta l-isponsorship lil Paul Dimech, Viċi President ta’ Otters ASC fiċ-ċentru ta’ investiment ta’ MeDirect f’Għawdex. Preżenti kien hemm ukoll Frances Zammit, Senior Officer ta’ MeDirect f’Għawdex flimkien ma’ John Borg u Frank Said minn Otters ASC.

Jean Bovin – Head of BlackRock Investment Institute, together with Wei Li – Global Chief Investment Strategist, Alex Brazier – Deputy Head, and Nicholas Fawcett – Macro Research all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Holding tight: Central banks are set to hike policy rates this week. Markets expect rate cuts to soon follow due to cooling inflation, whereas we see central banks holding tight.

Market backdrop: U.S. stocks rose last week as initial earnings updates topped low expectations. We think earnings will contract in 2023’s second half as wage gains hit margins.

Week ahead: The Fed and European Central Bank will likely raise interest rates again this week. We see the Bank of Japan opting to keep policy loose to sustain inflation.

The Federal Reserve and the European Central Bank (ECB) are set to hike rates again this week, yet markets have been taking this in stride. Soft June U.S. core inflation has revived hopes for rate cuts in 2024. This can fuel a bull run across assets for some time – until it runs into the disconnect between fast-falling inflation and stronger-than-expected economic activity. We look for opportunities beyond broad asset classes, such as the artificial intelligence theme in equities.

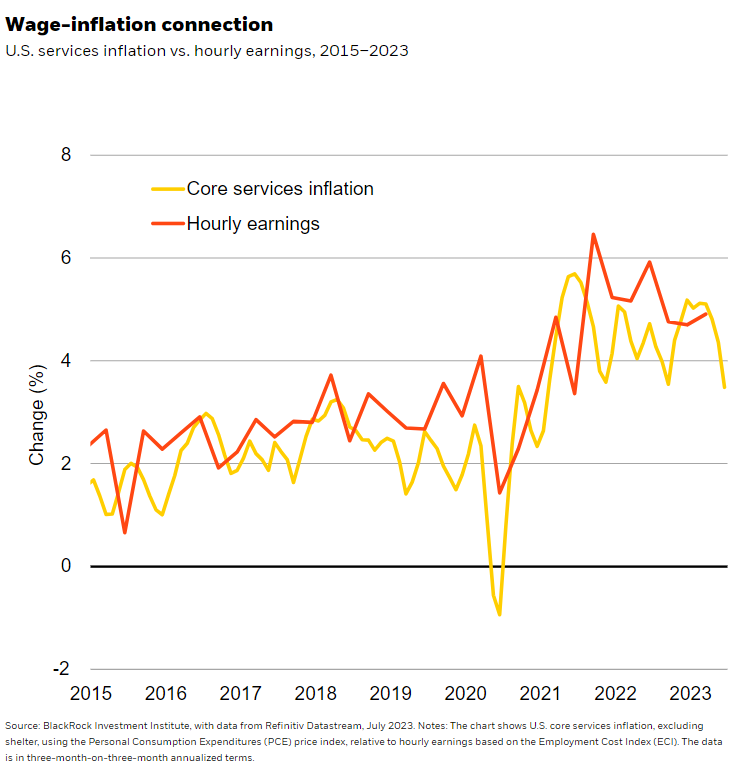

The surprising fall in June U.S. core CPI inflation was clearly good economic news. Yet how can inflation suddenly be falling if the U.S. economy is stronger than expected and the labor market remains tight? First, there’s a perception growth is strong. The reality is that the U.S. economy has barely grown over the last 18 months – despite historically tight labor markets and strong consumption. Second, the inflation story is complex. We are seeing a combination of 1) a shift in consumer spending from goods to services and 2) wage pressures from the tight labor market. The first is spurring goods deflation. The flip side is persistent services inflation, exacerbated by ongoing wage pressures. We expect core services inflation excluding housing (yellow line in the chart) to stay elevated due to those wage gains (dark orange line). The result? A rollercoaster trajectory over the next quarters before inflation likely settles near 3% – well above the Fed’s 2% target.

