Wei Li – Global Chief Investment Strategist of BlackRock Investment Institute, together with Vivek Paul – Head of Portfolio Research, Alex Symes – US Head of Research and Strategy, and Christian Olinger – Portfolio Strategist all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

A granular view: Financial cracks from rate hikes have led to jitters over commercial real estate. Yet granularity is key. We see opportunities in some U.S. industrial properties.

Market backdrop: The Federal Reserve signaled a pause may follow last week’s rate hike. Yet jobs data showed a tight labor market. We expect a pause but no rate cuts this year.

Week ahead: We expect U.S. inflation data out this week to show services are keeping inflation sticky, while survey data should gauge how U.S. consumers are holding up.

The fastest rate hiking cycle since the 1980s is causing financial cracks. This has caused bank turmoil and raised concerns over U.S. commercial real estate due to its high vacancy rates and reliance on bank loans. Yet we see varied risks across sectors, regions and investment choice. So we use our new playbook and get granular. We favor selected sectors such as industrial real estate as we see long-term forces like e-commerce and geopolitical fragmentation fueling demand.

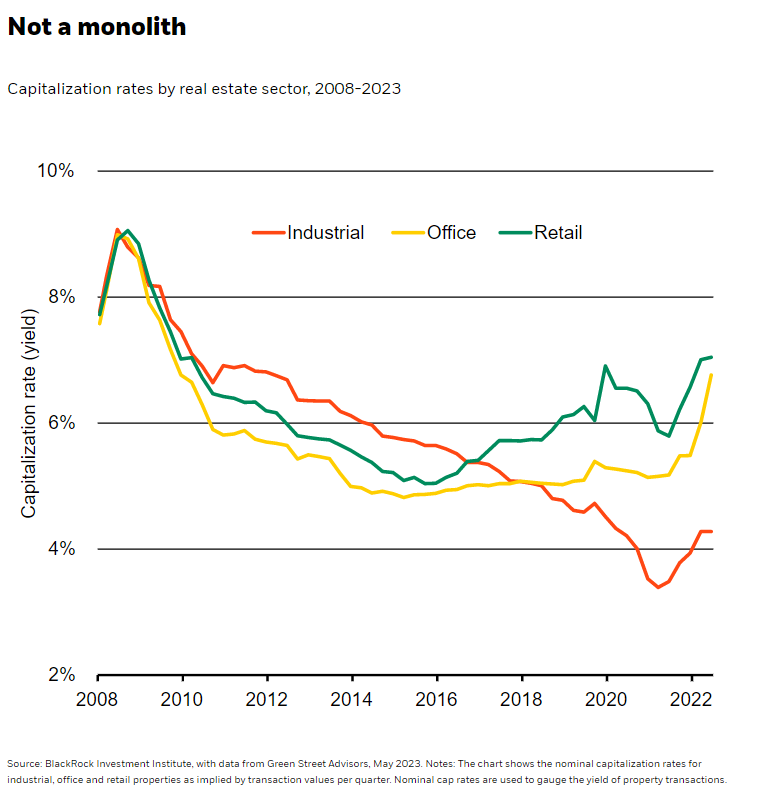

We went underweight private growth assets from a view of five years and over in 2023’s first quarter. That includes broad commercial real estate – a sector we’ve projected negative returns for since June 2022. Yet we know commercial real estate is not a monolith. Case in point: Capitalization rates – a yield metric that rises when valuations fall – have diverged. We expect retail cap rates to keep rising (green line in chart) due to pressure from e-commerce growth. Office cap rates (yellow line) are likely to rise too as they have since 2022. Investors are requiring higher cap rates for offices given rising interest rates and higher vacancy rates due to remote work. We expect industrial cap rates (dark orange line) to stay low relative to peers as we see higher earnings growth for the sector. Private assets can play a sizeable role in long-term portfolios, with potential to diversify returns, in our view. Private markets overall are complex, with high risk and volatility, and aren’t suitable for all investors.

Varied impact

The impact of the pandemic and bank turmoil on commercial real estate sectors has varied, too. Shifting work habits have cut demand for U.S. offices, based on a high vacancy rate of about 13% in March, National Council of Real Estate Investment Fiduciaries (NCREIF) data show. Banks’ exposure to real estate added to market jitters. Banks held 40% of outstanding real estate debt as of 2022’s third quarter, the Mortgage Bankers Association found. That has raised fears high-vacancy or highly-levered U.S. properties will struggle to refinance debt, causing some to hit the market at cheaper valuations or default. That dynamic may create a funding gap but also chances to scoop up discounted assets – with risks. We see the gap as a bigger concern for U.S. assets: Private European valuations are cheaper than U.S. peers, MSCI and NCREIF indexes show.

We’re cautious on private commercial real estate valuations: We think they need to fall more as rate hikes raise financing costs and cool inflation. That combo will likely bite into commercial real estate income growth. Exchange-listed real estate valuations are largely lower across the U.S., UK and Europe as real estate investment trusts (REITs) sold off with stocks in 2022, indexes show. Public REIT values tend to lead private markets by a few quarters. Yet REITs’ near-term correlation with stocks means they diversify portfolios less and may see more volatility when stocks fully price in economic damage.

Getting granular

Industrial assets – referring to warehouses used for distribution, manufacturing and research and development – have fared better than office. Industrial assets have a vacancy rate around 2% as of March and their share of the commercial real estate market has doubled since 2016 to take up roughly a third of the market now, according to NCREIF data. This differentiation is why we get granular. We like industrial assets that could see structural trends feeding demand in the long term, like distribution and last-mile logistics centers. The expansion of e-commerce looks set to keep on driving demand as it has for decades, in our view. We also think geopolitical fragmentation will likely shift supply chains and prompt companies to re-shore operations – bringing manufacturing closer to home. Companies have already been storing more goods locally to prevent renewed supply chain snarls, U.S. Census Bureau data show. Some may aim to widen their web of warehouses to cut transportation costs and to support new manufacturing plants. Construction spending on the latter rose to about $147 billion annualized this March vs. $90 billion in March 2022, U.S. Census data show.

Bottom line

Financial cracks have fed concerns over commercial real estate’s outlook. We’re cautious on the sector. Yet we go granular in our portfolio views. We see better value in real estate sectors that may see long-term demand, like industrial.

Market backdrop

The Fed signaled a pause may follow last week’s rate hike. The U.S. two-year Treasury yield sank 0.5% percentage points near 2023 lows before reversing about half the fall by Friday when April U.S. payrolls beat market expectations. The data also confirmed a tight labor market and wage pressure keeping inflation sticky. That makes rate cuts unlikely this year, in our view. We think that’s true for the European Central Bank, too: It pointed to more hikes after raising rates again last week.

All eyes are on U.S. inflation data this week. We expect services to keep inflation sticky even as interest rates stay higher. We’re also watching survey data to see how the consumer is holding up. We expect pandemic savings to dwindle and further crimp spending. We see the Bank of England hiking again this week as inflation remains stubbornly high.

Week Ahead

May 9: China trade data

May 10: U.S. CPI inflation

May 11: Bank of England policy decision; China CPI and PPI

May 12: UK GDP; University of Michigan survey

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 8th May, 2023 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.