Jean Boivin, Head of the BlackRock Investment Institute together with Wei Li, Global Chief Investment Strategist, Alex Brazier, Deputy Head of the BlackRock Investment Institute and Nicholas Fawcett, all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points:

Rate hike expectations: Central banks have primed markets to expect too many rate hikes in the face of persistent inflation, in our view. This keeps us neutral on stocks in the short run.

Market backdrop: The U.S. added 390,000 jobs in May – a number that was matched by new entrants to the labor force. This shows the labor market is not as tight as feared.

Week ahead: The European Central Bank (ECB) this week is set to give more clues about its rate path. U.S. inflation data could provide crucial inputs for the Fed’s rate hikes.

The Federal Reserve signaled its focus is on taming inflation without flagging the big economic costs this will entail. As long as this is the case and markets believe it, we don’t see the basis for a sustained reThe ECB is set to confirm this week that rate increases are imminent, and markets expect it to hike well into 2023. The Fed is seen to reach peak rates at this year’s end. The sum total of rate hikes will ultimately prove to be historically low, we believe, as central banks choose to live with inflation rather than squash growth. The problem: Markets have been primed to assume hawkish intent and are quick to perceive risks of overtightening. This keeps us neutral on equities in the short run.

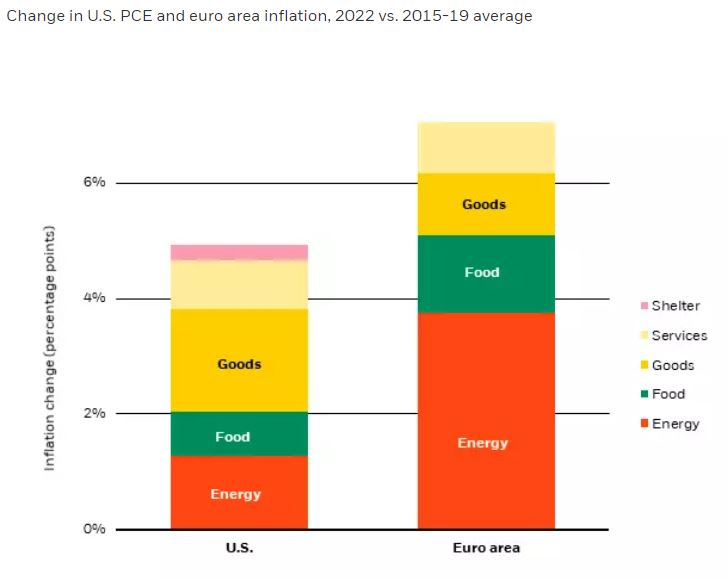

Same high inflation, different drivers

The ECB and the Fed both need to quickly normalize policy from the emergency settings adopted when the pandemic first hit. And they both face inflation that’s running at multi-decade highs – and are feeling pressure to rein it in. The difference: the drivers of inflation. Inflation in the euro area is driven primarily by higher energy and food bills that were exacerbated by the tragic war in Ukraine. See the red and green shaded areas in the bar chart on the right. This should dissipate in the medium term, in our view, as Europe finds new energy and food sources. In the U.S., inflation is more broad-based, with increases driven by goods and energy in almost equal parts (the left bar). We see U.S. inflation as persistent and expect it to settle at higher levels than pre-Covid.

We have entered an era where production constraints have become the dominant drivers of inflation. Think about bottlenecks and difficulties in producing, sourcing, transporting and staffing. Both central banks have yet to acknowledge the sharp trade-off when trying to rein in this type of inflation with rate hikes: Squash growth and jobs or live with higher inflation than before the pandemic. We don’t see a goldilocks outcome where inflation stays near 2% while unemployment remains low and growth resumes an upward trend. This leaves the door open for markets to expect overtightening at any signs of persistent inflation, a tight labor market or economic strength – and keeps us neutral on equities in the short run.

A new inflation era

The situation is most acute in Europe. Markets expect the ECB to hike rates well into 2023 to rein in inflation that was running at an annual clip of 8.1% in May. Instead, we see it quickly raising rates out of negative territory but then pausing in the face of a recession triggered by Europe’s 1970s-style energy crisis. Last week’s decision by the European Union to ban most Russian crude oil imports is the latest example of how the West is determined to wean itself off Russian energy. This is pushing up oil prices and dragging down growth. We see a material slowdown in euro area economic activity as a result. This should do much of the ECB’s work for it. Conclusion: We believe market expectations for ECB rate hikes are overly hawkish.

Market pricing of Fed rate hikes has cooled recently on market expectations that inflation is bound to come down. This spurred a rebound in equities from 2022 lows and stopped the U.S. dollar rally in its tracks. In other words, markets have moved as if inflation is yesterday’s story. We disagree. Sure, core inflation is bound to come down from 40-year highs. But we see it as persistent and running above the Fed’s 2% target for years to come. We see short-term risk of a snap back in the market’s rate expectations as data show the persistence of inflation – and as the Fed keeps talking tough on inflation.

Where this leaves investments

What does this mean for investments? The volatile macro and market landscape is here to stay, in our view. We believe central banks will ultimately deliver a historically muted response to inflation. That underpins our core strategic view of preferring equities over government bonds. We have less conviction on a tactical horizon of six to 12 months. This is why we have gradually trimmed risk all year and downgraded DM equities to neutral last month. We are looking for signs that central banks acknowledge the trade-off of living with some inflation for the sake of preserving growth. We could see another sharp policy pivot in the coming months, this time a dovish one. This would be a catalyst to go back to overweight equities.

Bottom line

What does this mean for investments? The volatile macro and market landscape is here to stay, in our view. We believe central banks will ultimately deliver a historically muted response to inflation. That The sum total of rate hikes will prove to be historically low, we believe, as central banks choose to live with inflation. But markets are primed to perceive a risk of overtightening. This is why we are neutral on stocks in the short run.

Market backdrop

The U.S. added 390,000 jobs in May – a number that was matched by new entrants to the labor force. This shows the labor market is not as tight as is commonly thought. The data triggered a fall in stocks and rise in yields, illustrating the market is conditioned for an overly hawkish Fed. A macro landscape shaped by production constraints is volatile, we think – and more so with central banks that appear oblivious to the sharp trade-off they are facing: live with higher inflation or squash growth.

The ECB’s media briefing is this week’s key event after ECB President Christine Lagarde indicated rate hikes will kick off in July. We think the market’s pricing of the ECB rate path is too aggressive and see the ECB pausing its hiking cycle amid materially weaker growth. U.S. consumer price inflation could inform the Fed’s rate path in coming months.

Week Ahead

- June 6 – 8: China services PMI; India, Poland policy meetings

- June 9: China trade data; ECB policy meeting

- June 10: U.S. and China inflation data

- June 11: China credit and money data

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of April 25th, 2022 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Investor Information Document (KIID), which may be obtained from MeDirect Bank (Malta) plc.