Alex Brazier, Deputy Head of the BlackRock Investment Institute together with Wei Li, Global Chief Investment Strategist, Vivek Paul, Deputy Head of Portfolio Research and Kurt Reiman, Senior Strategist for North America, all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points:

What’s behind the prices: Commodities prices have spiked as demand from the restart clashed with tightening supply. We see the war and net-zero transition keeping prices high.

Market backdrop: U.S. and euro area inflation data last week showed still persistent inflation. Stocks and bond yields fell as markets priced more risk of rates hitting growth.

Week ahead: Labor participation and wage growth are key to watch in this week’s jobs data, we think, as the Fed weighs the magnitude of its next rate rise later this month.

We see an era of structurally higher commodities prices ahead. Why? First, look back. Prices ran up because the economic restart drove demand amid abnormally low supply. The West has tried to wean itself off Russian energy after years of declining investment. Now, look forward. We see structurally higher prices amid tight supply for energy and rising demand for metals that will be critical to power the path to reach net-zero carbon emissions by 2050.

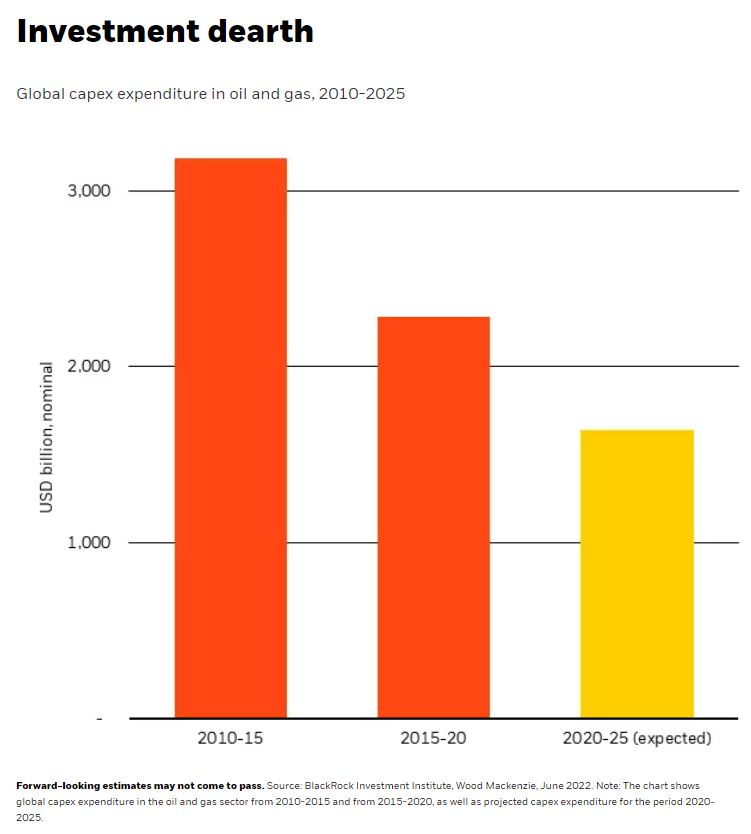

Commodities prices and renewables have surged over the past two years, even with recent declines. Rate hikes choking off the restart could cause more dips. But we think prices are at structurally higher levels now. Why? The West is trying to wean itself off Russian supplies. The flow of Russian gas into Europe has fallen by two-thirds already in just a few months. This is a structural change, and we see it as part of accelerating geopolitical fragmentation. The supply crunch is rooted in years of declining investment from traditional energy companies (see the red bars in chart) and forecasters expect even less in years to come (the yellow bar). This hasn’t been balanced by equally strong investment in clean energy supply. Lower capital expenditures are a result of both investors pushing for more capital discipline and concerns about long-term demand for traditional energy.

Energy commodities prices are likely to be supported by growing energy demands amid tight supply in coming decades. Even with improving energy efficiency in developed markets, global energy demand could rise significantly, especially if energy consumption in emerging markets jumps markedly as living standards improve.

And even with rapid growth of clean energy infrastructure, it would be nearly impossible to meet energy demand in coming years without fossil fuels, as we say in a recent net-zero report. Some investment will likely still be needed in new fossil fuel production capacity to meet energy demand. Without capex, production generally falls as wells deplete. Current investment is below what is needed to meet demand in the short run, in our view, as capex has dropped by nearly half since 2014.

