Liontrust GF High Yield Bond Fund is manufactured by Liontrust Fund Partners LLP and represented in Malta by MeDirect Bank (Malta) plc.

Market review

Emerging from a period of such extreme market support was always going to be turbulent for capital markets. The pace at which monetary policy tightens is also being dictated by the rise and stubbornness of inflation, with it now pretty clear central bankers were behind the curve with the transitory rhetoric of 2021. Add to all this, war in Europe, with geopolitics turning the last three decades on its head. Risk premia clearly had to re-price to this new world.

With this backdrop, despite negative returns, high yield has been fairly resilient. The worst of the drawdown during the quarter was half that of the S&P 500 and much less than more growth-oriented measures like the NASDAQ. Meanwhile, if you had chosen to invest in gilts, you would have lost 7.5% in the quarter.

The outperformance of low-quality bonds has continued in Q1 2022. On one hand, this doesn’t make a huge amount of sense given the spectre of stagflation; on the other, CCC rated bonds are skewed towards metals and energy, which will benefit from the enormous commodity price inflation we’re seeing as a result of Putin’s invasion of Ukraine. To be clear, the outperformance of low quality has been marginal in this quarter. We continue to dislike the asymmetric risks, maintaining our structural preference for high quality.

Fund review

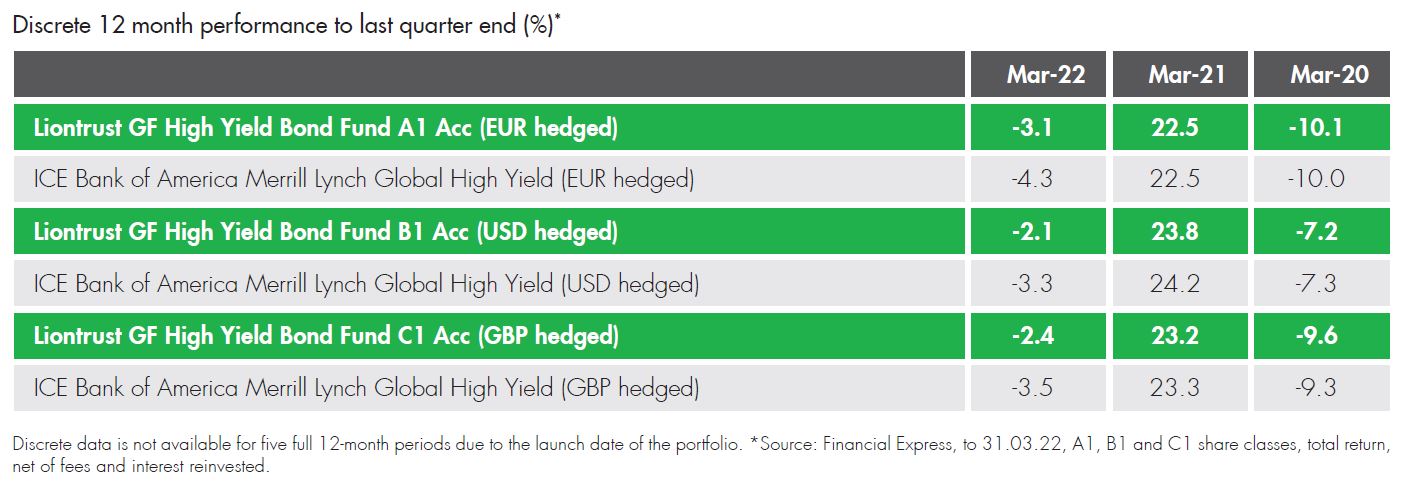

Over the quarter, the Liontrust GF High Yield Bond Fund (A1, accumulation class, total return in euros) produced a return of -4.6% versus the ICE BAML Global High Yield index’s (euro hedged) -5.8%*.

Around one-third of the outperformance versus index is from the real estate sector, where we have not owned distressed Chinese real estate bonds. We have kept close to developments in the sector, but we have generally found it too opaque to invest.

Another sector which proved useful to avoid was leisure. With a concentration in airlines and cruising lines, rising energy costs is becoming a thematic risk. With this in mind, we switched part of our holding in Ardagh Packaging into the metal can subsidiary from the part of the group more exposed to glass packaging. Glass packaging is more energy intensive, although we believe Ardagh Group has more than enough resilience and pricing power in order to adapt.

