Wei Li, Global Chief Investment Strategist at the BlackRock Investment Institute together with Vivek Paul, Senior portfolio strategist, Nathalie Gill, portfolio strategist and Kurt Reiman, Senior Strategist for North America all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Passing on ‘buy the dip’: We’re not buying the stock dip because valuations haven’t really improved, there’s a risk of Fed overtightening, and margins challenge corporate earnings.

Market backdrop: Stocks fell and yields jumped last week on news of persistent U.S. inflation and rapid euro area rate hikes, showing markets are primed to be hawkish on rates.

Week ahead: The Fed is set to lift rates by 0.5% this week. The eventual sum total of rate hikes will be historically low, in our view, but the risk of overtightening is rising.

U.S. stocks have suffered the biggest year-to-date losses since at least the 1960s. That’s ignited calls to “buy the dip.” We pass, for now. Valuations aren’t much cheaper given rising interest rates and a weaker earnings outlook, in our view. A higher path of policy rates justifies lower equity prices. We also see a risk the Fed will lift rates too high – or that markets believe it will. Plus, margin pressures are a risk to earnings. That’s why we’re neutral on stocks on a six- to 12-month horizon.

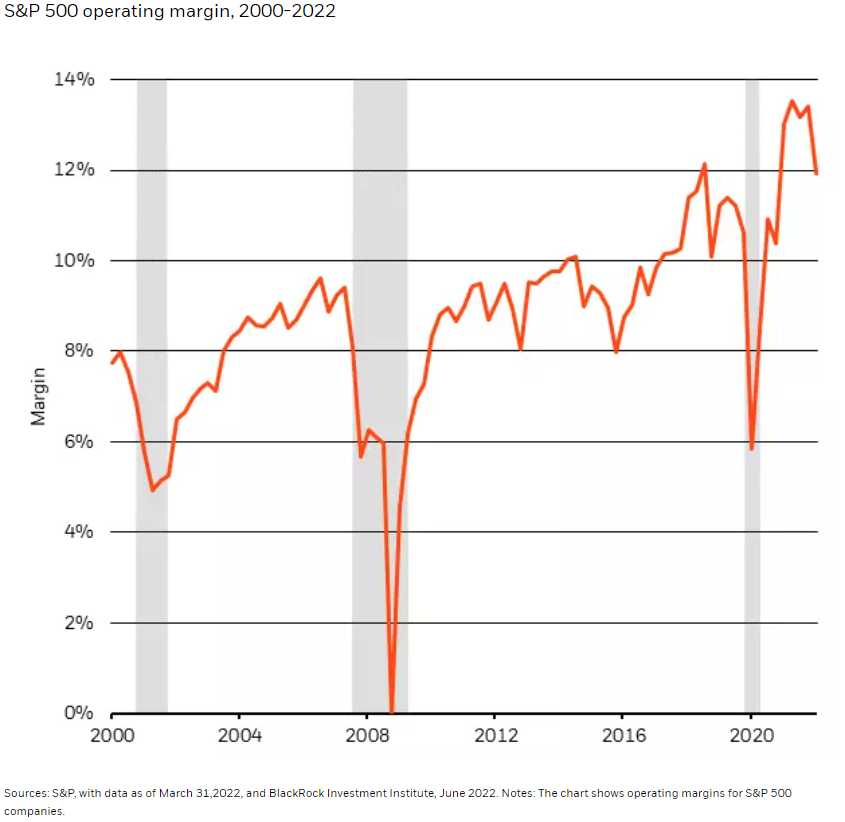

Margin pressure worries mount

So we don’t buy the dip. Why? Three reasons. First, profit margins have marched upward for two decades, as the chart shows. We now see increasing risks to the downside. We expect the energy crunch to hit growth and higher labor costs to eat into profits. The problem: Consensus earnings estimates don’t appear to reflect this. For example, analysts expect S&P 500 companies to increase profits by 10.5% this year, Refinitiv data show. That’s way too optimistic, in our view. Stocks could slide further if margin pressures increase. Falling costs like labor have fed the multi-decade profit expansion. So far, unit labor costs – the wages a company pays to produce a unit of output relative to its selling price – haven’t risen much. We see real, or inflation-adjusted, wage hikes to entice people back to work. That’s good for the economy – but bad for company margins.

Companies have managed to expand margins over the years through automation and other means, including in the pandemic. Now challenges are mounting. We see easing consumer demand as the restart of economic activity slows. This will reduce companies’ ability to pass on higher costs to consumers, in our view. We also expect a rotation of consumer spending back into services and away from goods as the world normalizes – and see this helping the economy more than equities. Services make up most of the economy, whereas S&P 500 earnings are evenly split between services and goods.

Risks to stocks

The second reason we’re not buying the dip: Equities haven’t cheapened that much, in our view. Why? Valuations haven’t really improved after accounting for a lower earnings outlook and a faster expected pace of rate rises. The prospect of even higher rates is increasing the expected discount rate. Higher discount rates make future cash flows less attractive.

Lastly, we’re not pounding the table on buying stocks right now because of a growing risk that the Fed tightens too much – or that markets believe it will, at least in the near term. Signs of persistent inflation, like last week’s CPI report, may fuel the latter risk. That’s all part of why we turned tactically neutral on equities last month. Stocks slumped last week near lows of the year. We don’t see a sustained rally until the Fed explicitly acknowledges the high costs to growth and jobs if it raises rates too high. That would be a signal to us to turn positive on equities again tactically.

We see central banks ultimately opting to live with inflation instead of raising policy rates to a level that destroys growth. That means inflation will likely stay higher than pre-Covid levels. We also think the Fed will quickly raise rates and then hold off to see the impact. The question is when this dovish pivot will take place. This uncertainty is why we’re tactically neutral on stocks but overweight on a strategic, or longer-term, horizon. We think the sum total of rate hikes will be historically low.

Bottom line

We are tactically neutral on stocks and are not buying the dip. First, valuations haven’t really improved when taking into account faster rate hikes than the market had priced. Second, there’s an increasing risk that the Fed overtightens or markets actually believe its tough talk on inflation. Third, a slowing restart and margin pressures spell trouble for heady earnings estimates in 2022 and 2023. We think central banks will eventually make a dovish pivot to save growth or avoid a deep recession. This is why we are overweight equities in the long run but neutral on a tactical horizon.

Market backdrop

U.S. CPI inflation data showed persistently high inflation last week, while the European Central Bank (ECB) announced plans to end asset purchases and carry out a rapid series of rate hikes. Stocks fell and yields rose, showing markets are primed to be hawkish on rates. We think the ECB and markets are underappreciating the risk that the energy crunch could bring the euro area to the brink of recession. We expect the ECB to accept this at some point and rethink its rate path.

The Fed will be front and center this week as it likely raises rates by 0.5%. Markets will focus on updated growth and inflation forecasts, indications of the future policy rate path and whether the Fed acknowledges that reducing inflation back to its 2% target would come at the cost of jobs and growth. We see the Fed hiking rates to a neutral level – one that neither stimulates nor drags on activity – by the end of the year, before pausing.

Week Ahead

June 14: Germany ZEW sentiment report; Japan machinery orders

June 15: U.S., Brazil monetary policy decisions

June 16: UK monetary policy decision; U.S. Philly Fed Business Index

June 17: U.S. industrial production; Bank of Japan rate decision

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of June 13th, 2022 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Investor Information Document (KIID), which may be obtained from MeDirect Bank (Malta) plc.