Jean Bovin – Head of BlackRock Investment Institute, together with Wei Li – Global Chief Investment Strategist, Ben Powell – Chief Investment Strategist for APAC, and Nicholas Fawcett – Macro Research all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Brighter backdrop: We see the outlook brightening for Japanese stocks vs. developed peers given fewer supply constraints, supportive monetary policy and corporate reforms.

Market backdrop: Developed market (DM) short-term bond yields rose last week after the Bank of England hiked rates again. We see central banks compelled to hold policy tight.

Week ahead: We’re gauging U.S. consumer spending and inflation in the PCE data out this week. We expect to see still-persistent inflation in U.S. and euro area data.

We see the outlook brightening for Japanese stocks and are rethinking our modest underweight that is currently in line with other DMs. We initially saw risks if the Bank of Japan (BOJ) scrapped its cap on government bond yields to curb inflation. We now believe inflation is unlikely to stick due to fewer supply constraints. So the BOJ may opt to keep policy loose to sustain above-target inflation. Plus, corporate reforms are spurring a shareholder-friendly shift – a key development this year.

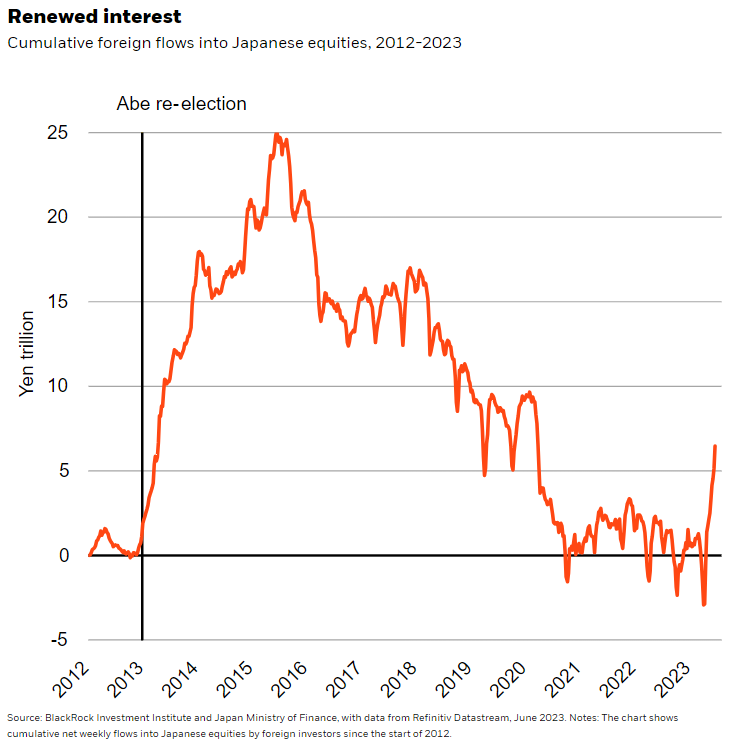

We’ve seen some investors get excited about foreign investment in Japanese stocks surging since April (see the dark orange line in chart), a reversal from the lackluster interest of recent years. There have also been questions about whether enthusiasm may be overdone. We believe assessing the change calls for a longer-term perspective – looking back more than a decade ago when then Prime Minister Shinzo Abe introduced his “three arrow” approach to structural economic reform. Investment in Japanese equities began to slide in late 2015 as the initial euphoria over monetary policy, fiscal policy and corporate reforms faded – especially as the corporate reforms took time to pan out. Global investor interest has picked up in recent weeks, but the uptick does not come close to offsetting the outflows since 2015. What’s reviving foreign investor interest? A more shareholder-friendly approach by Japan’s companies and loose monetary policy not unwinding quickly.

Case in point: The Tokyo Stock Exchange has asked companies that are trading under their book value to publish plans “as soon as possible” on lifting their stock prices. The exchange specifically called for better balance sheet management as many companies hoarded cash over the past decade. We think it makes sense for companies to deploy this cash by investing in growth opportunities or buying back shares now that the growth outlook has improved and inflation has returned. We see this as a potentially pivotal moment for Japan: Roughly half of its companies trade below book value and roughly half have cash on their balance sheets after subtracting liabilities, Refinitiv data shows. Signs companies are complying may appear in coming weeks during Japan’s annual shareholder meeting season. Plus, Japanese investors could be the next key buyers thanks to tax incentives starting in January 2024 that encourage savers to shift their money from cash into investments.

Japan’s policy picture

On the macro front, the BOJ’s efforts to raise inflation – after a long battle with deflation – are a stark difference from other DM central banks that are still hiking rates to deal with stubborn inflation. We thought the BOJ would be forced to scrap its yield cap and quickly tighten monetary policy because inflation surged above its 2% target. We saw risks that getting rid of the cap would push up global yields and reduce risk appetite. That’s why we went underweight Japanese stocks in February on our tactical horizon of six to 12 months, in line with our underweight to other DM stocks. Yet now we think the BOJ will be slow to tighten monetary policy, even if it alters its yield cap as it has signaled it will in coming months.

Why? Japan’s inflation has picked up sharply, partly due to the energy crunch as the West tried to wean itself off of Russian supplies. The impact did not hit Japan’s economy as hard as Europe and has since faded as energy prices fell, reducing the drag on incomes. Import prices have also started to cool. Other inflation drivers are easing, too: Wage gains have fizzled since the end of 2022. Japan’s labor market does not face the same constraints as in other DMs and has room to grow without stoking inflation. We see the BOJ being more cautious in tightening policy to ensure inflation has become embedded.

Bottom line

The BOJ likely winding down its ultra-loose policy slowly and corporate reforms differentiate Japan’s stocks from DM peers, we think, even as we stay cautious on DMs overall. We see higher inflation spurring households to search for better returns instead of hoarding cash, especially as incentives for stock investment are rolled out. Japanese investors may bring money back home if bond yields rise with changes to the BOJ’s yield cap. We think foreign investors could consider unhedged Japanese equity exposures to benefit from any yen strength. We see the BOJ intervening again if the yen weakens too much.

Market backdrop

DM short-term bond yields rose last week even as equities lost some steam. The Bank of England raised rates by more than the market expected, pinning the two-year gilt yield near 15-year highs. The Swiss and Norwegian central banks also hiked. We think central banks are being compelled to hold policy tight as inflation remains persistent. We see a tighter policy era ahead – and expect that to reinforce the new regime of greater macro and market volatility.

We’re gauging U.S. consumer spending and inflation in the PCE data out this week. Euro area inflation is also in focus. We see major central banks keeping interest rates higher for longer to fight sticky inflation driven by supply constraints. We expect core inflation to stay above policy targets for some time.

Week Ahead

June 26: Germany Ifo business survey

June 27: U.S. consumer confidence

June 30: U.S. PCE; euro area inflation; China manufacturing PMI; UK GDP

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 26th June, 2023 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.