Jakir Hossain, an associate data journalist for Morningstar who covers stock trends and news for the markets team discusses the bear market, which is a decline of 20% or more of a major stock market index, and shares information on listed stocks covered by Morningstar analysts that are undervalued.

There’s one good thing about a bear market: For investors looking to put money to work, stocks end up cheaper than they were before it started.

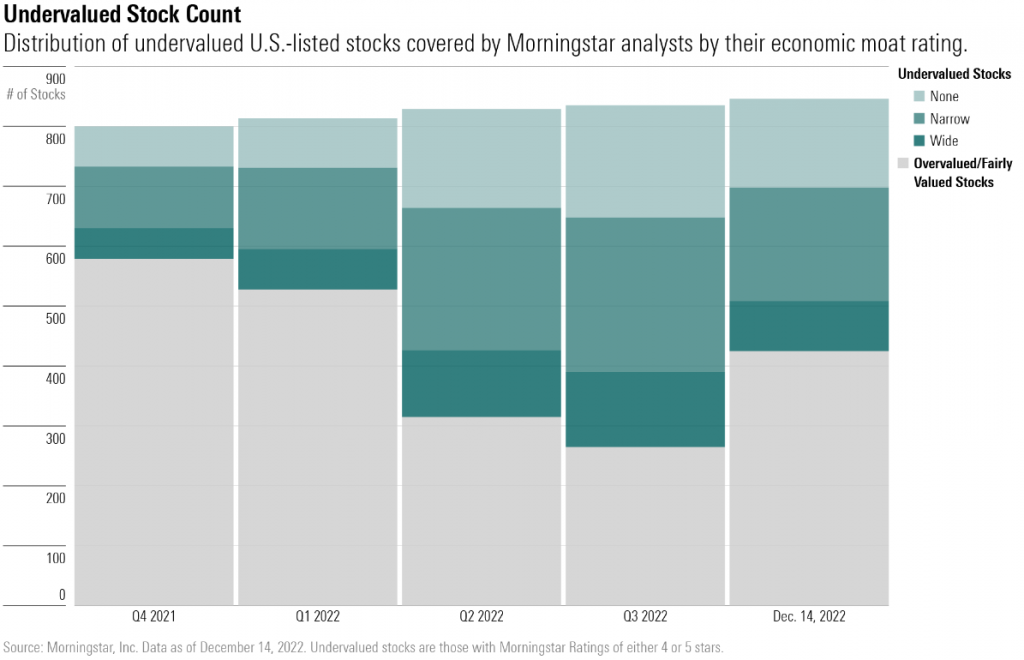

Valuations for the U.S. market did a flip-flop from the start of the year, with Morningstar analysts now viewing the market as 11% undervalued, compared with 6% overvalued during its peak on Jan 3.

As of Dec. 14, 421 of the 846, or about 50%, of the U.S.-listed stocks covered by Morningstar analysts are undervalued—having a Morningstar Rating of 4 or 5 stars. About 305 of them are considered 20% undervalued or more. At the start of the year, only 221 stocks were considered undervalued, and 126 were 20% undervalued or more.

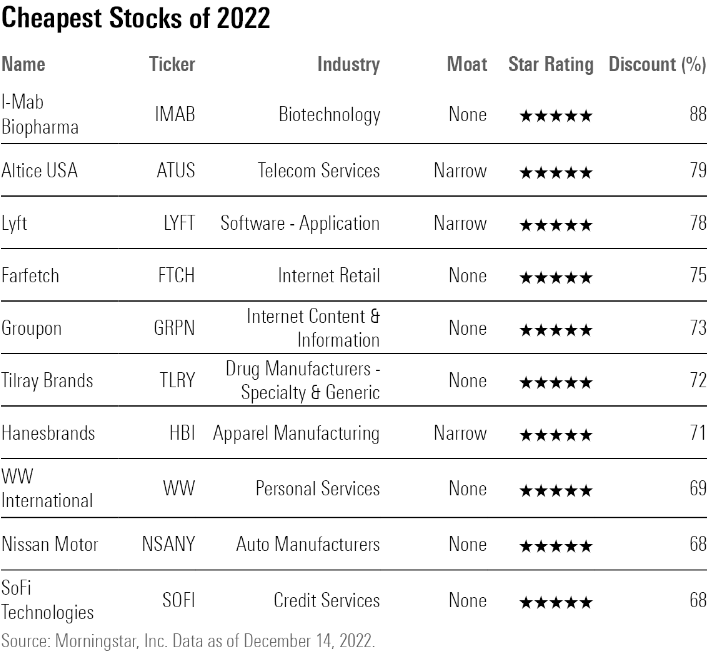

Heading into the final days of 2022, here are the stocks trading at their biggest discounts to their Morningstar fair value estimates:

