Liontrust GF High Yield Bond Fund is manufactured by Liontrust Fund Partners LLP and represented in Malta by MeDirect Bank (Malta) plc.

Market review

In Q4, the global high yield market returned 5.2% (US dollar terms), its first positive quarter in 2022. The US high yield market produced a return of 4.0% and in Europe the market returned 5.6%. Both markets performed well, primarily on the back of expectations that we may be closer to the top of the interest rate cycle amid easing inflation concerns. Performance was also supported by relatively good corporate earnings and limited primary supply providing a strong technical rally.

The US and European high yield markets in Q4 both saw BB and B bonds significantly outperform CCCs, which is also reflective of the pattern we have seen for the full year, where better quality bonds outperformed lower quality bonds.

During 2022, investors contended with a climb in inflation, the Russia-Ukraine conflict, a rapid pace of monetary tightening, increasing global growth concerns, and significantly higher government bond yields. Not surprisingly, these tough conditions produced a challenging backdrop for returns.

Fund review

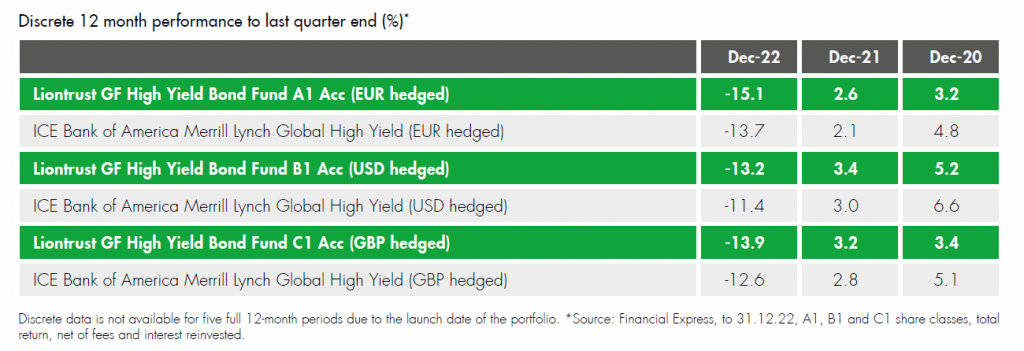

Over the quarter, the Liontrust GF High Yield Bond Fund (A1, accumulation class, total return in euros) produced a return of 5.1% versus the ICE BAML Global High Yield index’s (euro hedged) 4.3%*.

Relative to the index, the best performing sector in the Fund in Q4 was telecoms, followed closely by capital goods and healthcare. Our preference for higher quality and less cyclical sectors skew us towards slightly longer duration in our credit selection than our index, which has worked in our favour this quarter. Decent contributors to stock-picking include UK life insurance companies Rothesay and Phoenix as we saw sterling denominated names come back into favour after Kwasi Kwarteng’s ‘mini budget’ was reversed, pharmaceutical company Cheplapharm, packaging company Ardagh, and industrial equipment manufacturer Howden. Howden being taken over by Chart Industries; it was a CCC-rated 11% coupon bond that we sold above the call price to lock in a positive total return.

Our real estate exposure has been a slight drag to performance this quarter. As a reminder, we do not have exposure to Chinese real estate so our exposure to the sector is underweight versus the index. We have exposure to highly rated northern European real estate names, diversified by both geography and end use.

During Q4 the Fund participated in one new issue: House of HR. This company operates across Europe and provides HR solutions to a wide scope of industries. It is a credit we have previously held and has since come back to the market to fund its acquisition by Bain Capital. It has a strong business model, ability to pass through costs to customers and generates a healthy level of cashflow. The euro-denominated bond is rated B2 and came with an attractive coupon of 9% and at a discount to par offered a yield of around 10.5%.

We also purchased a few new holdings in the Fund. South African company Sappi produces a diverse range of products including coated woodfree paper, dissolving wood pulp and speciality packaging. The packaging part of the business provides a defensive and growing source of revenues, while the paper segment is in structural decline but currently benefitting from strong pricing power due to market supply dynamics. Management’s more recent announcements of asset sales, improved future guidance and tender for outstanding 2026 bonds in efforts to deleverage the business are all taken positively and provides us additional comfort around the credit. This is a euro-denominated, Ba2/BB- rated bond with 3.625% coupon trading in the mid-80s.

