Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Ben Powell – Chief Investment Strategist for APAC and Devan Nathwani – Portfolio Strategist, all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Cutting through the noise: We see recent market volatility tied to near-term sentiment shifts rather than corporate earnings and macro data. We prefer to look through these air pockets.

Market backdrop: U.S. stocks fell for a second straight week, with the S&P 500 suffering its largest one-day drop since late 2022. Risk assets made up some ground by week’s end.

Week ahead: The Federal Reserve, Bank of Japan and Bank of England all meet this week. The Fed may signal a first cut in September, while the BOJ could hike again.

We’ve argued that markets are vulnerable to sudden risk sentiment shifts over short periods as has played out recently. Hopes for more Federal Reserve rate cuts, combined with another potential Bank of Japan hike, led to a yen surge and knock-on effects. Yet these Fed rate cut hopes have not driven a broad risk rally. Instead, we’ve seen markets grapple with tech’s return potential on artificial intelligence (AI) – and this is driven more by sentiment than earnings prospects, in our view.

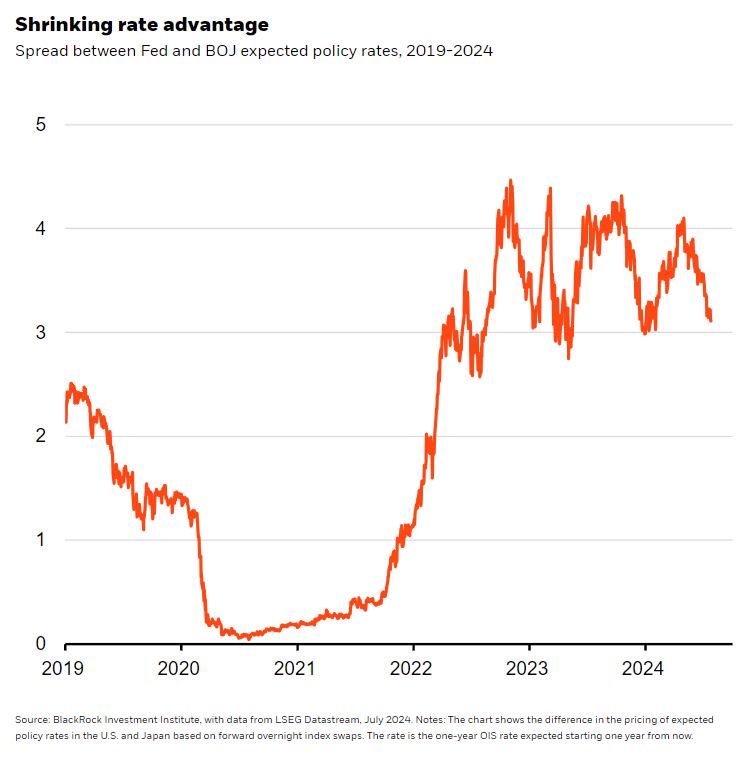

The market volatility comes as the Fed could this week signal a first policy rate cut in September and markets are pricing in multiple cuts through next year. Pricing of Fed rate cuts should have been positive for U.S. risk assets – and yet last week the S&P 500 suffered its worst daily session since 2022. Stocks pulling back even as markets price in more Fed rate cuts is a sign momentum trades had run too far and were poised for a short-term reversal – and markets are still extrapolating too much from near-term macro news, as we have argued. The BOJ could hike for a second time this year Wednesday. That means the gap in Fed and BOJ expected policy rates, a big driver in the yen’s drop to a 35-year low, is narrowing. See the chart. The yen’s resulting surge caused investors to unwind positions using the low-yielding yen to buy higher-yielding currencies – what’s known as the carry trade.

One sign of yen-funded carry trades coming under strain: As the yen surged this month, leveraged funds closed their short- yen positions – used to fund a carry trade – at the quickest pace since 2011, CFTC data show. Such a sharp unwind may have been a technical factor driving some of the market volatility and air pockets. The yen’s popularity as a funding currency can cause knock-on effects in other markets, helping tighten global financial conditions. Technical factors like thinner trading activity in the northern hemisphere summer, the two-week buyback blackout period ahead of Q2 earnings and stretched positioning in U.S. equities have likely amplified these effects. We avoid getting caught in short-term crosscurrents by sticking to our framework. We don’t see the BOJ driving further sharp yen gains and expect it to go slow in normalizing policy.