During a period of broad market sell-off, there were few individual bonds that added material outperformance on their own. However, stock-picking collectively added around one-third to the outperformance versus index. Obviously, there are exceptions as not every decision can always go our way: the Fund’s holding in Bausch Health bonds detracted from stock-picking, for example, costing the Fund around 10bps. Sentiment towards Bausch has been poor since it announced a more aggressive financial policy. We have reduced the Fund’s holding size, but believe the company has enough strength in its core business and strategic flexibility to survive intact in the medium to long term.

During the quarter, portfolio activity has been relatively modest, although we have taken opportunities to switch bonds which have sold off less into bonds which have sold off more. An example of this was reducing our holding in CCC-rated Howden at the same price it traded in December and buying subordinated bonds issued by BBB-rated Telefonica ten points below the December level.

Since the start of the 2021, we’ve managed the Fund with some hedges in place designed to protect returns in a rising interest rate environment. In Q1 2022, these hedges gained the Fund ~30bps.

Outlook

There is plenty in the world to worry about, but we don’t believe there is a material risk of a systemic rise in default rates. Of course, in a world of both higher interest rates and energy prices, profits and cash flow will be squeezed, but we believe there is enough quality and resilience in the high yield market to continue to make good risk-adjusted returns in this type of environment. This applies to BB-rated and B-rated bonds although, spoiler alert, we don’t think this is the case in CCC-rated bonds!

US high yield spreads are still below the long-term average, but with the number of interest rate hikes priced into US government bonds, the overall yield is in line with the long-term average. Given the likely resilience the US economy has to continued conflict in Europe, we think US high yield is decent value.

However, with European spreads above the long-term average, we also like valuations in Europe. The Fund is split fairly evenly between US and Europe (including the UK), which in an index context represents a large European overweight. The Fund has light exposure to cyclicals and companies with high energy costs of production. We have zero airlines, which are so exposed to fuel costs. The quality bias we have within our process means we are light in CCC-rated risk, which is only 5% of Fund. Moreover, our quality bias means we seek companies with pricing power and resilience, two operational qualities that are the best defence in more difficult economic periods.

Liontrust Key risks & Disclaimers:

Past performance is not a guide to future performance. Do remember that the value of an investment and the income generated from them can fall as well as rise and is not guaranteed, therefore, you may not get back the amount originally invested and potentially risk total loss of capital. The issue of units/shares in Liontrust Funds may be subject to an initial charge, which will have an impact on the realisable value of the investment, particularly in the short term. Investments should always be considered as long term.

Investment in the GF High Yield Bond Fund involves foreign currencies and may be subject to fluctuations in value due to movements in exchange rates. The value of fixed income securities will fall if the issuer is unable to repay its debt or has its credit rating reduced. Generally, the higher the perceived credit risk of the issuer, the higher the rate of interest. Bond markets may be subject to reduced liquidity. The Fund may invest in emerging markets/soft currencies and in financial derivative instruments, both of which may have the effect of increasing volatility.

Issued by Liontrust Fund Partners LLP (2 Savoy Court, London WC2R 0EZ), authorised and regulated in the UK by the Financial Conduct Authority (FRN 518165) to undertake regulated investment business.

This document should not be construed as advice for investment in any product or security mentioned, an offer to buy or sell units/shares of Funds mentioned, or a solicitation to purchase securities in any company or investment product. Examples of stocks are provided for general information only to demonstrate our investment philosophy. It contains information and analysis that is believed to be accurate at the time of publication, but is subject to change without notice. Whilst care has been taken in compiling the content of this document, no representation or warranty, express or implied, is made by Liontrust as to its accuracy or completeness, including for external sources (which may have been used) which have not been verified. It should not be copied, faxed, reproduced, divulged or distributed, in whole or in part, without the express written consent of Liontrust. Always research your own investments and (if you are not a professional or a financial adviser) consult suitability with a regulated financial adviser before investing.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from Liontrust Fund Partners LLP. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest should always be based upon the details contained in the Prospectus and Key Investor Information Document (KIID), which may be obtained from MeDirect Bank (Malta) plc.