Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Ben Powell – Chief Investment Strategist for APAC all forming part of the BlackRock Investment Institute and Yuichi Chiguchi Head of Multi-Asset Strategies & Solutions and Chief Investment Strategist in Japan share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

The rally rolls on: A weak yen is unlikely to end the positive momentum in Japanese equities. The drivers of the recent rally remain, so we stay overweight Japanese stocks.

Market backdrop: The S&P 500 neared its 2024 highs last week, supported by strong Q1 earnings. In Japan, authorities appear to have intervened to bolster a weak yen.

Week ahead: We’re eyeing U.S. CPI inflation data this week to gauge if it will keep coming in hot. We see U.S. interest rates staying high for longer given sticky inflation.

Twelve-month returns for the MSCI Japan are near 14% in U.S. dollar terms. We don’t see the recent slide in the yen to 34-year lows versus the dollar derailing this momentum. Why not? Japan’s growth outlook remains positive, corporate reforms are taking hold and rising wages can support consumer spending. Ultimately, yen weakness is mainly due to the gap between Bank of Japan and Fed policy rates. The yen could recover once the Fed cuts. We stay overweight Japan’s stocks.

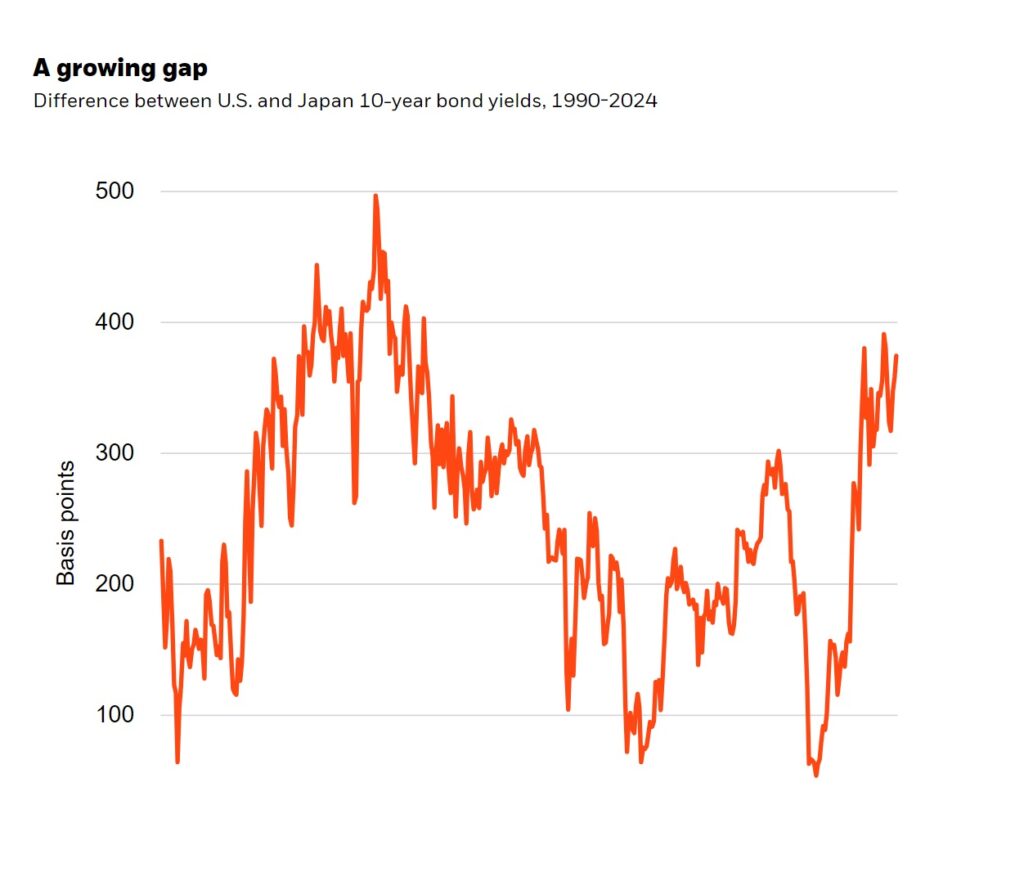

At the end of April, the yen tumbled to near 160 to the dollar – its lowest in 34 years. The Japanese authorities appear to have intervened by buying U.S. dollars, warning investors betting against the yen and helping slow its slide. Any near-term drivers aside, we think the yen’s weakness is caused by the gap between Fed and Bank of Japan (BOJ) policy rates. The Japanese currency started depreciating in 2022 as the Fed started hiking rates rapidly. Its fall accelerated in April as the BOJ affirmed it would not rush to unwind its loose policy, while markets pared back their pricing of Fed rate cuts for this year given sticky U.S. inflation. Government bond yields for the U.S. and Japan reflect that gap in the market’s monetary policy expectations. Ten-year U.S. Treasury yields have surged above Japanese government bond yields, with the difference close to two-decade highs. See the orange line in the chart.

Yet we think that gap between U.S. and Japan 10-year yields could narrow again as BOJ and Fed policy rates begin to move closer to each other. Sticky U.S inflation may mean the Fed will keep interest rates high for longer, but we still see it starting to cut them later this year. And the BOJ is likely to hike rates again as it cautiously normalizes its emergency policy of negative interest rates. That should ease pressure on the yen. That said, should the yen weaken significantly between now and then, it could stoke inflation as the cost of imported food and energy rises. The BOJ could respond by tightening policy more rapidly. But we think that’s unlikely as it would risk threatening an improving growth outlook, and victory in its decades-long battle against no or low inflation is not yet assured. We see government subsidies on food and energy as a more likely response.

