Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Ann-Katrin Petersen – Chief Investment Strategist for Germany, Austria, Switzerland and Eastern Europe and Filip Nikolic – Macro Research all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

High for longer: We see inflation limiting how much central banks can cut interest rates. We like U.S. stocks over Europe’s as they benefit from the artificial intelligence theme.

Market backdrop: Markets remain sensitive to Federal Reserve policy signals and its rate path, helping lift the VIX index of implied S&P volatility from four-year lows last week.

Week ahead: Markets will be parsing signals for future rate cuts by the European Central Bank (ECB) and updated macro forecasts at the policy meeting this week.

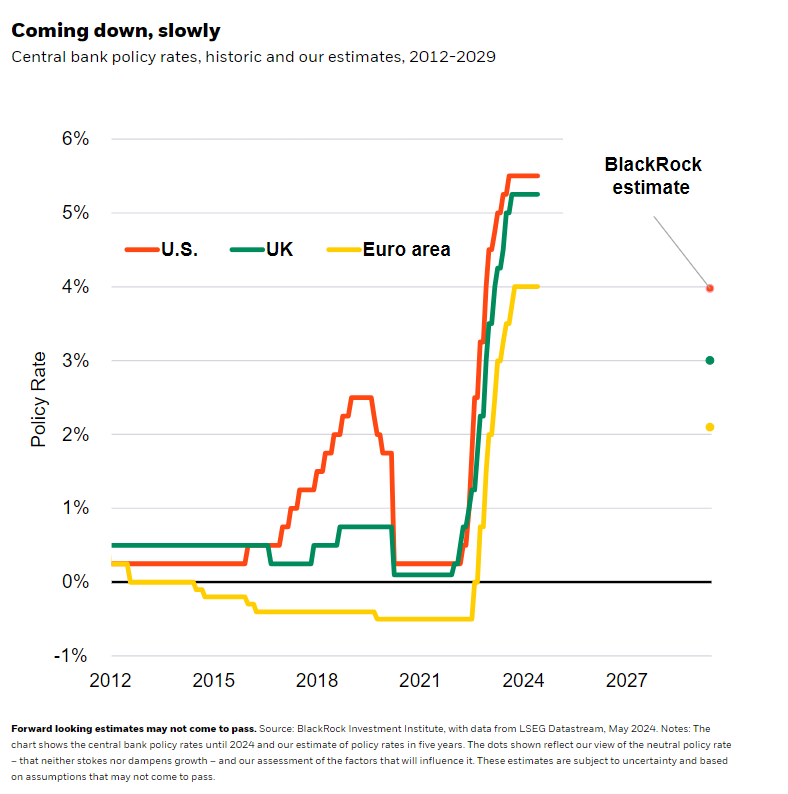

Major central banks are gearing up to cut interest rates. But like their hiking cycles, this cutting cycle will be far from typical, we think. Why? The ECB is set to start easing before the Fed, but a wider policy gap between them will be temporary, in our view, even if a Fed hike is not impossible. Central banks are eyeing rate cuts with inflation still above 2% and growth strong or improving. We see them keeping rates high for longer. We prefer U.S. stocks over Europe because of the AI theme.

European government bond yields have swung as markets question how far the ECB will ease policy beyond a first cut expected this week. Falling inflation and 18 months of weak economic activity make the case for the ECB to start cutting rates. But we don’t think it will cut far and fast. Likewise in the U.S., we see just one or two Fed cuts this year. This is not your typical rate cutting cycle. Central banks are set to keep rates above pre-pandemic levels (see the dots in the chart) due to persistent inflationary pressures – and last week’s euro area inflation data again showed stalling inflation progress. Unusually, the ECB is readying to cut when growth is improving, inflation is above its 2% target and the unemployment rate is at a record low. That’s a far cry from the economic crisis and low inflation in the past decade that spurred the ECB to introduce negative interest rates and buy bonds at scale.

In another unconventional step, the ECB is on the verge of easing policy before the Fed – and before it’s certain what’s next for monetary policy in the U.S., in our view. U.S. inflation is proving volatile and services inflation especially elevated, so another rate hike is not entirely off the table. This means that in the short term, the gap between Fed and ECB policy rates could widen and weigh on the euro against the U.S. dollar until the Fed starts cutting rates. Investors may see opportunities in further policy divergence, but we think it will be temporary as both central banks ultimately keep rates high for longer.

Supply constraints in play

Even with anticipated rate cuts, we see policy rates in the U.S. and Europe settling at a far higher level than they were pre-pandemic. The reason: inflation. We don’t see euro area inflation falling below 2% as it did when central banks cut rates before 2020. That’s because we are in a world shaped by supply constraints – a reality ECB officials have acknowledged recently. Among those constraints are mega forces – structural shifts driving returns now and in the future – like geopolitical fragmentation, demographic divergence and the low-carbon transition. Those forces are also playing out in the U.S. As a result, we expect ongoing inflationary pressures and structurally lower growth than in the past across major economies.

The ECB trimming rates and recovering euro area growth should favor European stocks. Yet we are underweight, preferring U.S. stocks on a tactical, six- to 12-month horizon as they are set to get a bigger boost from mega forces like AI. Within fixed income, our preference flips. We scoop up the higher total yields on offer in euro area credit. Improving growth in the euro area could also limit any spread widening relative to the U.S. We are neutral euro area government bonds and UK gilts as market pricing of near-term rate cuts aligns with our view. We see support for European bonds due to smaller fiscal deficits than in the U.S. Rules on limiting deficits now apply again after being suspended during the pandemic. We await the results of the European parliamentary election in June and UK general election in July – but expect a muted impact on bonds.

Our bottom line

An ECB cut is unlikely to be the start of a meaningful global easing cycle. We favor U.S. stocks over Europe’s on stronger corporate earnings and the AI theme. We’re neutral European government bonds but get income in European credit.

Market backdrop

U.S. stocks receded last week from record highs. Markets remain sensitive to Fed policy signals and the path of interest rates, helping lift the VIX index of implied S&P volatility from four-year lows. U.S. 10-year Treasury yields ticked up – partly due to weak Treasury auctions. German 10-year bund yields set fresh 2024 highs last week and sit near 2.64%. Ultimately, we see supply constraints creating persistent inflation pressure, keeping policy rates above pre-pandemic levels and growth below.

Markets will be parsing signals for future ECB rate cuts from its updated macro forecasts and President Lagarde’s press conference this week. We see the expected June 6 cut as the start of an atypical easing cycle as central banks keep interest rates high for longer. In the U.S., we rely on data – like this week’s employment report and service-sector PMI reading – rather than Fed signals to determine the policy path.

Week Ahead

June 4: U.S. job openings

June 5: U.S. ISM non-manufacturing PMI; China Caixin services PMI

June 6: ECB policy decision; U.S. international trade data

June 7: U.S. employment report; China trade data

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 3rd June, 2024 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.