Jean Bovin – Head of BlackRock Investment Institute, together with Wei Li – Global Chief Investment Strategist, Alex Brazier – Deputy Head, and Nicholas Fawcett – Macro Research all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Eyeing higher yields: Major central banks tightened policy last week, including unexpectedly in Japan. We see the potential for rising Japanese bond yields to pull global yields higher.

Market backdrop: The Bank of Japan tweaked its yield cap, sending local yields to a nine-year high. Developed market stocks hit 15-month highs.

Week ahead: U.S. jobs data this week is likely to show still-low unemployment, confirming a tight labor market. We see weak euro area activity as rate hikes bite.

The Bank of Japan surprised markets last week after it tweaked its yield curve control policy again, joining a tightening wave across developed markets (DM). The Federal Reserve hiked rates and said more could come: It may be overestimating the economy’s strength, we think. By contrast, the European Central Bank signaled an end to its tightening bias and a new phase of data-dependency. We see global yields rising with tighter policy all around and favor European bonds in DM.

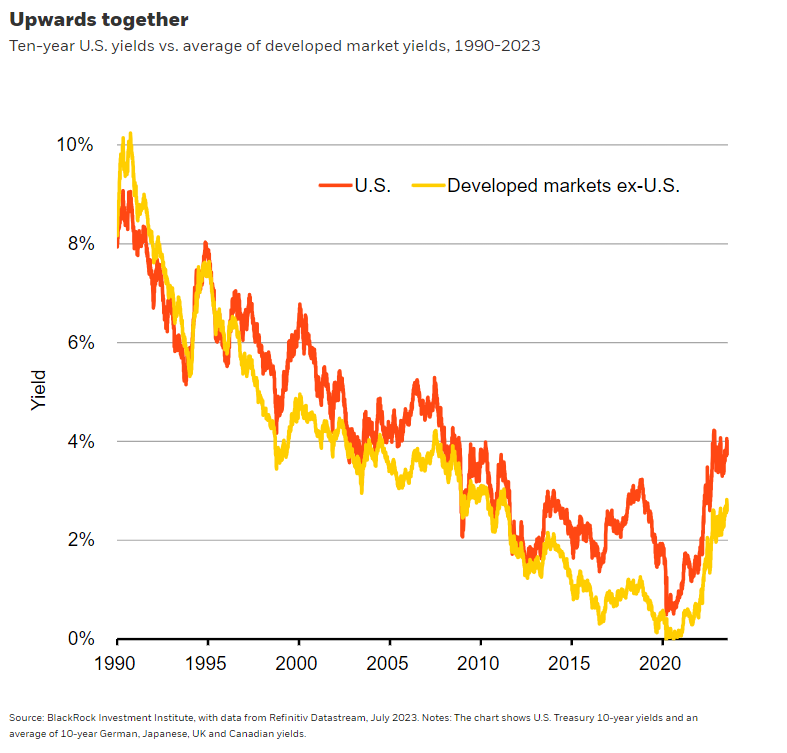

The Bank of Japan (BOJ) took another step last week to wind down stimulus by loosening its policy of capping 10-year bond yields. The shift saw Japanese 10-year yields rise to a nine-year high. Most global yields rose as well, highlighting why the BOJ move matters for markets – the gravitational pull between DM bond yields is strong. Take the 10-year bond yield of U.S. Treasuries and the average DM peer: They have largely moved in lockstep for decades – apart from 2015-2020 when the euro area and Japan were fighting deflationary risks with negative interest rates and hefty bond purchases. See the chart. We think the BOJ’s move to relax its yield curve control is an important development: It is gradually joining the global policy tightening campaign, and in this case policy is about letting long-term government bond yields rise. We see potential further tweaks to BOJ policy pulling up developed market bond yields alongside Japanese ones.

The BOJ unexpectedly shifted its hard yield cap up to 1% from 0.5% but kept the half a percentage point range either side of zero as a “reference point,” allowing flexibility on bond purchases. Inflation has returned but not as much as in other economies – and the BOJ is unsure if higher wages will be sustained and keep inflation around its target. The BOJ is still projecting inflation below target a few years ahead but sees a risk of higher-than-forecast inflation in the interim. We expect the BOJ to let yields rise as inflation gets more entrenched, but only gradually. This is a form of tightening, in our view. It has gone smoothly for now, but we think the muted market response may embolden the BOJ to do more, though it could become trickier. It may be some time before the BOJ lifts short-term policy rates from the current -0.1%.

A different problem

The Fed and ECB have a different problem: Inflation is still too high. Last week’s U.S. PCE inflation and wage data showed a move in the right direction. But we fear an inflation rollercoaster as service price pressures persist – and jobs data this week will be key to assessing the outlook. The Fed, like us, is not yet convinced that inflation is on track to reach its target. It thinks economic weakness is the only way to get there – and sees resilient GDP and consumer spending as signs the demand in the economy is still too strong. We think the Fed may be misreading the economy’s strength based on low unemployment: That shouldn’t be taken as the usual sign of a buoyant economy, but rather a result of structural worker shortages holding back growth potential. We think this perceived strength raises the risk that the Fed hikes more than markets expect and then cuts as it generates too much weakness – rather than just holding tight.

The ECB also believes economic weakness is needed to get inflation down to target. It hiked again last week but signaled an end to its tightening bias and a new phase of data-dependency. The ECB recognizes that it’s already causing damage, as seen in PMIs. Yet we still see it holding policy tight to get inflation right down even as more weakness emerges.

Bottom line

We see the BOJ’s shift confirming why DM yields are likely heading higher as investors demand more term premium for the risk of holding long-term government bonds. We stay tactically underweight long-term bonds but see key regional differences. We tactically prefer euro area bonds to U.S. peers as market pricing better reflects ECB policy staying tight. That view played out this week with euro area yields flat while U.S. and Japanese yields climbed. We stay underweight Japanese bonds given the scope for a further yield rise. We also have a relative preference for high quality credit for income.

Market backdrop

The BOJ’s tweak to its yield cap drove Japanese bond yields to nine-year highs and pulled along some other DM yields, with the U.S. 10-year Treasury yield up 10 basis points on the week to near 4%. The MSCI World index of DM shares edged higher on the week to hit a 15-month high. Mega cap tech firms met a high bar in delivering on expected second quarter earnings. Analysts are eyeing an earnings recovery beyond this quarter, but we expect them to stay under pressure over the next year.

We’re focused on U.S. jobs data this week. We think companies being reluctant to let go of workers in a tight labor market will likely keep unemployment low even as economic activity stagnates. Euro area activity data will likely show further weakness as rate hikes bite. Markets are also leaning toward another hike from the Bank of England this week.

Week Ahead

July 31: Euro area GDP and flash inflation data

August 1: U.S. job openings; euro area unemployment

August 3: Bank of England policy decision; China services PMI

August 4: U.S. payrolls report

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 21st July, 2023 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.