Emily Haisley, Behavioral Finance with BlackRock Risk & Quantitative Analysis, together with John Boivin, Head, Wei Li, Global Chief Investment Strategist and Beata Harasim, Senior investment strategist, all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Investing biases: We highlight the top three behavioral biases to avoid in the new, volatile market regime – and give tips on how investors can try to overcome them.

Market backdrop: Stocks rallied and yields fell last week after markets concluded the Fed’s pace of rate hikes will slow. We are less sanguine and see a dovish pivot only later.

Week ahead: We are watching this week’s U.S. jobs report for any signs production capacity is on the mend. The labor shortage is a key production constraint.

Investors are strapped in for a market rollercoaster in a new regime of increased volatility. Views on central bank rates are shuffling fast, as last week’s market reaction to the Fed’s rate hike showed. We think this warrants careful thought about portfolio changes. But change is hard. Behavioral biases subconsciously influence investment decisions. We look at three biases likely to trouble investors, especially in this volatile market – and share tips on how to overcome these pitfalls.

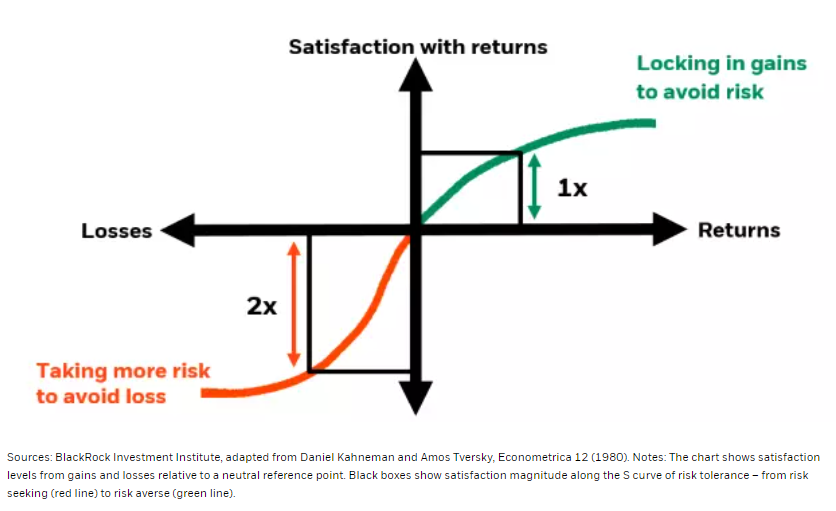

Pain vs. gain

Satisfaction with gains and losses in behavioral finance prospect theory.

The first bias is the disposition effect, or the tendency to hold losing positions too long and sell winning ones too soon. We expect the disposition bias to be most prevalent when investors are feeling stinging losses – like so far this year. Both stocks and bonds have racked up declines not seen since the 1970s this year. Behavioral finance finds that people feel the pain of loss twice as strongly as they experience an equivalent gain as pleasurable (the red versus green arrow in the chart). As a result, people may hold on to losing positions to avoid the pain of a loss (bottom left in chart). Meanwhile, it’s tempting to lock in gains too soon on winning positions because of a reluctance to take more risk for only marginal benefits (top right).

There’s a second bias that should really be public enemy No. 1 today for professional investors: inertia. This is a reluctance to make changes or making ones too small to affect performance. Why is this especially a problem now? The era of steady growth and inflation known as the Great Moderation is over, we believe. A new regime of increased macro volatility is in its place. Yet central banks appear to believe they can magically curb inflation and cause only a mild economic slowdown, as we wrote last week. We see more volatility ahead as markets have rallied on hopes the Fed is about to change course and relax policy. That optimism is misplaced, in our view. All of this calls for professional investors to change their portfolios more quickly. It will be costly, in our view, to just follow playbooks such as “buying the dip“ or make slow and minimal changes.

Endowment is the third kind of bias to guard against in the current market backdrop. Think of it as excessively deliberating over whether you may one day need something that sat collecting dust for years – whereas you clearly should be decluttering. People with this bias overvalue their assets. The longer they own them, the higher the price they demand to give them up. The endowment effect can lead investors to hold on to positions even after an investment strategy has played out. This can hurt performance. Positions often produce more returns earlier in their life spans, we find.

Tips to mitigate these biases

First, do a blank-slate exercise – imagine you have realized all your gains and losses. Then construct the ideal portfolio for the most likely market and macro environment over your time horizon. That doesn’t mean abandoning long-standing investment processes. Instead, consider portfolio changes without basing it on your historical portfolio holdings and performance. Second, think of future market events or performance thresholds that would signal when to take profit or cut losses. Making a plan can help determine how to react amid volatile markets and high emotions. This is the reason we give signposts for changing our views in our 2022 midyear outlook. Third, encourage open conversations about biases and the changes required to overcome them. Discuss your emotions after losses, examine mistakes even when performance is good, and weigh input from colleagues with an alternative point of view.

Our bottom line

Beware of behavioral biases in investing. We are guarding against their pitfalls because we believe the new regime requires an overhaul of portfolios. We’ve reduced portfolio risk throughout this year. Our latest tactical move: an up-in-quality portfolio shift by downgrading developed market stocks and upgrading investment grade credit. We underweight U.S. Treasuries and overweight inflation-linked bonds, believing markets underestimate the new regime’s inflationary nature

Market backdrop

The Federal Reserve increased the fed funds rate by another 0.75% last week. U.S. stocks rallied as markets concluded the Fed’s pace of rate hikes will slow, while yields fell on news of stalling growth. The Fed still thinks hiking rates will only cause a mild slowdown. It has yet to acknowledge the stark growth-inflation tradeoff: crush growth or live with some inflation. We don’t see a policy pivot until 2023, as data show persistent inflation. Expect more volatility until the Fed changes course.

This week’s U.S. jobs report is front and center. The report will be key as the Fed looks to the labor market for further signs of healing in production capacity. The Bank of England (BoE) is set to increase interest rates again. But we think it is nearing the point where it changes course. To us, the growth cost of further rises will lead the BoE to live with inflation above target.

Week Ahead

August 3: Caixin Services PMI

August 4: Bank of England policy meeting

August 6: U.S. jobs report

August 7: China trade data

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 1st August, 2022 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Investor Information Document (KIID), which may be obtained from MeDirect Bank (Malta) plc.