Wei Li – Global Chief Investment Strategist of BlackRock investment institute, together with Alex Brazier – Deputy Head, Ben Powell – Chief Investment Strategist for APAC, and Nicholas Fawcett- Macro Research all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Three big shifts: Recession foretold in developed markets (DM), a pause in central bank rate hikes and China’s reopening help shape 2023 and reinforce our tactical views.

Market backdrop: European equities led DM stocks higher. Surprisingly weak U.S. services data spurred bets for Federal Reserve rate cuts this year, which we think are unlikely.

Week ahead: We see the U.S. CPI slowing as spending shifts back to services from goods, but wage growth will keep core inflation higher than before the pandemic.

We see three shifts shaping 2023 as the new regime keeps playing out. First, we see DM economies facing recession. Second, DM central banks will halt rate hikes when economic damage is clearer. Goods inflation should fall sharply as spending shifts. But we don’t expect rate cuts as inflation stays above policy targets. Third, China’s reopening and domestic spending will drive global growth as DM recessions hit. We like emerging market stocks over DM and like high grade credit.

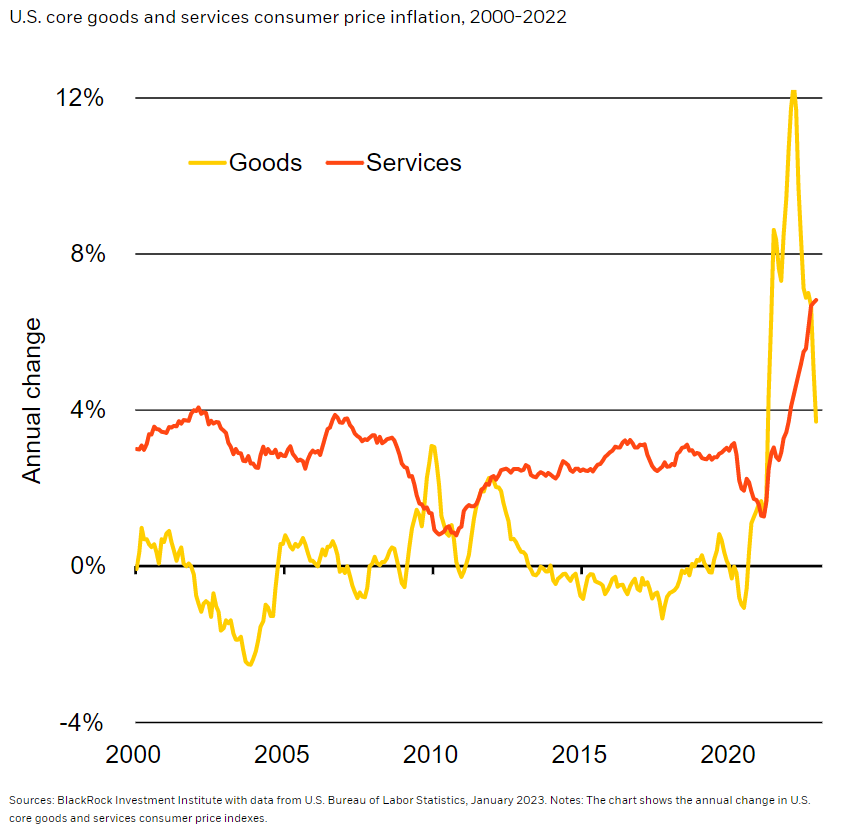

The inflation divide

In 2022, DM economies grew, China growth slowed, and inflation and interest rates surged. In 2023, sharp rate hikes aimed at pushing inflation down to policy targets will cause recessions in DMs – the first shift from last year. We’re already seeing evidence that rate hikes are hurting the most interest-rate-sensitive parts of the economy, like housing. Hikes have an overall lagged effect that will reinforce economic pain from the energy shock in Europe and weigh on U.S. consumers as they exhaust savings. We think recessions will push central banks to pause hikes – the second shift. Inflation is set to fall as U.S. consumer spending rotates to services from goods, dragging down goods inflation (yellow line in the chart). But labor shortages will likely make services inflation stickier (orange line). So we don’t see central banks cutting rates to rescue DMs from recession.

Reduced U.S. labor supply means that companies are having trouble hiring. The December jobs data showed little sign of the situation changing fundamentally, in our view. Wage growth did cool, but labor shortages are still pushing it up to a level that makes achieving central banks’ 2% inflation target unlikely. Getting inflation to settle back at targets would entail reducing labor demand – and would need an even deeper recession than we see ahead. That’s why we see central banks keeping rates higher for longer than markets expect instead of cutting rates. And over the long term, we see three structural trends keeping inflation pressures higher on average than pre-pandemic: aging demographics, geopolitical fragmentation and the transition to net-zero carbon emissions.

The third shift

China is rapidly lifting Covid-19 restrictions. We estimate its economic growth will clock in above 6% in 2023, cushioning the global slowdown as recession hits major DM economies. But China’s growth surge will be tempered by falling demand for its exports as U.S. spending shifts away from goods. We don’t expect the level of economic activity in China to return to its pre-Covid trend, even as domestic activity restarts. We see growth falling back once the restart runs its course.

Our tactical views

These three shifts we see ahead in 2023 reinforce our tactical views and are why we maintain our most defensive stance. Earnings expectations for 2023 are still not fully reflecting the DM recessions we expect, in our view. That’s why we’re underweight DM stocks. We stand ready to turn more positive on DM stocks when more of the economic damage we see ahead is in the price or our assessment of market risk sentiment improves. China replacing the U.S. as the driver of global growth underpins our preference for emerging market equities, including Chinese equities, over DM peers.

Within fixed income, we see more attractive opportunities to earn income in investment grade credit, U.S. mortgage-backed securities and short-term Treasuries. We stay underweight long-term nominal government bonds because they don’t reflect our view that yields will rise further as investors demand more term premium, or compensation for the risk of holding them amid persistent inflation and higher rates.

Our bottom line

2022 was a year of soaring inflation, rapid rate hikes and pandemic-induced lockdowns in China. We see volatility ahead in 2023 but expect the year to be shaped by big shifts from last year: recessions in developed markets, inflation falling and central banks pausing their rate hikes, and China reopening. We’ll likely turn more positive on risk assets after gauging what’s in the price and market risk sentiment – a central theme of our new investment playbook.

Market backdrop

European equities led gains in DM stocks this week. Ten-year German bund yields led a drop in major government bond yields. Falling energy prices are helping pull down headline inflation and fanning hopes for less hawkish DM central banks. A sharp drop in the U.S. services PMI spurred expectations for Fed rate cuts next year. But we see sticky core inflation keeping central banks on track to overtighten policy – and keep policy rates higher than markets are expecting.

We expect the annual change in the U.S. CPI to slow again in December, falling from the 40-year highs reached in 2022 as spending normalizes back to services from goods – putting pressure on goods prices – and thanks to lower energy prices. But sticky wage growth due to labor shortages is likely to keep core inflation sticky and the Fed on track to keep hiking rates

Week Ahead

Jan. 10-17: China total social financing

Jan. 12: U.S. CPI

Jan. 13: UK GDP; U.S. University of Michigan consumer sentiment

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 9th January, 2023 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.