John Boivin, Head of BlackRock Investment Institute, together with Wei Li, Global Chief Investment Strategist, Scott Thiel, Chief Fixed Income Strategist, and Nicholas Fawcett, Macro Research all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points:

More volatility ahead – Market views of Fed rate hikes have swung sharply. We see more volatility ahead as long as central banks think they can curb inflation without crushing growth.

Market backdrop – Yields spiked before easing after the ECB raised rates by 0.5% last week. We expect it to pause hikes before the Fed as the energy crisis hits growth hard.

Week ahead – Markets are pricing another 0.75% rate rise by the Fed this week. We think the Fed will overtighten rates and cause acute damage to growth before pivoting.

The Fed is set to raise rates by an additional 0.75% or more this week as it scrambles to raise the fed funds rate into restrictive territory to rein in inflation. Market views on what to expect next for rates have been volatile. Why? Central banks think they can curb inflation and cause only a mild slowdown, whereas this is unlikely in reality, in our view. We see more volatility ahead until central banks take sides in the stark trade-off between growth and inflation they are facing.

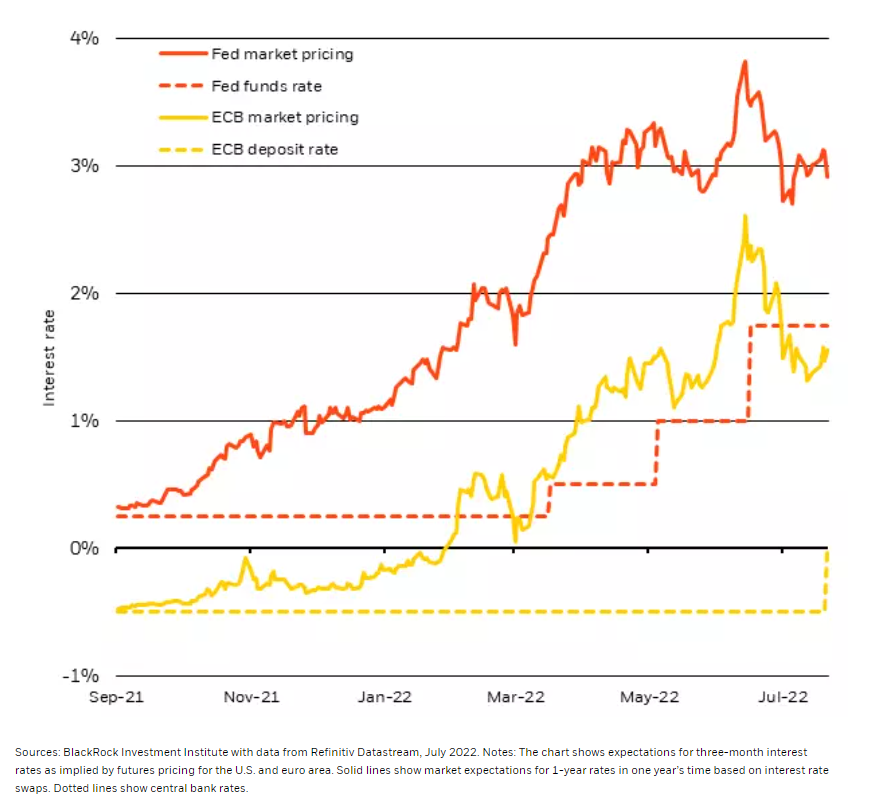

Bumpy ride

Central bank policy rate pricing in rate forwards, September 2021-July 2022.

Market expectations for Fed and European Central Bank (ECB) policy rates have swung up and down in the past year, futures pricing of Refinitiv data show. First, market pricing for the fed funds rate jumped from near zero to almost 4% in June. See the red line in the chart. That epic move was followed by a one percentage point drop in just a month’s time. The biggest monthly changes in rate projections have been more than double the average in the two decades before the pandemic, we find. The reason: Central banks have been ignoring the sharp trade-off they are facing: crush growth or live with some inflation. This has caused rate projections to surge higher on expectations central banks will fight inflation at all cost and then retreat on recession fears. The Fed’s forecasts in particular suggest it believes it can bring inflation back to its 2% target without damaging growth.

The Fed and ECB are hostage to the “politics of inflation,” in our view, responding to a chorus of voices demanding they bring down inflation. The problem? Today’s inflation is caused by production constraints, from labor shortages to supply chain kinks, not because of excessively high demand. Rate hikes can cool the latter but don’t really fix the former, we think. Reducing inflation to 2% would mean slamming spending down so hard it would stall the economic restart. Yet the Fed and ECB still suggest they can engineer a “soft landing,” where higher rates decrease inflation and cause only a mild slowdown. Case in point: The ECB explicitly said it doesn’t foresee a recession when it raised rates by 0.5% last week.

Can they stick a soft landing?