Reassessing risks

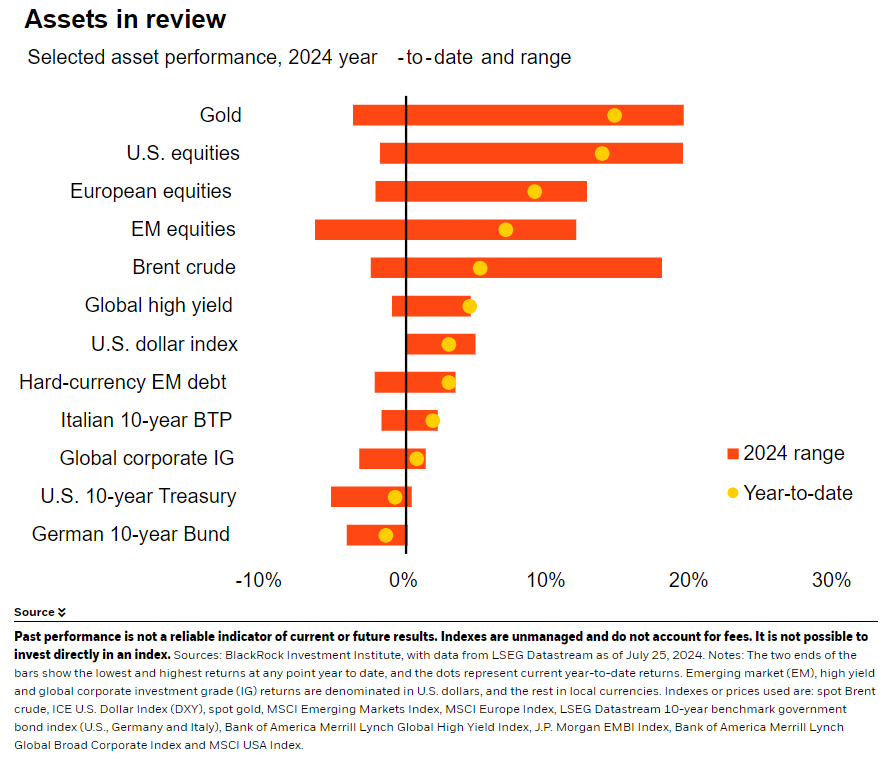

The carry trade unwind is just one part of a broader global risk reassessment, in our view. Market sentiment has shifted on AI companies in the spotlight. Tech shares have retreated in recent weeks on concerns over further U.S. restrictions on chip exports to China and questions about the future returns major tech companies will achieve on their heavy AI investment. We had warned the outsized performance of AI winners made them susceptible to near-term pullbacks. Yet we still see AI supported by strong earnings. More broadly, Q2 corporate earnings have topped expectations so far, with S&P 500 earnings growth projected at about 13%, above the 9% expected at the start of the season, LSEG Datastream data show.

Bouts of volatility like we’ve seen are a defining feature of the new macro and market regime, we think. We eye opportunities that hinge on the real economy. The recent upside surprise in U.S. Q2 GDP growth, supported by capital spending on AI – on top of the investment in buildings and infrastructure tied to earlier policy incentives such as the CHIPS Act – is a sign of the transformation underway, in our view. We’re focusing on potential policy changes in the upcoming U.S. election, with Vice President Kamala Harris now set to be the Democratic candidate taking on former President Donald Trump in November.

Bottom line

We see central bank policy expectations, equity factor rotations and currency moves driving the recent market volatility. We caution against extrapolating from these moves. We key on earnings and the real economy for opportunities.

Market backdrop

U.S. stocks fell for a second straight week, led by technology names. The rotation into smaller companies carried on due to jitters about whether big tech firms can deliver on their heavy AI investment. We think the disconnect between stocks and U.S. 10-year Treasury yields – holding around 4.21% – reveal momentum and technical factors at work. We have expected spurts of near-term volatility as markets grapple with uncertainty on many fronts. The Japanese yen surged versus major currencies.

Central banks take center stage this week as the Fed, BOE and BOJ meet. Markets will be parsing signals for future Fed rate cuts this year, as Chair Jerome Powell has hinted cuts could come before inflation hits the 2% target. We think falling inflation has made a September cut more likely. Markets are torn on whether the BOE will cut this week. Even if central banks start to ease policy, we expect higher-for-longer rates due to persistent inflation pressures.

Week Ahead

July 30: U.S. consumer confidence; euro area GDP

July 31: Fed policy meeting; BOJ policy meeting; euro area inflation

Aug. 1: Bank of England (BOE) policy meeting

Aug. 2: U.S. payrolls data

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 29th July, 2024 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.