Jean Boivin, Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Natalie Gill – Portfolio Strategist and Carolina Martinez Arevalo – Portfolio Strategist all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

The stock story: U.S. stocks could run with hopes for inflation to fall to target and sharp rate cuts into 2024. We stay selective as we expect resurgent inflation to come into view.

Market backdrop: U.S. stocks climbed and the 10-year U.S. Treasury yield fell last week. The December U.S. CPI confirmed inflation is falling but set to rollercoaster back up.

Week ahead: We look to U.S. data this week for more signs policy rates are cooling business activity and consumer spending. We expect growth to slow further this year.

Equity markets – and even the Federal Reserve – have largely embraced the soft landing narrative that inflation will fall to the Fed’s 2% target without a recession. We agree that inflation will near 2% this year, likely supporting that narrative for now. The problem: Inflation won’t remain at that target, in our view, and this risk becoming clearer could challenge upbeat sentiment. So we monitor earnings season for any signs of cracks given pricey valuations.

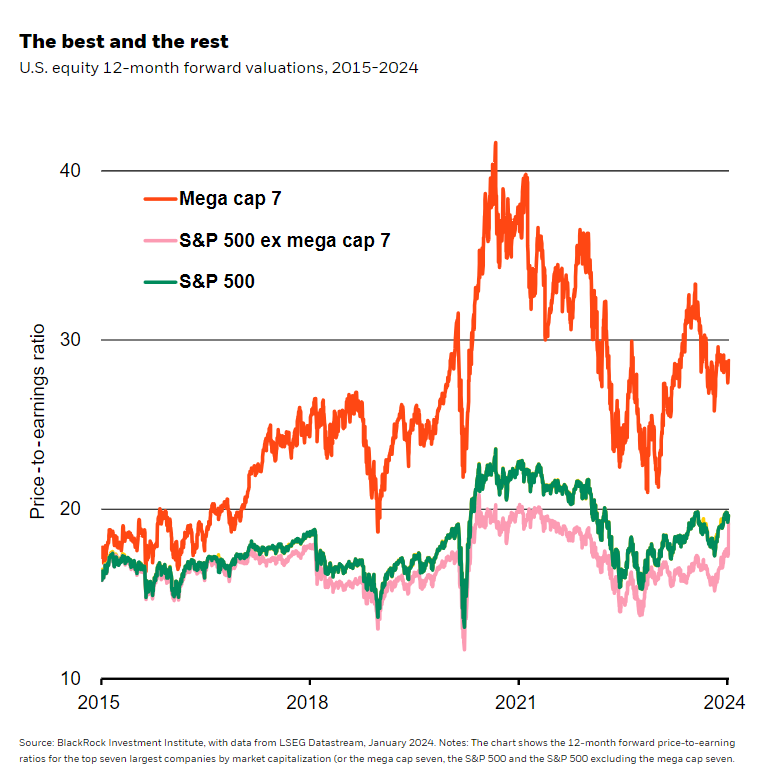

Even after the market-wide rally in December, market concentration in a handful of mega caps – firms with ultra-large market capitalizations – remains high. Favored by markets for their ability to leverage artificial intelligence (AI), these technology companies drove U.S. stock market gains last year. Price-to-earnings ratios divide a company’s share price by its earnings per share. Their expected price-to-earning valuations for the next 12 months (orange line in the chart) are about a third higher than for the S&P 500 and when excluding them (green and pink lines). Stronger earnings expectations have supported the mega cap rally, with valuations falling in the second half of 2023. Will pricey valuations halt the rally? We find valuations tend to matter more for long-term rather than near-term stock returns, and that’s why they usually aren’t enough to spoil market sentiment without a catalyst.

Earnings could be a catalyst. We expect greater focus on earnings this year after consensus expectations rose through last year, with up to 11% growth now expected in the next 12 months, LSEG data show. The 2023 Q4 earnings season should shed more light on how such expectations will evolve. Profit margins in the U.S. and euro area have held up as companies have passed on higher costs to consumers and cut costs. We think they will normalize over time due to pressure from higher interest rates, ongoing wage gains and lower if still above-target inflation.

All eyes on inflation

Inflation is another catalyst that could challenge the positive market sentiment, in our view. Stocks are currently priced for a near-perfect outcome: a soft economic landing, where inflation falls, central banks sharply cut rates and more cuts come if growth risks emerge. Appetite for investing in risk assets seems much stronger now as markets have confidence inflation is normalizing back to 2% and that rates cuts are on the way. Inflation falling closer to target will likely dominate market news in the near term and buoy stocks for some time. Yet market jitters in early January suggest there is some anxiety about macro risks further out. Our portfolio managers generally see 2024 as another year of flip-flopping market narratives – and volatility.

The December CPI confirmed our view that U.S. inflation is on track to fall back near 2% this year due to falling goods prices. Yet data also reinforced that inflation will likely jump back near 3% in 2025 due to structural forces such as ongoing wage pressures in a tight labor market and geopolitical fragmentation. The risk of resurgent inflation coming into view – which we think will happen later this year – is one development that could spoil upbeat market sentiment. In Europe, banks have driven fatter profit margins for the broader market. But the European Central Bank cutting rates this year could dent their income.

Our bottom line

We think stocks can run with the soft-landing narrative into 2024, until other possible outcomes – like an inflation rollercoaster – come into view. We stay selective in developed market stocks. We still favor Japan, tech, AI and quality overall as they have outperformed – and will likely be more resilient to any shift in market narrative. Bond yields have fallen on market pricing of sharp rate cuts. We expect ongoing yield volatility as we don’t see central banks delivering such cuts.

Market backdrop

U.S. stocks rose nearly 2% last week, now flat for the year, while the 10-year Treasury yield ticked down to 3.95%. We think long-term yields are likely to drift higher. That’s because the Fed will not be able cut rates as deep or as quickly as markets are pricing due to the resurgent inflation we expect – a risk the December CPI confirmed. We also see investors demanding more compensation for the risk of holding long-term bonds given interest rate volatility and massive Treasury bond issuance.

We look to U.S. data out this week for more signs that higher policy rates are cooling business activity and consumer spending. CPI data in the UK will likely follow other developed markets and show inflation falling as the mismatch between goods and services unwinds. Yet we see inflation rising again in early 2025 as an aging population keeps the labor market tight, driving wage pressures. That means central banks will likely keep interest rates high for longer.

Assets in review

Week Ahead

Jan. 17: U.S. retail sales; UK CPI; China Q4 GDP

Jan. 18: U.S. Philly Fed business index

Jan. 19: University of Michigan consumer sentiment survey

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 16th January, 2024 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.