We think a soft landing is unlikely. Central banks today face sharp trade-offs between growth and inflation, as detailed in our midyear outlook, and many have yet to acknowledge this. The ECB limited its maneuvering room by stressing it’s only focused on inflation. This will make it harder to change course. We see a pivot later this year when a recession we flagged in early March comes knocking. We expect the Fed to change course only next year, when the economic effects of rate rises become clear. The market agrees. Rate projections now show the Fed cutting rates in 2023. That’s consistent with our view.

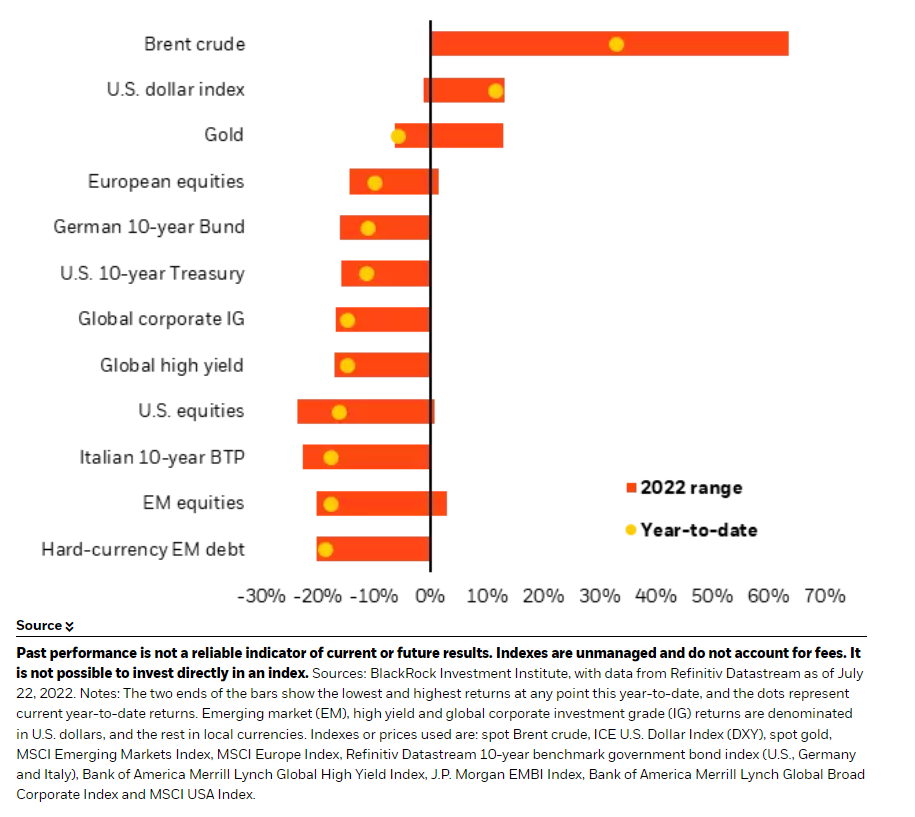

The ECB and Fed will eventually choose growth over inflation, we believe. That means they won’t have slammed demand all the way down to meet the low level of productive capacity. Production constraints are likely to keep fueling inflation as a result. That’s why we think inflation will persistently run above central bank targets, even as it declines from current 40-year highs. Market expectations are not consistent with this. Breakeven inflation rates, a measure of expected inflation derived from bond yields, have fallen sharply in the past month. Markets appear to expect a typical slowdown, where both growth and inflation weaken. This means inflation data could surprise to the upside – and cause markets to rapidly price a higher rate path once again. Result: another equities sell-off. That’s why we further reduced equities to a tactical underweight.

Our bottom line

We expect more volatility, so we focus on nimble, tactical positioning. We are underweight developed market equities on a tactical horizon because central banks appear set to overtighten policy. We are ready to switch back to overweight once central banks pivot to a more moderate rate path. We’re overweight credit amid higher yields and low default risks. We steer away from U.S. Treasuries as we expect further rate rises and a higher term premium, or the compensation investors demand for holding long-term bonds. We like inflation-linked bonds amid persistent inflation.

Market backdrop

The ECB raised rates by 0.5% last week. European bond yields spiked briefly on the news before settling lower on recession fears. We see a euro area recession even if rates rise very little. Why? We think the energy shock from Russia’s invasion of Ukraine will drag down economic activity. We’re already seeing weakness in PMI data, especially in Europe. The ECB’s new bond buying instrument to limit market stress may make it more inclined to overtighten policy into a recession, in our view.

This week’s Fed meeting is front and center. The market is pricing a hike of at least 0.75%. We think the Fed has boxed itself in by responding to political pressures to tame inflation. We see the Fed ultimately living with higher inflation, but only once the cost to growth from rising rates becomes clear. Second quarter U.S. and euro area GDP data will help gauge momentum.

Week ahead

July 26: U.S. consumer confidence

July 27: U.S. Fed interest rate decision

July 28: U.S. GDP

July 29: Euro area inflation, GDP; U.S. PCE, consumer spending

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 25th July, 2022 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Investor Information Document (KIID), which may be obtained from MeDirect Bank (Malta) plc.