Wei Li – Global Chief Investment Strategist of BlackRock Investment Institute together with Glenn Purves – Global Head of Macro, Bruno Rovelli – Chief Investment Strategist for Italy and Carolina Martinez Arevalo – Portfolio Strategist, all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Staying selective : We still see tariffs causing further contractions in quarterly activity but the cumulative impact may be more limited. We eye opportunities from mega forces.

Market backdrop : U.S. stocks ticked down last week after a tech-driven rally over easing restrictions on AI chip exports. UK stocks rose on news of a U.S.-UK trade deal.

Week ahead : We’re looking for early signs of tariffs pushing up inflation in U.S. CPI data out this week. Sticky inflation will limit how far the Federal Reserve can cut rates.

The U.S.-China deal represents a major de-escalation in the trade conflict. Three key takeaways? First, it reaffirms that the hard economic rules we’ve been flagging will shape policy. Second, tariffs will likely bring more supply-driven contractions in quarterly activity, but the cumulative impact on overall 2025 activity could be more limited. Third, the deal gives a sense of where the U.S. effective tariff rate will settle. We stay risk on, monitoring corporate earnings reports for selective opportunities.

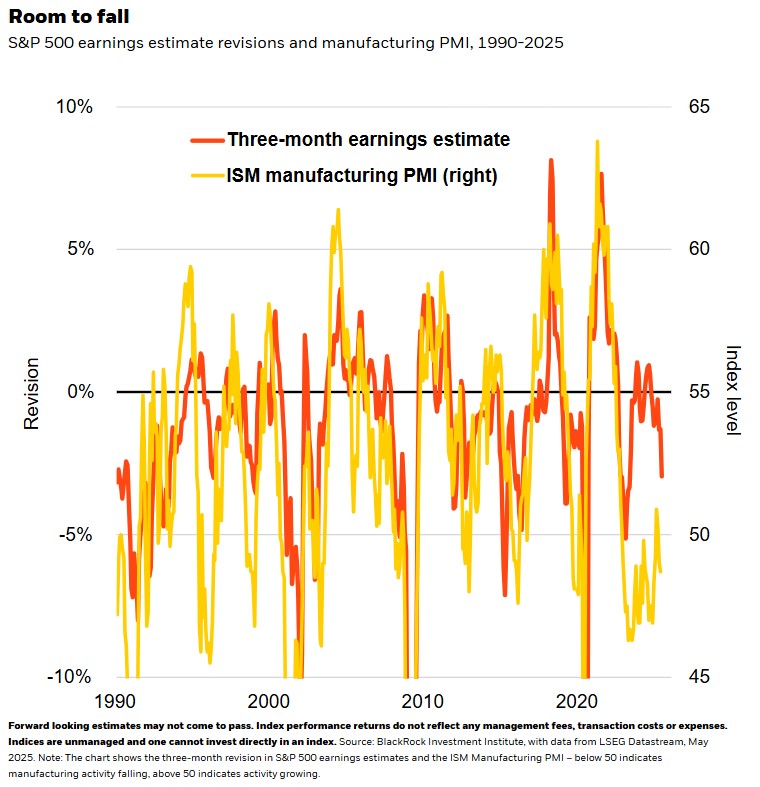

The 90-day cut to U.S.-China tariffs shows a hard economic rule shaping policy: supply chains can’t be rewired quickly without disruption. That’s reflected in both nations’ explicit goal of avoiding economic “decoupling.” We still think tariffs will up inflation and hurt growth, with recession-like effects in coming quarters. Earnings estimates often suffer steep cuts when activity slumps. See the chart. Analysts have already cut forecasts for broad S&P 500 earnings growth from 14% in January to 8.5%, a slightly bigger drop than in an average year, per LSEG data. Yet the cumulative impact on overall 2025 activity may be more limited. The U.S. average effective tariff rate could land around 10-15%, we estimate, higher than at the start of 2025 but a more manageable economic disruption. We stay positive on developed market (DM) stocks and see mega forces creating select opportunities.

As we track how evolving tariffs ripple out, we see three key themes in Q1 earnings reports. First, moving production to the U.S. or countries on better terms with the U.S. has, for the first time, been discussed on all Q1 earnings calls so far, per Alphasense data. Some are now giving timelines. Second, many firms look set to accept higher input costs as supply chains adjust. The latest external estimates see tariffs denting net earnings by around 5%. Third, 60% of companies updating their spending plans are now guiding below consensus forecasts – up from 40% at the start of the year but still below the 71% hit in the pandemic, Bank of America and FactSet data show. Yet opportunities persist in certain sectors. Big tech is reaffirming or upping AI-linked investment, for example. And Q1 results show U.S. companies are starting from a position of strength.

What we like

In Europe, infrastructure and defense spending plans have led us to upgrade European equities to neutral. Yet execution of those plans is key – and the new German chancellor’s limited coalition support highlights potential obstacles. Europe’s Stoxx 600 has performed broadly on par with the S&P 500 since the April 2 tariff announcement and European earnings estimates for 2025 have fallen to 3.5% from 8% in January. Yet that masks divergence. Financials are up over 20% this year, thanks to persistently high yields and strong company and household balance sheets. We’ve preferred Spain since the start of 2025 due to strong growth and exposure to financials, utilities and infrastructure – sectors that benefit from mega forces. Spanish stocks are also less exposed to U.S. tariffs: only 5% of its exports are U.S.-bound, less than the EU average, trade data show. Japanese equities offer another bright spot: Ongoing corporate reforms keep us overweight on a currency-unhedged basis.

Structural shifts also call for selectivity in other asset classes. Gold has been a better buffer against geopolitical risks than other traditional safe-haven assets since April 2. It has soared, while long-term U.S. Treasuries and the U.S. dollar have – unusually – slid alongside stocks, Bloomberg data show. Under new regulation, U.S. banks will soon be able to treat gold as a high-quality asset on their balance sheets. That could drive demand and make gold a core holding.

Our bottom line

We still see supply disruptions upping inflation and hitting growth, but also a path to avoiding a U.S. contraction over 2025 as a whole. Mega forces, greater fiscal spending and higher interest rates are driving select opportunities.

Market backdrop

U.S. stocks ticked down last week after a tech-driven rally on reports the U.S. plans to lift restrictions on AI chip exports. The S&P 500 remains 8% below February’s record high. The UK’s FTSE 250 rose more than 1% last week and hit a two-month high after the Bank of England cut rates by 25 basis points and the U.S. signed a trade deal with the UK. U.S. two-year and 10-year Treasury yields were largely steady at 3.89% and 4.39% respectively as the Federal Reserve left rates unchanged.

U.S. CPI data for April is in focus this week. While it’s probably too soon to see the early April tariffs pushing up directly on inflation, we’re watching for signs of an uptick in core goods prices. We think sticky inflation will make it difficult for the Fed to cut interest rates much this year as it grapples with a now sharper trade-off between protecting growth and reining in inflation.

Week Ahead

May 13 : U.S. CPI

May 15 : Japan GDP; Philly Fed Business index

May 16 : University of Michigan consumer sentiment survey

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 12th May, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.