Transition to boost demand

The buildout of clean energy infrastructure will boost demand for other commodities, too. Transition essentials like wind turbine farms and electric vehicles require staggering amounts of iron ore, copper, lithium and other metals to match fossil-fuel-generated power sources’ outputs. Mineral demand for clean energy technology would have to rise by at least four times by 2040 to meet climate goals, according to the International Energy Agency.

The transition path remains uncertain. Last week’s Supreme Court decision means the Environmental Protection Agency now has more limited regulatory authority in requiring utilities to reduce reliance on higher carbon sources of energy, unless Congress approves legislation. This reinforces our view that the invasion of Ukraine has created a more divergent transition globally as Europe doubles down on net-zero efforts. The same impetus isn’t felt elsewhere.

What this means for investments

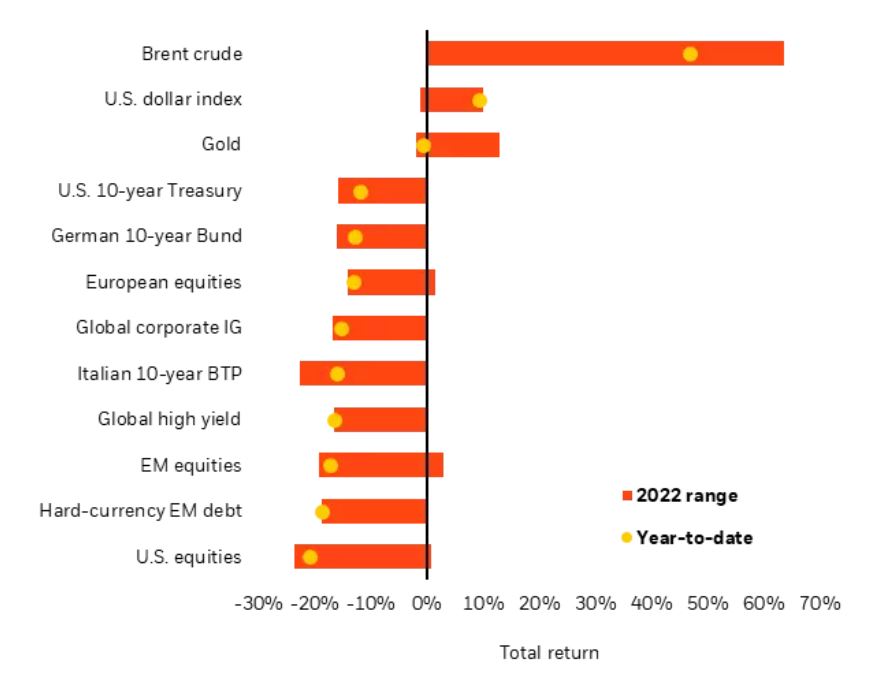

Time horizon is key. In the near term, we expect sharp rate rises from the Federal Reserve to choke off the restart of economic activity. That typically implies bad news for commodities or commodities producers – but not if we are in a new era of higher commodities prices. We see tactical opportunities in selected energy stocks after the recent selloff. They now appear priced for some retrenchment of energy prices, and we could see rising revenues and earnings amid the race to replace Russian supply.

On a longer-term, strategic horizon, we believe lower-carbon sectors like tech and healthcare will benefit more than traditional energy stocks. At the same time, we think some of the greatest opportunities may be in carbon-intensive companies with credible decarbonization plans or companies supporting the transition with the supply of critical minerals.

Market backdrop

Stocks slid after U.S. and euro area data last week showed persistent inflation and signs of slowing economic activity. U.S. two-year Treasury yields posted their largest weekly drop since 2020. Short-term rate markets are signaling doubts central banks, including the Fed, will hike rates as high as their projections. Central bankers’ talk on fighting inflation also gave little indication they face a policy trade-off: either crush growth or live with inflation. So we don’t see this as a time to buy the dip.

The key focus in next week’s U.S. jobs report will be signs the labor market is gradually healing – especially a recovery in labor participation. Labor shortages have added to U.S. inflation’s march up to 40-year highs. We think wage growth may help the labor market normalize by enticing people back to the workforce and incentivizing them to stop hopping jobs for higher pay.

Week Ahead

- July 5: China services PMI; U.S. factory orders

- July 8: U.S. jobs report

- July 9: China inflation data

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of April 25th, 2022 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Investor Information Document (KIID), which may be obtained from MeDirect Bank (Malta) plc.