Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Nicholas Fawcett – Senior Economist, and Filip Nikolic – Macro Research all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Higher for longer: Recent macro data reinforces our view that the Fed will not cut rates as much as markets expect. Weaker euro area activity gives the ECB more room to loosen.

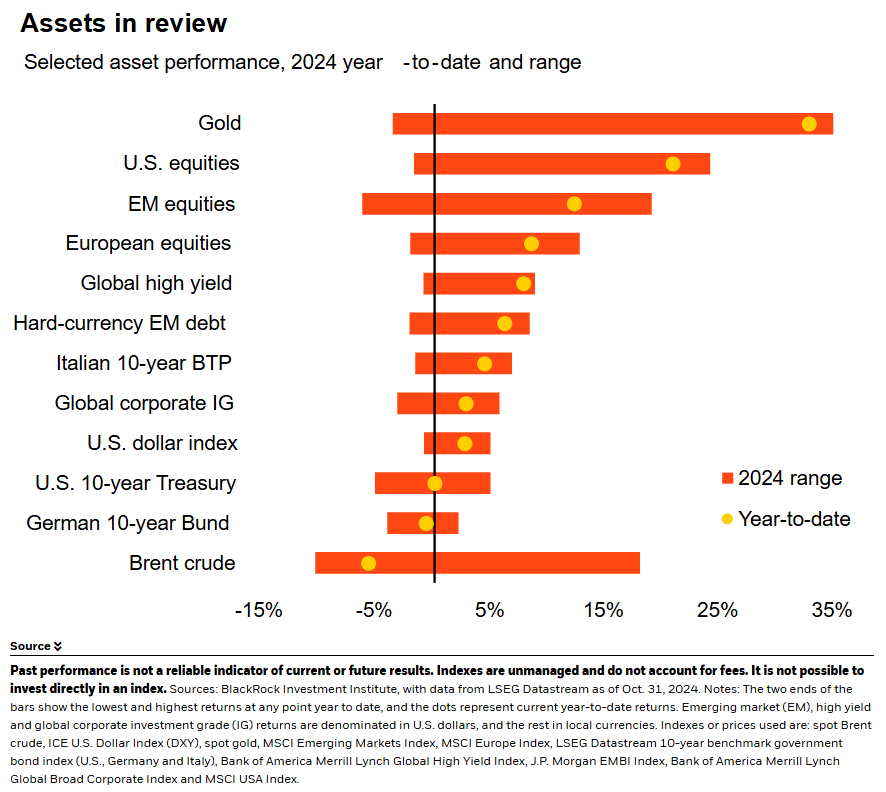

Market backdrop: Mixed corporate earnings results and guidance from mega cap tech companies hurt U.S. stocks last week. U.S. 10-year Treasury yields hit four-month highs.

Week ahead: The Fed and Bank of England are both poised for another 25-basis point cut this week. We still think U.S. rates will settle slightly higher than markets expect.

With the Federal Reserve poised to cut policy rates again this week, recent solid jobs and wage data – including last week’s updates – reinforce why we do not see the central bank delivering the lower rates markets expect. We think investors are viewing structural changes through the lens of a typical business cycle – and that is driving market volatility. The European Central Bank is seen cutting rates closer to our view, one reason we prefer euro area fixed income over the U.S.

We have seen huge swings in Fed rate cut pricing this year as markets struggle to put incoming – and often conflicting – macro data in context. The U.S. economy’s unexpected recent resilience led markets to price out some rate cuts. But we do not think this is a typical business cycle. The unwind of pandemic-era supply shocks and a temporary immigration boost explain much of inflation’s cooling, in our view. That is why U.S. wage growth cooled from near 6% annually in early 2022 to around 3% now. See the chart. Yet last week’s labor data show wage growth is still strong, and current levels suggest core inflation could stay nearer to 3% versus the Fed’s 2% target. We see mega forces, structural shifts driving returns now and in the future, at play that could keep inflation sticky longer term – notably an aging population that would limit labor supply and future growth.

A still-thriving economy – even as the Fed has only just started cutting rates – has spurred markets to price out some cuts. Futures markets now show policy rates settling around 3.7% by the end of 2025, up from 2.8% in September, LSEG Datastream data shows. Yet markets are pricing in more Fed cuts than the central bank is likely to deliver, in our view.

Inflationary forces

Why? We see inflation staying higher than pre-pandemic levels. U.S. Q3 GDP data last week showed consumer spending is still driving overall economic growth. Average monthly job creation over the past three months now stands at 104,000 after last week’s jobs report – still a healthy pace and one likely to pick up given hiring stalled due to hurricane-related disruptions. As the U.S. election occurs, neither presidential candidate is focused on budget deficits that are likely to stay large no matter who wins. The prospect of higher tariffs or reduced legal immigration would also have inflation implications. Population aging and other mega forces are inflationary, too. Massive capital spending and reallocation from the artificial intelligence buildout may spur inflation, as could increasingly complex global supply chains due to geopolitical fragmentation.

Market pricing of ECB rate cuts is more in line with our view than in the U.S. The ECB tightened by more than the Fed on the way up – 450 basis points from January 2020 to the peak versus 375 for the Fed. ECB policy looks even tighter given Europe’s weaker consumer spending and limited fiscal support compared with the U.S. Tight policy gives the ECB more room than the Fed to cut rates to jump-start growth. That is why the ECB sped up the pace of easing in cutting rates a third time last month, making each policy meeting a live one. We see the ECB cutting to around 2%, consistent with market pricing. This drives our preference for European fixed income over the U.S., especially in credit. UK bond markets are eyeing the potential inflation impact of the tax and spending mix in the UK’s new budget. We see a tepid UK growth outlook driving the Bank of England to cut more than markets have priced in. That is why we recently went overweight UK gilts.

Our bottom line

This is not a typical business cycle. We see structural forces holding inflation higher long term, keeping the Fed from cutting as much as markets expect. ECB rate cut pricing is closer to our view, one reason we prefer euro area bonds.

Market backdrop

U.S. stocks slipped last week, with tech leading the way down after some mega cap tech companies failed to deliver on high expectations for earnings guidance. Tech’s troubles and weak U.S. payrolls for October overshadowed strong U.S. Q3 GDP growth fueled by resilient consumer spending. U.S. 10-year Treasury yields reached four-month highs near 4.40%. UK 10-year gilt yields hit 11-month highs after the new UK government budget boosted planned borrowing for investment.

Central bank policy decisions are in focus this week. Markets widely expect both the Fed and BOE to cut rates another 25 basis points Thursday and will be watching for clues on the pace of future easing. The UK growth outlook is weaker than in other developed markets, meaning the BOE may cut further than the Fed in coming years, we think. Markets have come closer to our ultimate U.S. rate pricing, yet we still see rates settling higher than markets expect.

Week Ahead

Nov. 5: U.S. trade data

Nov. 7: Fed policy decision; Bank of England (BOE) policy decision; China trade data

Nov. 9: China CPI and PPI

Nov. 8-15: China total social financing

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 4th November, 2024 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.