Wei Li – Global Chief Investment Strategist of BlackRock Investment Institute together with Vivek Paul – Global Head of Portfolio Research, Tara Lyer – Chief U.S. Macro Strategist and Filip Nikolic – Macro Research all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Our mega force lens: Geopolitical risk has escalated in the Middle East. The flare-up of tensions in the region and brief market fallout underscore that mega forces affect returns now.

Market backdrop: U.S. stocks rose last week on mostly strong Q1 earnings for mega cap tech. The Federal Reserve’s preferred inflation metric rose more than expected in March.

Week ahead: This week, we watch U.S. payroll data for signs that immigration is still offsetting adverse demographics. The Federal Reserve is expected to hold rates steady.

We have long viewed the world through the lens of mega forces, or big structural shifts. They help explain macro and market outcomes not only long term, but right now. Geopolitical fragmentation is one of five mega forces we track. The strikes between Israel and Iran – and the market response – are one example of how mega forces impact returns now. Most of these mega forces create supply constraints. Yet a productivity boom from artificial intelligence could ease these constraints.

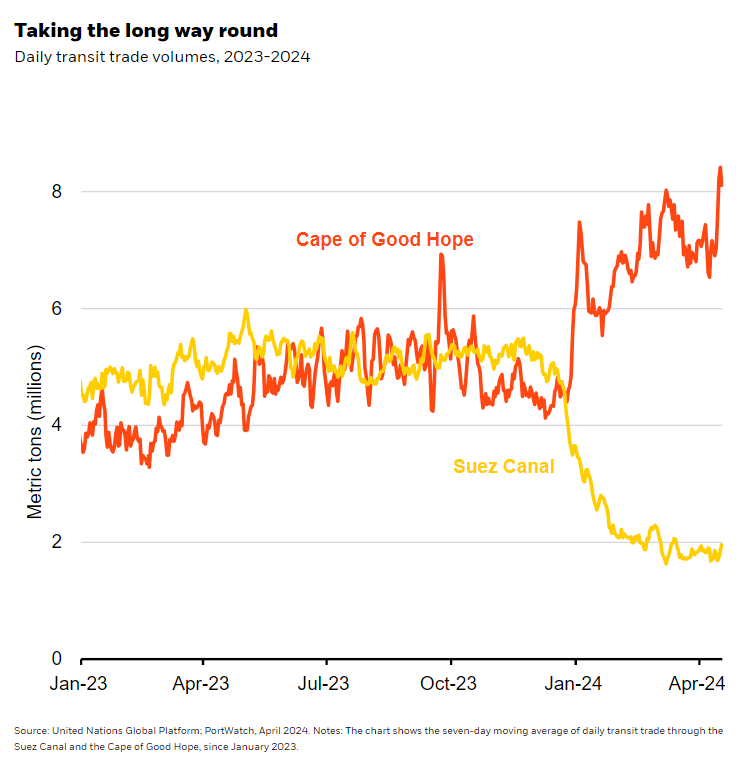

We see escalating tensions in the Middle East as a sign we’re in a new geopolitical regime. The first direct strikes between Israel and Iran structurally raise risk in the region, in our view. The strikes come as Iran has used proxy attacks by the Houthi rebels on ships in the Red Sea as a response to the war in Gaza. These attacks upended supply chains, diverting swathes of goods from the Suez Canal to the Cape of Good Hope. See the chart. Since the attacks began, shipping costs from China are still up about 75% from the end of last year, LSEG Datastream data show. Persistent supply constraints that keep inflation and interest rates above pre-pandemic levels are an upshot of our mega force view. The International Monetary Fund’s recent discussions on the growth impact of structural challenges – like geopolitical risk and other mega forces – reflect similar thinking to ours.

Since we rolled out our mega forces framework last year, we have seen more evidence that these forces are a useful investment lens. We think the geopolitical turmoil in the Middle East has lowered the bar for escalation in the region – upping the chances of persistently higher oil prices. Commodity shocks reinforce why governments are prioritizing energy security and affordability alongside decarbonization. The recent events show traditional energy still has its place, even in the low-carbon transition – and can be a buffer against geopolitical risk.

Supply constraints at work

Population aging is another example of supply constraints playing out in real time. Shrinking working-age populations in developed markets are limiting productivity and output. An unexpected jump in immigration in the U.S. and other major economies offsets the impact of a dwindling domestic workforce for now. Yet we find this effect must persist for some time to outrun adverse demographics. We look to this week’s U.S. payroll data for signs immigration is still supporting labor markets.

A resilient U.S. jobs market marked by persistent wage gains is keeping services inflation elevated. Markets now expect fewer than two Federal Reserve rate cuts in 2024, down from seven earlier this year. Higher-for-longer rates could keep squeezing bank deposits, where interest rates have lagged the Fed policy rate – unlike yields on money market funds. Plus, banks face stricter regulations. We like private credit – where default rates have fallen three quarters in a row – over public on a strategic horizon of five years and longer. Private markets are complex, with high risk and volatility, and aren’t suitable for all investors.

One mega force that could ease supply constraints? AI. We think AI could deliver strong efficiency gains across sectors. We watch for AI adoption to broaden beyond tech – into sectors like healthcare, communication services and financials, and into applications like data centers and infrastructure. We see a high bar for Q1 mega cap tech earnings to beat lofty expectations. Early results have skewed positive – yet any signs of weakness could trigger a change in our U.S. stock view.

Our bottom line

Mega forces provide a useful investment lens now, not just in the future, we think. We like energy stocks as a buffer against geopolitical risk. We prefer private credit over public on a strategic horizon. We stay overweight the AI theme.

Market backdrop

The S&P 500 broke a three-week losing streak last week and rose 3%, while U.S. 10-year Treasury yields hit new 2024 highs. The Federal Reserve’s preferred inflation metric rose more than expected in March, supporting our higher-for-longer interest rate view. U.S. mega cap tech led a strong start to Q1 earnings – we think sticky inflation raises the bar for earnings to keep delivering and supporting sentiment. The Bank of Japan kept rates steady as expected, driving the yen to a new 34-year low.

The Fed policy decision, U.S. wage and payrolls data are in focus this week. The Fed is widely expected to hold interest rates steady at this week’s meeting, and we look for signs of how the Fed has dialed back its own projections for three rate cuts this year. One important input for the Fed: the Q1 ECI, its preferred wage gauge. We eye signs of wage pressures easing and the potential knock-on effect on inflation. The payrolls data rounds out a busy week.

Week Ahead

April 30: U.S. ECI wage data; euro area flash inflation and Q1 GDP

May 1: Fed policy decision

May 2: U.S. trade data

May 3: U.S. payrolls data

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 29th April, 2024 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.