Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Glenn Purves – Global Head of Macro, and Nicholas Fawcett – Senior Economist, all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Pro-risk on Fed cuts : A cooling labor market supports Fed rate cuts and is core to our risk-on stance. U.S. jobs updates are key – and now delayed due to the government shutdown.

Market backdrop : Tech and the AI theme powered equities globally, with U.S. stocks at new all-time highs. U.S. Treasury yields fell across the curve.

Week ahead : The government shutdown likely means a delay to release of U.S. trade and other data next week, so we keep an eye on private or state-reported data.

Our pro-risk stance hinges on signs that a cooling labor market spurs more Federal Reserve rate cuts. But the U.S. government shutdown delays one important sign – September payrolls data. This shifts focus to other data like job openings, private sector hiring and jobless claims – all so far consistent with a softer labor market. We are overweight U.S. equities and neutral long-term Treasuries, having closed a long-held underweight to bonds as the Fed resumed cuts.

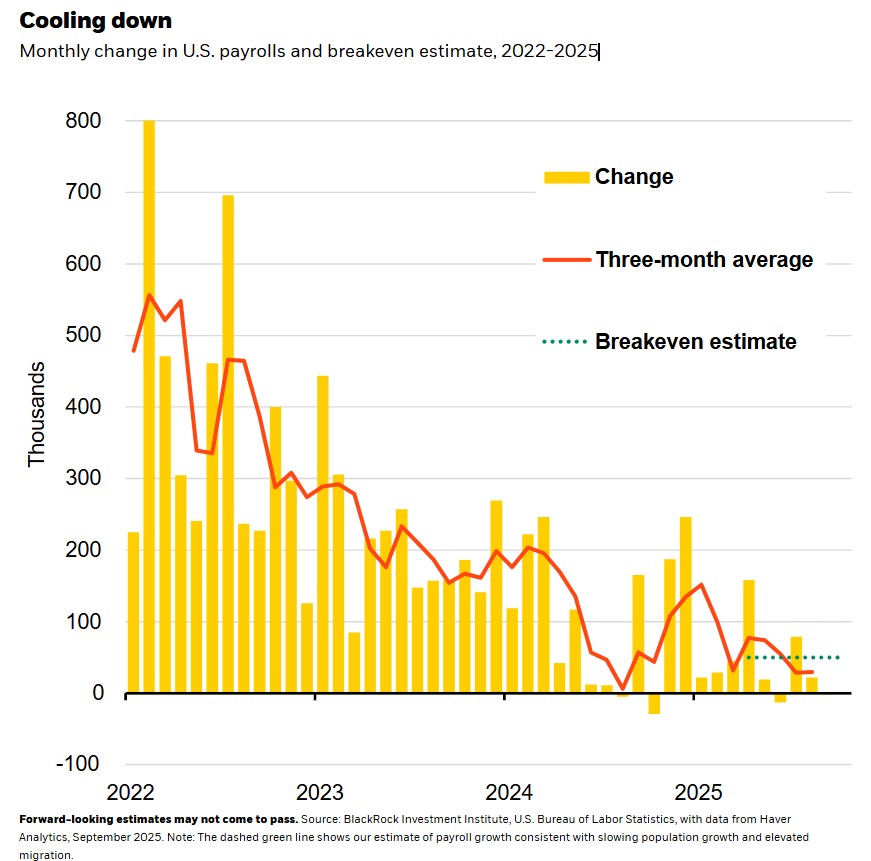

Motivated by worries about the softening labor market, the Fed cut rates last month – cuts that underpin our pro-risk stance, as we outlined in our Q4 Global Outlook. Job growth has run below 200,000 a month this year and unemployment has edged higher. The slowdown likely reflects tariff uncertainty, as companies wait for clarity, and federal job cuts, with about 100,000 jobs lost so far and more ahead. Labor supply has also weakened: the Congressional Budget Office now expects net immigration of 400,000 in 2025 versus a January estimate of 2 million. The result: labor demand has slowed sharply, but the “breakeven” pace of job growth – keeping unemployment and wage gains in check – has also fallen notably. See the chart. In other words: yes, job gains are slowing, but job losses are muted, with the unemployment rate low by historical standards – a “no-hiring, no firing” stasis.

For the Fed, this combination of weaker payroll gains and slowing inflation from softer labor demand has mitigated the tension between its inflation and employment mandates; justified the September rate cut; and allowed it to signal scope for more cuts. Questions about Fed independence and fiscal dominance are on the backburner for now. But the government shutdown that started on Oct. 1 deprives the Fed of important monthly payrolls data – just as that data become even more critical for its decisions. In its absence, policymakers and investors have latched onto other proxies – including the job openings (JOLTs) report released just before the shutdown, the private-sector ADP jobs report and state-reported weekly jobless claims – for a picture of the market. We think they’ll keep using these proxies until federal data releases return.

Several possible paths ahead

The shutdown and missing data hasn’t prevented markets from pricing for two further quarter-point cuts this year. We agree, provided the labor market keeps slowing. But beyond this year, we see several possible paths for activity and the labor market. In our base case scenario, resilient household incomes fuel a recovery in consumer spending. On top of this, large-scale investment stemming from the AI buildout – in tech equipment, software and data centers – drives growth. This scenario wouldn’t warrant the more than 100 basis points of rate cuts that markets have priced in by the end of 2026, in our view. That degree of policy easing would typically be associated with a more severe weakening in the labor market and drop in inflation. A sharp deterioration in U.S. growth looks less likely now, given the recent rebound in consumer demand.

A plausible alternative to our base case? A hiring rebound as peak tariff uncertainty passes and strong GDP growth puts the Fed back in a bind between inflation and employment, reviving questions about its independence – a possibility that shows why reliable labor market data is critical now. The September cut, expected quarter-point cuts later this year and ongoing AI capital investments support our long-held tactical overweight to U.S. equities and the AI theme. We also see an opportunity to lock in higher yields, particularly real yields, with U.S. 10-year real yields holding well above pre-pandemic levels.

Our bottom line

Our overweight to U.S. stocks depends on resilient activity and a cooling labor market spurring more Fed rate cuts. We stay neutral Treasuries, having closed a long-held underweight to long-term Treasuries as the Fed resumes cuts.

Market backdrop

U.S. stocks started Q4 by pushing to new all-time highs, with tech still leading. The AI theme remains key and global: A partnership between South Korean chipmakers and OpenAI helped spark Kospi gains of nearly 5%, taking its rise this year to nearly 50%. U.S. Treasury yields fell across the curve, with the 10-year yield near 4.10% and falling back near a five-month low. Gold prices hit new record highs to take their surge to nearly 50% this year.

The U.S. government shutdown will likely delay publication of U.S. trade data, an important gauge of how tariffs are impacting U.S. inflation. Import price data suggest that foreign suppliers haven’t been absorbing much of the tariff impact, leaving U.S. firms and consumers to bear most of the burden. Meanwhile, we eye the University of Michigan survey to see whether consumer sentiment – and by extension spending – is holding up.

Week Ahead

Oct. 7 : U.S. trade data (scheduled)

Oct. 10 : University of Michigan survey

Oct. 10-17 : China total social financing

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 6th October, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.