Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Catherine Kress – Head of Geopolitical Research & Strategy, all forming part of the BlackRock Investment Institute and Simon Wan – Portfolio Manager from BlackRock Multi-Asset Strategies and Solutions share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Defense spending rising – The geopolitical fragmentation mega force is evolving, with a big focus now on rising defense spending. We refine our preferences across regions and sectors.

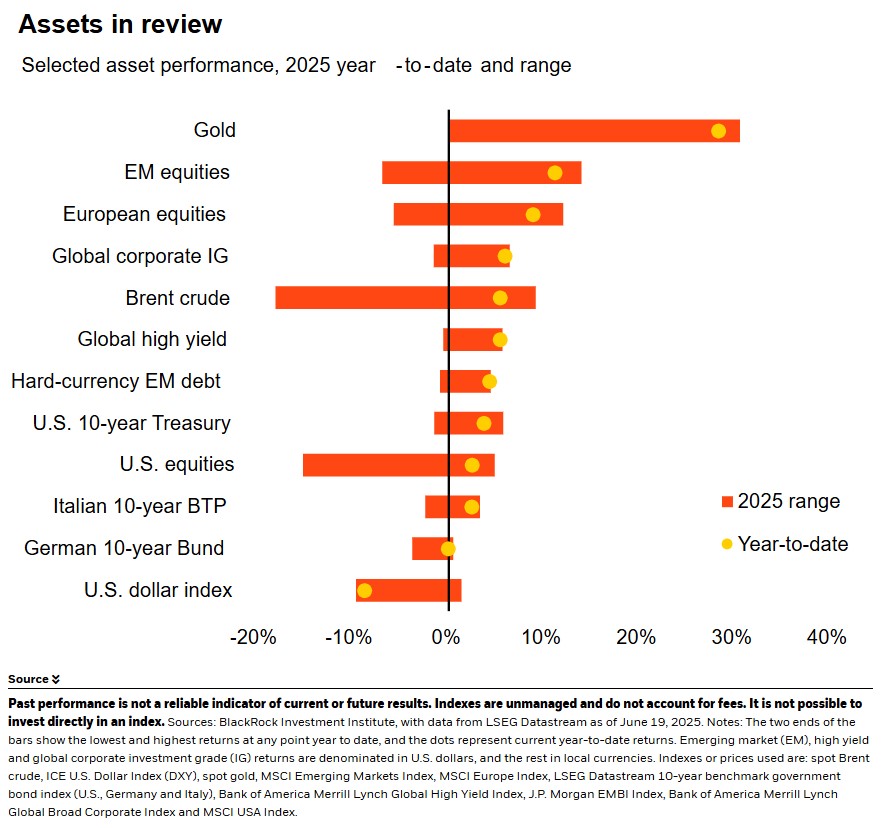

Market backdrop – Oil prices steadied after their surge on the Israel-Iran conflict. U.S. bond yields were little changed after the Fed signaled it was eyeing the impact of tariffs.

Week ahead – We watch the U.S. PCE data for signs of tariff impacts, so far limited in major data. Solid wage growth is keeping core inflation above the Fed’s 2% target.

