During 2021, MeDirect Group continued to accelerate its investment programme to build its highly customer centric app combining a broad range of investment services seamlessly integrated with daily banking functionality.

The Group’s technology platform has been undergoing an impressive transformation for over the past two years, by leveraging on a unique flexible and scalable technologies along with the objective of delivering best-in-class user experience to support its mission of making digital investment simple, inclusive and empowering for all. Later this year, the Group will launch exciting new functionality to its website, mobile app and other customer touch points.

“In the first half of 2021, MeDirect Group maintained steady progress as it achieved strong growth in all those business lines targeted for new investment, resulting in an encouraging profitable performance following 2020 which was a year impacted by significant impairment provisions due to the COVID-19 pandemic,” said Arnaud Denis, Chief Executive Officer of MeDirect Group.

In the first six months of 2021, MeDirect Group continued to implement its balance sheet diversification by actively planning the launch of its future Belgium residential mortgage business line and by successfully launching the home loan business in Malta earlier in 2021.

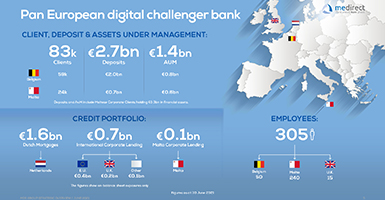

In addition, the Group continued to achieve positive growth in business volumes in jurisdictions in which it operates. In fact, over the past 12 months, total clients in Belgium and Malta increased by 15 per cent to 83,000, leading to a 31 per cent increase in assets under management with an all-time high of Eur0.8 billion (44 per cent increase) in Belgium and Eur0.6 billion (18 per cent increase) in Malta.

Over the past twelve months, the Dutch residential mortgage origination volumes grew by Eur1.0 billion (168 per cent increase) and corporate lending in Malta increased by 25 per cent to €108.4 million as the Group continued to support the local economy.

By starting to benefit from a more diversified business model and given the improving credit outlook, the Group achieved a promising performance in the first half of 2021 as profit before tax was Eur3.2 million compared to a significant loss last year driven by prudent provisioning to reflect the impact of COVID-19.

MeDirect Group continued de-risking its international corporate lending portfolio such that, since the beginning of the financial year, the gross size of the portfolio has been reduced by 24 per cent from Eur903.4 million to Eur691.1 million and by 46 per cent over the last twelve months.

The gross outstanding balances of the Dutch mortgage book grew by 32 per cent throughout this financial period and as at 30 June 2021 amounted to Eur1.6 billion. Total funding increased as a result of the funding from the Dutch mortgage securitisation transactions that increased from Eur348.2 million to Eur682.6 million.

The Group’s liquidity remained robust, and capital ratios remained well above minimum requirements. The total capital ratio remained high at 19.3 per cent as at 30 June 2021. MeDirect Group’s liquidity reserves remained strong at Eur601 million as at 30 June 2021, and the Group’s LCR stood at 625 per cent.

Mr Denis concluded: “The Group’s financial performance improved with lower impairment charges, better capital ratios. Although the outlook for the rest of the year remains challenging, MeDirect continues its accelerated transformation into a leading retail WealthTech banking platform and is working strongly to revert to sustainable profitability in the medium term as we remain disciplined but cautiously optimistic as the economic recovery unfolds.”

MeDirect Bank iżomm ir-ritmu mgħaġġel ta’ bidla b’aktar żvilupp fil-pjattaforma tiegħu tal-WealthTech

Matul l-2021 il-Grupp MeDirect baqa’ għaddej b’ritmu mgħaġġel bil-programm ta’ investiment biex ikompli jiżviluppa l-app tiegħu iffukata fuq il-ħtiġijiet tal-klijenti, u li tiġbor firxa wiesgħa ta’ servizzi ta’ investimenti u tintegrahom mal-funzjonijiet bankarji l-oħra ta’ kuljum.

Fl-aħħar sentejn, il-pjattaforma diġitali tal-Grupp sarulha għadd ta’ bidliet sinifikanti bis-saħħa ta’ teknoloġiji uniċi li huma flessibbli u addatabbli sabiex toffri esperjenza tal-ogħla livell lil min jużaha ħalli b’hekk ukoll isseħħ il-missjoni tal-Grupp li jagħmel il-proċess tal-investiment diġitali eħfef, inklużiv u li jista’ jintuża minn kulħadd. Aktar tard din is-sena, il-Grupp se jniedi funzjonalità eċċitanti oħra fil-website tiegħu, fil-mobile app u f’mezzi teknoloġiċi oħra li jużaw il-klijenti.

Arnaud Denis, il-Kap Eżekuttiv tal-Grupp MeDirect, qal li: “Fl-ewwel nofs ta’ din is-sena, il-Grupp MeDirect żamm ir-ritmu ta’ progress u kellu tkabbir b’saħħtu fil-linji kollha tan-negozju immirati għal investiment ġdid, li wassal għal riżultat finanzjarju nkoraġġanti bi profitt u dan wara sena diffiċli bħalma kienet is-sena 2020, li ġabet magħha sfidi kbar minħabba l-pandemija tal-COVID-19.”