The impact of a weak yen

A weak yen affects Japanese firms differently. Manufacturers with higher input costs may see lower earnings. Yet as Japan’s goods become cheaper for foreign buyers, that will benefit the exporters that make up over half the market capitalization of Japan’s TOPIX index. As recent wage negotiations lead to higher wages, a strong consumer could support some sectors.

Japanese stocks have surged, based on the excess yield that investors receive for the risk of holding them over bonds. But we stay overweight Japanese stocks on a six- to 12-month, tactical horizon. The rally is a sign investor confidence is perking up. And a weaker yen doesn’t change the reasons behind our positive stance. The return of inflation in Japan means companies can raise prices and expand their net profit margins. Plus, shareholder-friendly corporate reforms are taking root, with more firms joining the Tokyo Stock Exchange’s list of those with plans to improve their governance. Government initiatives to encourage more domestic savers to invest could boost flows into Japanese stocks. These shifts are playing out over time. We also see mega forces – big structural shifts driving returns – creating long-term opportunities in Japan. For example, Japan’s population has been aging for many years. That has propelled efforts to adopt automation to boost productivity.

Our bottom line

We see diverging monetary policy driving the slide in the yen, but we don’t see the pressure persisting. We stay overweight Japanese stocks given ongoing corporate reforms and eye opportunities created by structural shifts.

Market backdrop

The S&P 500 climbed higher last week, approaching its 2024 highs. U.S. 10-year Treasury yields hovered around 4.50%. Given structurally higher interest rates, the onus has fallen on earnings to sustain U.S. equity strength. U.S. Q1 earnings have cleared a high bar thus far, showing strong results and signs of broadening. Japanese equities and 10-year government bond yields were flat. A historically weak yen, near 34-year lows versus the U.S. dollar, prompted suspected currency intervention.

We await U.S. CPI inflation data this week as some components have recently been higher than expected. We’re eyeing whether that will carry on. Supercore services inflation excluding food, energy and housing is particularly in focus as it will determine where inflation ultimately settles. We’re also watching core goods given their bumpy post-pandemic normalization. After softer-than-expected U.S. payrolls and wages, markets are again expecting a September rate cut.

Week Ahead

May 14: UK employment data

May 15: U.S. CPI

May 16: U.S. Philly Fed Business Index; Japan GDP data

May 10-17: China total social financing

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 13th May, 2024 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.