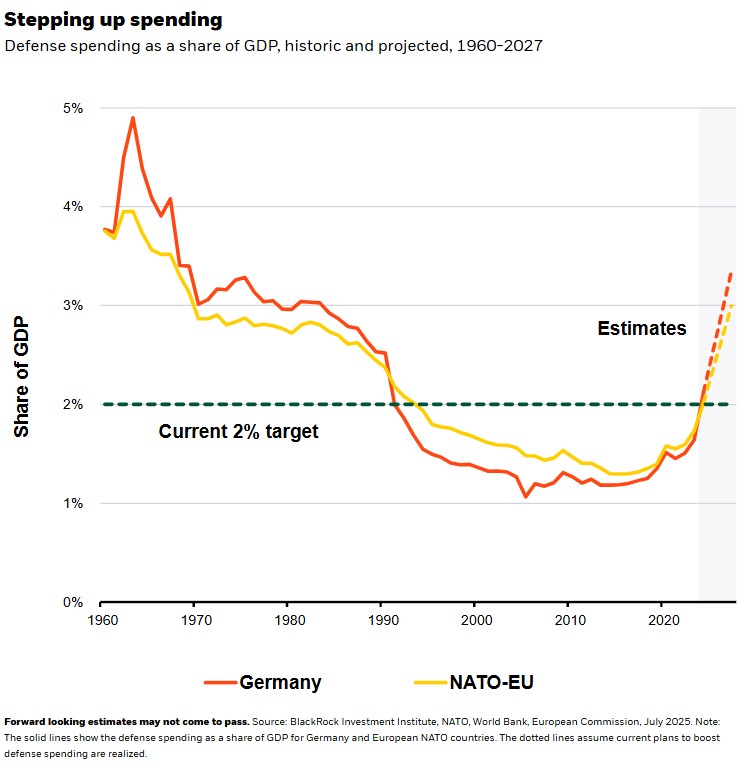

Geopolitical fragmentation has deepened in the past decade through shocks like the pandemic, Russia’s invasion of Ukraine, fresh conflict in the Middle East and rising trade tensions. A shifting U.S. security posture has accelerated this trend, pushing up defense spending in the EU and Asia – with this week’s NATO Summit set to lift Europe’s further. As the geopolitical mega force evolves, we take an active approach to the theme and get granular across regions and defense exposures.

Geopolitical fragmentation and economic competition – a mega force, or big structural shift we’ve long tracked – is rapidly evolving across multiple fronts. First: the emergence of geopolitical blocs, evidenced by different views on the Ukraine war and alignments with the U.S. and China. Second: competition between those blocs, most evident in the U.S.-China AI race. Third: the rewiring of supply chains to build resilience and support national security. Together, these dynamics are deepening geopolitical fragmentation and sparking investment in defense globally. After undershooting for decades, defense spending in Europe has now hit its target of 2% of GDP and is set to rise further. See the chart. Many NATO members are expected to agree to up spending to 5% of GDP after this week’s NATO Summit in The Hague, with an expected 3.5% for defense and 1.5% for defense infrastructure.

Another mega force overlaps with these dynamics: artificial intelligence. Tech supremacy has become a national security priority — particularly for the U.S. and China, where AI leadership is seen as critical to both economic advantage and military superiority. AI is expected to revolutionize how militaries around the world organize and operate. Take the use of drones in Ukraine and the Middle East, for example. We think investors can benefit from exposure to defense, meaning companies and industries directly or indirectly involved in products, services or capabilities supporting a country’s defense infrastructure. Such exposures can be a source of portfolio resilience, in our view, especially in periods of heightened geopolitical volatility.

Getting granular within defense

Yet we’re selective about which geographies and sectors we prefer to express the defense theme. Across regions, we eye opportunities in Europe as defense and infrastructure investment ramps up. Yet we stay selective for now given the over 60% surge in its aerospace and defense sector this year, according to LSEG data. Defense stocks in Japan and Korea look more attractive, in our view. We also favor the U.S.: it spends more than double on defense than Europe, SIPRI data shows. And it is home to the most advanced defense and defense tech firms. Many countries source key systems — especially air and missile defense — from U.S. suppliers. Among sectors, we see opportunities in defense tech. That includes not just AI and software companies, but also IT services and hardware like semiconductors that enable advanced technologies. We think many private companies in defense tech could launch initial public offerings (IPO) in coming years, allowing investors to tap this theme through public markets. We also like space tech, which we think could benefit as strategic competition intensifies.

In private markets, we see both near- and long-term opportunity, especially in infrastructure. Private markets are well suited for the capital-intensive, long-term nature of defense and infrastructure projects. Private markets can also fill in the gaps created by constraints on public funding that make it more difficult to get large infrastructure projects over the line without external funding. That is especially the case as worries about government debt and fiscal deficits mount.

Our bottom line

Growing geopolitical fragmentation and strategic competition in AI are reinforcing the global focus on national security and resilience – creating opportunities in defense. But as both mega forces evolve, they call for a selective approach.

Market backdrop

Oil prices added to gains to be up about 10% to near $75 a barrel since June 12 on concerns about potential energy supply disruptions as the conflict between Israel and Iran persisted. Stocks moved sideways, with the S&P 500 ticking down. U.S. 10-year Treasury yields were also mostly steady near 4.40%. The Federal Reserve kept policy rates unchanged, as expected. We still see a tight labor market and the eventual impact of tariffs limiting the Fed’s scope to cut rates.

We watch U.S. PCE data for signs of tariffs feeding through to consumer prices. Inflation data has been noisy since the pandemic, with big month-to-month swings making it difficult to draw conclusions. Wage growth has remained elevated, likely preventing inflation from settling at the Federal Reserve’s 2% target. We also watch early surveys for June activity to gauge how tariffs are impacting global manufacturing sentiment.

Week Ahead

June 23 : Global flash PMI

June 26 : U.S. durable goods

June 27 : U.S. PCE; Japan unemployment

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 23rd June, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.