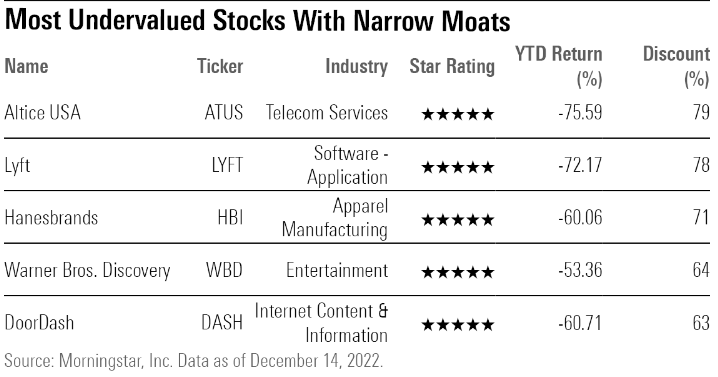

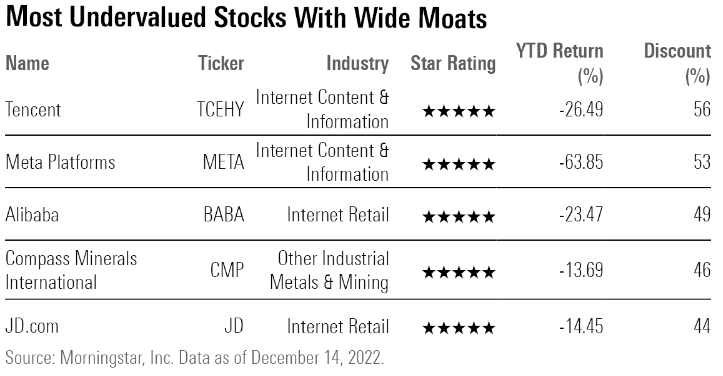

The bear market knocked down stocks of all stripes, including high-quality companies that Morningstar’s stock analysts assigned a Morningstar Economic Moat Rating of wide or narrow to, meaning they have durable competitive advantages over their peers. Companies with wide moats are expected to retain their competitive advantages for more than 20 years, while those with a narrow moat can fend off competition for 10 years. Among the most undervalued narrow- or wide-moat stocks in our coverage list:

- I-Mab Biopharma (IMAB)

- Altice USA (ATUS)

- Lyft (LYFT)

- Farfetch (FTCH)

In fact, about 274 of the undervalued stocks have a narrow or wide moat rating.

That’s the case even after Morningstar analysts cut back on their growth assumptions following third-quarter results, which led to a number of Morningstar fair value estimate cuts. In part due to fair value estimate cuts, 149 stocks lost their undervalued status between the end of the third quarter and Dec. 14.

Still, there’s a long list of stocks that remain at prices that leave them undervalued, analysts at Morningstar believe, even quality stocks with economic moats.

In fact, most of the undervalued stocks are those with narrow moats—191 of the 421 undervalued overall. On average, narrow-moat stocks are at an 11% discount.

Stocks with a wide economic moat rating are fewer in number, representing 83 of the 421 undervalued stocks overall. Though they tend to be less discounted than their narrow-moat peers at an average 7% discount to their fair value estimates.

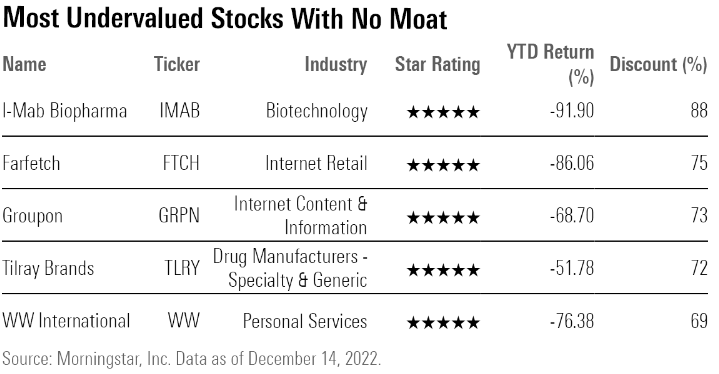

Lastly, here’s a list of undervalued stocks for companies that did not earn a moat rating. No-moat stocks trade at the highest average discount to their fair value estimates at about 15%.

To build a list of undervalued quality stocks, we screened for stocks that had a rating of 4 or 5 stars, and then sorted the results by each stock’s price/fair value ratio. This ratio measures a stock’s most recent closing price against its Morningstar fair value estimate

Stocks with a price/fair value ratio closer to 0.0 are considered undervalued, while stocks with a ratio of 1.0 or higher are viewed as overvalued Morningstar analysts.