The U.S. dollar and Treasury yields slid after the CPI data, while stocks moved higher as markets embraced the hope of a “soft landing” – growth holding up and inflation coming down. This hope can sustain risk assets for some time even if it doesn’t pan out. A lot would need to go right for such an outcome, in our view. Activity would need to hold up even as the full force of the Fed’s rate hikes has yet to kick in. That may be possible if tight labor markets spur companies to hold on to workers after struggling to find them coming out of the pandemic. Inflation would also have to drop sustainably closer to 2%.

Margin squeeze

We expect a squeeze on corporate margins if inflation stays high – and an even larger squeeze if it falls. Tight labor markets are set to keep production costs high. A sustained fall in inflation could soften demand. Why? This would likely come from good prices falling further and/or labor markets weakening significantly. So good economic news like falling inflation is not necessarily good news for markets. Margins have already dropped, Refinitiv data show, suggesting companies are starting to have trouble passing higher costs to consumers. We are watching Q2 earnings for more signs of margin pressures.

Holding tight

We see most developed market (DM) central banks forced to hold policy tight to lean against inflationary pressure as they focus on tight labor markets. This is a key theme in our midyear outlook. The Fed, ECB and Bank of England (BOE) face a similar challenge: Inflation has cooled from lower goods prices, but wage gains look set to keep services inflation sticky – and overall inflation on a rollercoaster. We see them pushing ahead on the inflation fight this week, too – though growth is weaker for the euro area and UK. The ECB and BOE have also tightened more aggressively than in the past and are still hiking. The story is different for the Bank of Japan. We think it may opt for loose policy this week to sustain above-target inflation since Japan has fewer supply constraints.

Bottom line

Soft inflation data has rekindled hopes for rate cuts in 2024, even as central banks are set to hike more in the near term and hold tight for long thereafter. We use our new playbook to look beyond broad asset classes in this tricky macro environment. We tap into the AI mega force within DM stocks. Mega cap tech led earnings forecast upgrades due to AI euphoria, and we’ll assess their Q2 earnings for ongoing strength. We upgrade UK equities to neutral as they better price in the weak growth outlook. We like Japanese stocks as loose policy looks set to support earnings. We favor U.S. inflation-linked bonds as markets underestimate inflation’s persistence. Yet we prefer euro area nominal government bonds over the U.S. as they price in rates staying higher for longer.

Market backdrop

U.S. stocks edged up on the week as early earnings updates, mostly from financials, topped low expectations. We expect Q2 results to be similar to Q1 – flat to slightly negative. We see a contraction later in the year as wage gains erode profit margins. Treasury yields steadied as markets eyed the signal from major central banks. UK markets breathed a sigh of relief on soft CPI data: Stocks climbed and 10-year gilt yields fell sharply on the week as markets priced in a lower peak in BOE policy rates.

The Fed and ECB are set to hike rates again this week, while the BOJ may keep policy loose to sustain inflation. U.S labor cost data is likely to reinforce the tight job market is fueling wage gains and inflation pressures. Global PMI data will help gauge how much rate hikes are dampening activity. We see major central banks holding policy tight even as activity slows.

Week Ahead

July 24: Global flash PMIs

July 26: Fed policy decision

July 27: ECB decision; U.S. Q2 GDP

July 28: U.S. June PCE, Employment Cost Index; BOJ decision

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 21st July, 2023 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.

We strive to ensure a streamlined account opening process, via a structured and clear set of requirements and personalised assistance during the initial communication stages. If you are interested in opening a corporate account with MeDirect, please complete an Account Opening Information Questionnaire and send it to corporate@medirect.com.mt.

For a comprehensive list of documentation required to open a corporate account please contact us by email at corporate@medirect.com.mt or by phone on (+356) 2557 4444.