Wei Li – Global Chief Investment Strategist together with Alex Brazier – Deputy Head, Axel Christensen – Chief Investment Strategist for Latin America, and Michael Dilmanian – Investment Strategist all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

- We favor emerging market (EM) to developed market (DM) assets on a brighter macro backdrop. We get granular and harness mega forces, per our playbook.

- U.S. bond yields slumped last week on softer CPI inflation data. We think stilltight labor markets will compel the Federal Reserve to hold policy tight.

- We look to this week’s U.S. data for more signs higher policy rates are cooling production and spending. We see policy staying tight even as activity weakens.

We tapped into what’s proved a stealth rally in EM stocks and bonds, along with the DM stock gains this year. We still think EM assets have an edge over developed market (DM) peers in the first layer of our new playbook, the macro assessment. Inflation is cooling enough in key EMs to allow policy rate cuts. We get granular in our playbook’s second layer to find countries and sectors we like. Our third layer harnesses mega forces to capture structural shifts within EMs.

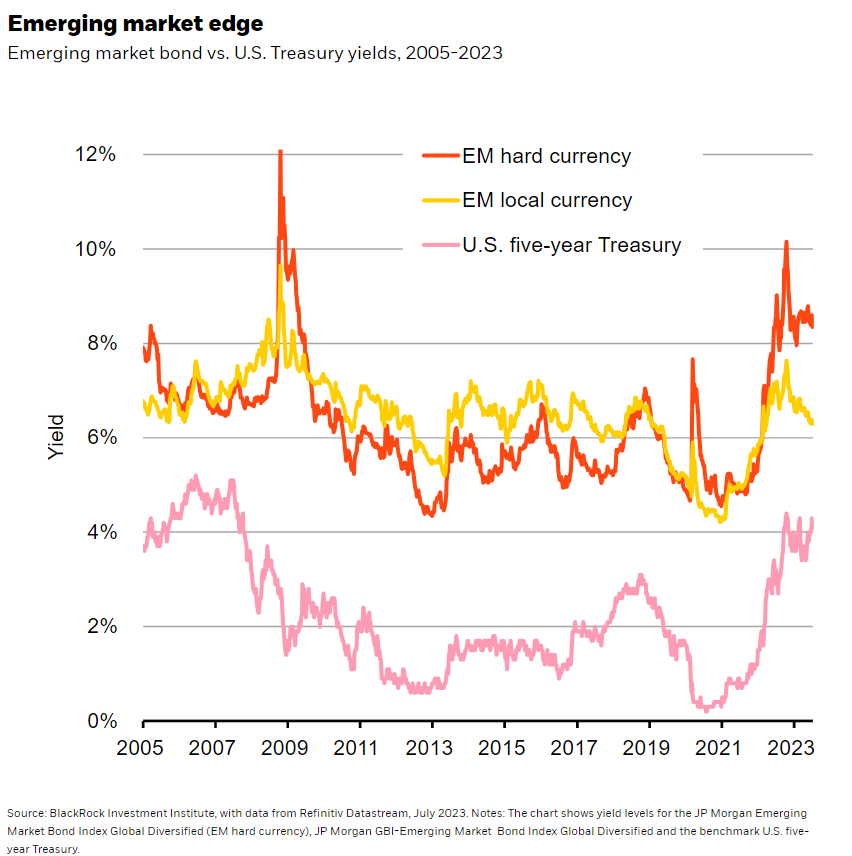

We’ve preferred EM debt to DM long-term peers for some time. We went tactically overweight EM local currency debt in March, picking up higher yields for carry and benefiting from a broadly weaker U.S. dollar plus tightening spreads this year (yellow line in chart). Higher EM yields remain attractive, but tightening spreads with Treasuries (pink line) lead us to consider switching to hard currency peers typically issued in U.S. dollars (orange line). But peaking DM policy rates should support EM currencies, bolstering EM local debt for now. DM rate hikes have hit EM hard in the past, but we think they’re in a different spot now thanks to improved external balance sheets. We think that’s why we’re not seeing the EM asset volatility as in the 2013 taper tantrum. The Fed’s plan to taper bond purchases then sparked sharp EM capital outflows and currency depreciation. It’s the opposite now: capital inflows and stronger currencies are boosting returns in EM local currency bonds.

A brighter EM macro and policy picture may also be underappreciated, in our view. DM central banks inching toward the end of rapid hikes is good for EMs – but a key difference is we think EM peers are closer to rate cuts as inflation falls. EM central banks were well ahead of DM peers in hiking – and some have hiked much more to bring inflation down quickly. Take Brazil: Policy rates have risen to just under 14% from 2% in 2021. When it comes to EM investing this year, much focus has been on China’s economy losing steam. But outside China, EM equities have staged a stealth rally with double-digit gains across Latin America and other parts of Asia. We see more upside there and more attractive valuations relative to DM economies as the policy picture and EM economic growth prospects improve, even as China’s restart sputters. That’s the first layer of our new playbook in action: our macro take in the context of what’s in the price.

Evolving our playbook

The second layer of our new playbook is about getting granular. We go beyond broad EM exposures to find the brightest macro backdrops across countries and most attractive valuations under the surface. Within EM local currency bonds, we like Mexico for its quality tilt and Brazil for its exceptional carry from still-high bond yields. Our playbook also calls for being nimble. EM is not disconnected from global growth, so we are constantly watching for how that may affect the EM backdrop.

We also get granular in sectors and regions and use the third layer of our playbook – harnessing mega forces – to capture returns now and in the future. We see five big structural forces transcending the macro backdrop: digital disruption and artificial intelligence (AI), geopolitical fragmentation, the low-carbon transition, aging populations and the future of finance. We see abundant EM equity opportunities through these mega forces – what matters is what markets have priced. The semiconductor industry is powering AI and is a key part of the EM technology sector. A rapidly growing population in India sets the country apart from DMs. India’s system of digital payments also bodes well for the future of finance there, we believe: It could pave the way for a credit boom as banks adapt lending. We think the low-carbon transition presents an important opportunity for Latin America, especially for countries that hold large reserves of key resources like copper and lithium. The rewiring of supply chains due to global fragmentation could also have significant implications for countries like Mexico that could benefit if U.S. companies bring operations and production closer to home.

Bottom line

Our new playbook leads us to favor EM over DM assets. We see a brighter policy outlook as some EMs stand ready to cut policy rates. We get granular in EM debt across countries and in EM equities by harnessing mega forces.

Market backdrop

U.S. bond yields dropped and stocks climbed to 15-month highs last week as markets eyed an end in sight to the Fed’s rapid hiking cycle after the softer-than-expected June CPI data. Both two- and 10-year Treasury yields posted their sharpest weekly declines since the March banking turmoil. The labor market is key for what lies ahead for inflation. We see still-strong wage growth keeping core inflation elevated, compelling the Federal Reserve to hold policy tight.

We look to U.S. data out this week for more signs that higher policy rates are cooling production and spending. CPI data across developed markets will likely show persistently high inflation – making central banks hold tight on policy. We’re also focusing on GDP and industrial data for China to gauge to what extent its economic restart is losing steam.

Week Ahead

July 17: China GDP, industrial production

July 18: U.S. industrial production, retail sales; Canada CPI

July 19: UK CPI

July 20: U.S. Philly Fed business index

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 17th July, 2023 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.