Below, we’ve highlighted four stocks that have the highest discount to their fair value ratio among all of the 846 U.S.-listed stocks covered by Morningstar analysts.

I-Mab

- Economic Moat: None

- Discount: 88%

“I-Mab Biopharma is a clinical-stage Chinese biotech firm with strong innovative products in its pipeline. Its first commercial drug will be felzartamab (CD38, Greater China), which could be launched in China at the end of 2023 or early 2024 for third-line multiple myeloma, or MM. Other core assets are lemzoparlimab (”lemzo,” CD47, Greater China), uliledlimab (“uli,” CD73, global rights), and eftansomatropin (long-acting growth hormone, Greater China). Although we do not award I-Mab a moat due to the early stage of its portfolio, we are impressed with its differentiation and rational design and believe it has a positive moat trend.

— Jay Lee, senior equity analyst

Altice USA

- Economic Moat: Narrow

- Discount: 79%

“Altice USA has struggled to maintain revenue growth recently—more than cable peers Comcast and Charter—as it battles stiff competition from Verizon in the New York market. The firm has broken from its peers with plans to aggressively upgrade its networks with fiber rather than rely on traditional cable network technology. This strategy will sharply curtail free cash flow over the next few years. Still, we expect the firm’s networks will remain vital pieces of infrastructure that will generate strong, albeit slow growing, cash flow over the long term.”

— Michael Hodel, director of equity research, media and telecom

Lyft

- Economic Moat: Narrow

- Discount: 78%

“While Lyft’s mixed third-quarter results and fourth-quarter guidance were disappointing, we continue to see strength in the firm’s network effect which has driven growth in rider monetization. We were also pleased with Lyft’s latest cost-cutting measures. However, we continue to expect lower 2024 adjusted EBITDA than the firm guided for earlier this year. We have lowered our revenue growth assumption for this year through 2026 given the ongoing uncertainty regarding the macro environment.

“In addition, while we think Lyft will remain the second-largest ride-hailing platform in the U.S., we are now assuming Uber will slightly increase its market share over Lyft during the next few years. We now see Lyft hitting GAAP profitability in 2025, a year later than we had initially projected, as we do not foresee as much operating leverage given our lower revenue growth assumption. While adjustments to our model result in a $55 fair value estimate, down from $65, we continue to view shares of this narrow-moat firm as deeply undervalued.”

— Ali Mogharabi, senior equity analyst

Farfetch

- Economic Moat: None

- Discount: 75%

“Farfetch is a leading global online distribution platform for personal luxury goods. It connects luxury buyers and sellers and offers a wide selection of products to consumers (3.9 million stock-keeping units at the end of 2017, or 10 times more than the next biggest peer, according to the company) without exposing itself to unsold inventory risk. While we believe Farfetch’s business model exhibits traces of a network advantage moat source, we are currently wary of assigning it a moat, given the early stages of industry development, the company’s small size and reach (6% share of the online luxury goods segment, reaching less than 1% of the luxury buying population), and lack of business model monetization.”

“We believe Farfetch is well-positioned to take advantage of strong growth in online luxury good buying, which we expect to increase to 35% in 2030. We expect Farfetch to increase its market share to 10% from 6% in 2021 in 10 years’ time. We forecast the company to turn profitable by 2023 and reach a high-teens margin by 2028 as operating expenses are scaled against growing revenue.”

— Jelena Sokolova, senior equity analyst

Morningstar Disclaimers:

The opinions, information, data, and analyses presented herein do not constitute investment advice; are provided as of the date written; and are subject to change without notice. Every effort has been made to ensure the accuracy of the information provided, but Morningstar makes no warranty, express or implied regarding such information. The information presented herein will be deemed to be superseded by any subsequent versions of this document. Except as otherwise required by law, Morningstar, Inc or its subsidiaries shall not be responsible for any trading decisions, damages or losses resulting from, or related to, the information, data, analyses or opinions or their use. Past performance is not a guide to future returns. The value of investments may go down as well as up and an investor may not get back the amount invested. Reference to any specific security is not a recommendation to buy or sell that security. It is important to note that investments in securities involve risk, including as a result of market and general economic conditions, and will not always be profitable. Indexes are unmanaged and not available for direct investment.

This commentary may contain certain forward-looking statements. We use words such as “expects”, “anticipates”, “believes”, “estimates”, “forecasts”, and similar expressions to identify forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason.

The Report and its contents are not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject Morningstar or its subsidiaries or affiliates to any registration or licensing requirements in such jurisdiction.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from Morningstar, Inc. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. Any decision to invest should always be based upon the details contained in the Prospectus and Key Investor Information Document (KIID), which may be obtained from MeDirect Bank (Malta) plc.