Another new holding is Sirius Media, a US satellite radio subscription business. The company generates a healthy level of cash, has high margins, and the subscription model means revenues are predictable and it has a strong level of liquidity. Overall, the company is in a good financial position to deal with potential headwinds. The bonds we own are US dollardenominated, 4% coupon, with a 6.75% yield and are rated Ba3/BB.

Finally, Fortescue Metals Group was also added to the Fund in Q4. The company is an Australian miner of iron ore, sending the vast majority of its mined product to China. It is listed and has a decent equity cushion, strong credit metrics and is investing heavily to meet net zero (scope 1&2) targets by 2030. We own the US dollar-denominated, 6.125% coupon, Ba1/BB+ rated green bonds.

Outlook

Over the past year, the global high yield market has suffered from a volatile macro backdrop brought on by several factors including geopolitical issues, the energy crisis and central banks trying to combat high inflation amongst others.

In 2022, the market environment has punished bonds both across sectors and the credit rating spectrum, but we believe this will turn in the coming year. We have been investing in bonds based on strong corporate fundamentals and value and have a bias towards high quality defensive credits. We have minimal exposure to cyclical credits. We think our Fund is well positioned to withstand the mild recessionary period we are expecting to enter into in 2023.

Corporate fundamentals are strong and likely to erode off a strong base, while default rates are still very low. There is no major refinancing wall to address for companies and we believe there is sufficient demand to meet any increase in primary bond issuance versus last year. Taking these points into consideration, we expect the coming year to have a different story, where fundamentals and idiosyncratic themes come back into focus was a key driver of performance and, therefore, we expect to see more dispersion in the market.

The global high yield market has never had two consecutive years of negative total returns. We expect 2023 to follow this trend and result in positive return. Our Fund is currently offering a yield of almost 10% for sterling investors (closer to 8% for euro investors), which we view as an attractive entry point. Our bias towards, defensive, better quality, liquid, listed names should put us in a good position as we progress through 2023. We have slowly increased our cash balance going into the new year by selling some bonds into the Q4 rally and so we have enough cash to put to work for any opportunities that arise during periods of market volatility.

Liontrust Key risks & Disclaimers:

Past performance is not a guide to future performance. Do remember that the value of an investment and the income generated from them can fall as well as rise and is not guaranteed, therefore, you may not get back the amount originally invested and potentially risk total loss of capital. The issue of units/shares in Liontrust Funds may be subject to an initial charge, which will have an impact on the realisable value of the investment, particularly in the short term. Investments should always be considered as long term.

Investment in the GF High Yield Bond Fund involves foreign currencies and may be subject to fluctuations in value due to movements in exchange rates. The value of fixed income securities will fall if the issuer is unable to repay its debt or has its credit rating reduced. Generally, the higher the perceived credit risk of the issuer, the higher the rate of interest. Bond markets may be subject to reduced liquidity. The Fund may invest in emerging markets/soft currencies and in financial derivative instruments, both of which may have the effect of increasing volatility.

Issued by Liontrust Fund Partners LLP (2 Savoy Court, London WC2R 0EZ), authorised and regulated in the UK by the Financial Conduct Authority (FRN 518165) to undertake regulated investment business.

This document should not be construed as advice for investment in any product or security mentioned, an offer to buy or sell units/shares of Funds mentioned, or a solicitation to purchase securities in any company or investment product. Examples of stocks are provided for general information only to demonstrate our investment philosophy. It contains information and analysis that is believed to be accurate at the time of publication, but is subject to change without notice. Whilst care has been taken in compiling the content of this document, no representation or warranty, express or implied, is made by Liontrust as to its accuracy or completeness, including for external sources (which may have been used) which have not been verified. It should not be copied, faxed, reproduced, divulged or distributed, in whole or in part, without the express written consent of Liontrust. Always research your own investments and (if you are not a professional or a financial adviser) consult suitability with a regulated financial adviser before investing.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from Liontrust Fund Partners LLP. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.