Jean Bovin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Alex Brazier – Deputy Head, and Vivek Paul – Head of Portfolio Research all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Q4 update: Markets are adjusting to the new, more volatile regime. We see opportunities in the UK and euro area bond repricing, and still prefer Japanese equities.

Market backdrop: U.S. stocks dipped last week, and 10-year Treasury yields fell sharply from the week’s highs. A further drop in goods prices helped cool August PCE inflation.

Week ahead: A U.S. government shutdown has been averted for now. Yet the risk of one highlights ongoing U.S. fiscal challenges.

Markets are adjusting to the new regime of greater volatility and higher interest rates. This is starting to create some opportunities, in our view. Yields in long-term government bonds have surged, making European bonds look more attractive to us. Yet broad developed market (DM) equities still don’t fully reflect the new rate environment or unfriendly macro backdrop, even with their retreat. We stay selective in stocks, still preferring Japan and mega forces like artificial intelligence.

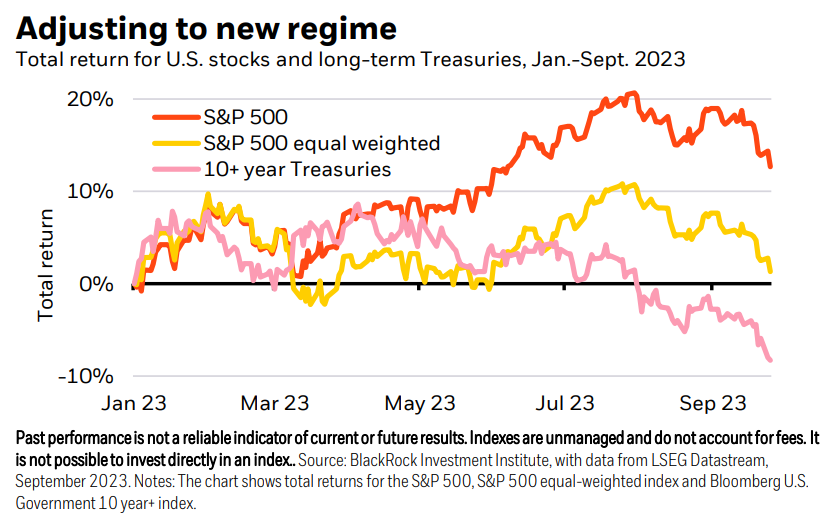

Ten-year U.S. Treasury yields have jumped to 16-year highs and long-term Treasury returns have slid (pink line in chart). The sharp rise in yields since the summer sparked a pullback in equities – with the equal-weighted S&P 500 (yellow line) that adjusts for the outsized impact of mega-cap companies erasing almost all its year-to-date gains. The rise in yields so far has largely been about markets realizing that central banks are poised to keep rates higher for longer, in our view. This adjustment to higher yields is bad for fixed income returns. But not all yield rises are created equal. The repricing of expected policy rates has largely played out, yet the compensation investors demand for the risk of holding long-term bonds – or term premium – has only risen a fraction of the amount we expect. We expect an increase in term premium to drive the next leg of higher yields. That is bad for bonds but not necessarily bad news for equities.

Concerns over U.S. debt levels and large Treasury issuance have prompted investors to demand more compensation for the risk of holding long-term bonds, driving long-term yields higher. We expect a further rise in such term premium and long-term yields due to those factors, plus persistent inflation and higher-for-longer rates. With long-term yields at multi-year-highs, bonds offer more income. Yet a march higher in yields can wipe that out: A roughly 0.5 percentage point rise in yields could drag on valuations enough to erase a full year of income for a 10-year duration bond. And such moves can happen quickly in this new macro regime. We stay underweight long-term bonds in our tactical and strategic views in Q4. The threat of a U.S. government shutdown – if pushed back for now – also highlights the long-term fiscal challenges the U.S. faces. If Congress eventually fails to provide funding for the new fiscal year, we expect a limited macro and market impact – similar to past shutdowns – because only a small part of the economy is directly impacted.

Eyeing opportunities

The difficult macro environment keeps us underweight the broad U.S. equity market on a tactical horizon of six to 12 months: Stocks don’t fully reflect higher-for-longer rates and the ongoing activity stagnation we expect. With the Q3 earnings season starting soon, analysts now see a mild contraction in broader Q3 earnings after having eyed growth earlier in the year, LSEG data show. We are getting closer to turning more positive on stocks given the recent retreat – but we’re not quite there yet.

As markets play catch up with the new regime and its implications, we take advantage of relative disconnects in market pricing and find new opportunities based on what’s in the price. We recently went overweight long-term euro area government bonds and UK gilts on higher yields and our view policy rates will be cut more than the market is pricing. Higher yields also underpin our overweights to short-term Treasuries and EM hard currency debt – generally issued in U.S. dollars.

We center our outlook on mega forces, or structural forces that can drive returns now and in the future. We get granular within asset classes to find sectors and regions that can thrive even as growth broadly stagnates in coming quarters. We went overweight Japanese stocks last month on the potential for earnings to beat expectations and ongoing shareholder-friendly reforms. We’re also neutral on UK and EM stocks. Our overweight to the digital disruption and artificial intelligence (AI) mega force in DM stocks taps into markets favoring companies generating ample profits over any hit from higher-for-longer rates.

Bottom line

We find new opportunities in Q4 via pricing disconnects and mega forces. Read our updated global outlook.

Market backdrop

U.S. stocks dipped last week, while the 10-year U.S. Treasury hit a 16-year high of 4.69% before retreating sharply on Friday. Euro area bond yields hit multi-year highs last week as markets priced in policy rates staying higher for longer, with fewer rate cuts. And Italian government bond spreads widened on a wider-than-expected government budget deficit forecast. Meanwhile, U.S. core PCE inflation rose less than expected in August as goods prices extended their drop.

With a U.S. government shutdown avoided for now, U.S. payrolls data for September is in focus this week. Pandemic-era mismatches in supply are unwinding – helping to cool inflation. Yet we think a shrinking workforce as the population ages means the economy will only be able to sustain a fraction of recent job growth to avoid resurgent inflationary pressures.

Week Ahead

Oct. 2: U.S. ISM manufacturing PMI; euro area unemployment

Oct. 4: U.S. ISM services PMI

Oct. 6: U.S. payrolls report

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 25th September, 2023 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.