Fl-ewwel sitt xhur tal-2021, il-Grupp MeDirect kompla jimplimenta d-diversifikazzjoni tal-balance sheet tiegħu billi ppjana, b’mod attiv, it-tnedija fil-futur ta’ self għax-xiri ta’ djar residenzjali fil-Belġju waqt li diġa nieda b’suċċess l-istess tip ta’ negozju tas-self għad-djar f’Malta, aktar kmieni din is-sena.

Barra minn hekk, il-Grupp baqa’ jkollu tkabbir pożittiv fil-volumi tan-negozju fil-pajjiżi li jopera fihom. Fil-fatt, fl-aħħar 12-il xahar, il-klijenti totali fil-Belġju u f’Malta żdiedu bi 15 fil-mija u issa jlaħħqu 83,000 ruħ – żieda ta’ 31 fil-mija fl-assi mmaniġġjati (assets under management) li jammontaw għal ċifri, bla preċedent għal bank, ta’ €0.8 biljun (żieda ta’ 44 fil-mija) fil-Belġju u ta’ €0.6 biljun (żieda ta’ 18 fil-mija) f’Malta.

Matul dawn l-aħħar 12-il xahar, l-ammont ta’ self fuq id-djar, li l-Bank jagħmel fl-Olanda żdiedu b’ €1 biljun (jew b’168 fil-mija) u s-self lill-kumpaniji f’Malta żdied b’25 fil-mija għal €108.4 miljun, u dan fisser li l-Grupp kompla jgħin ukoll lill-ekonomija lokali.

Il-Grupp issa beda jara l-frott mid-deċiżjoni li kien ħa qabel biex jiddiversifika l-mudell ta’ negozju tiegħu u, anke bis-saħħa tat-titjib ġenerali fis-suq tas-self, fl-ewwel nofs tal-2021 kiseb riżultati tajbin, tant li l-profitt qabel it-taxxa, fl-ewwel sitt xhur ta’ din is-sena, kien ta’ €3.2 miljun. Dan huwa riżultat tajjeb meta mqabbel mat-telf sinifikanti li ġarrab il-Grupp is-sena li għaddiet minħabba l-provvedimenti (provisions) li b’mod prudenti kellu jagħmel minħabba l-pandemija tal-COVID-19.

Il-Grupp MeDirect kompla jnaqqas ir-riskju mill-portafoll internazzjonali tiegħu ta’ self korporattiv u, mill-bidu tas-sena finanzjarja (1 ta’ Jannar 2021), id-daqs gross tal-portafoll tnaqqas b’24 fil-mija minn €903.4 miljun għal €691.1 miljun u b’46 fil-mija meta mqabbel ma’ tnax-il xahar ilu.

Il-bilanċi tas-self fuq id-djar fl-Olanda kibru bi 32 fil-mija matul dan il-perjodu finanzjarju u fit-30 ta’ Ġunju 2021 kienu jammontaw għal €1.6 biljun. Il-finanzjament totali żdied minħabba l-finanzjament mit-tranżazzjonijiet tat-titoli ipotekarji (mortgage securitisation transactions), li żdiedu minn €348.2 miljun għal €682.6 miljun.

Il-likwidità tal-Grupp baqgħet b’saħħitha u l-livelli tal-kapital (capital ratios) inżammu ’l fuq sew mir-rekwiżiti minimi. Il-proporzjon tal-kapital totali (total capital ratio) baqa’ għoli, u fit-30 ta’ Ġunju 2021 kien f’livell ta’ 19.3 fil-mija. Ir-riservi tal-likwidità tal-Grupp MeDirect ukoll baqgħu sodi, u fit-30 ta’ Ġunju 2021 kienu jammontaw għal €601 miljun, filwaqt li l-LCR (liquidity coverage ratio) tal-Grupp kien ta’ 625 fil-mija.

Is-Sur Denis ikkonkluda li: “Il-prestazzjoni finanzjarja tal-Grupp tjiebet grazzi għal provvedimenti (provisions) aktar baxxi, u b’riżultati aħjar fil-livelli tal-kapital (capital ratios). Minkejja li s-sitwazzjoni għall-bqija ta’ din is-sena se tibqa’ waħda ta’ sfida, MeDirect se jibqa’ għaddej b’ritmu mgħaġġel ta’ bidla biex jagħmel il-pjattaforma bankarja tiegħu tal-WealthTech waħda ewlenija f’dan is-settur, waqt li jaħdem bis-sħiħ biex jilħaq sitwazzjoni sostenibbli ta’ profitt fuq medda ta’ żmien medju. Il-Bank irid jibqa’ jaħdem b’mod dixxiplinat u kawtel u fl-istess ħin huwa ottimist li l-irkuprament tal-ekonomija mill-pandemija se jkompli.”

MeDirect Bank (Malta) plc, is licensed to undertake the business of banking in terms of the Banking Act (Cap. 371) and investment services under the Investment Services Act (Cap. 370).