Wei Li – Global Chief Investment Strategist together with Chris Weber – Head of Climate Research, Jessica Thye – Sustainable Research and Analytics all forming part of the BlackRock Investment Institute and David Giordano – Global Head of BlackRock Climate Infrastructure, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Three themes: We monitor battery prices, elections and market attention on climate resilience for their impact on transition-related investment opportunities and risks.

Market backdrop: U.S. stocks were mostly flat last week, while 10-year U.S. Treasury yields fell further. Markets still expect the first Federal Reserve rate cut around mid-2024.

Week ahead: We’re watching February U.S. CPI data out this week to see how much further inflation will fall in the near term. We still expect inflation to resurge in 2025.

The low-carbon transition is a mega force we track that is shaping investment returns now. We see potentially market-moving developments in three key areas this year. First, falling battery prices could boost demand for energy storage systems for power grids, and electric and hybrid vehicles. Second, elections around the globe could affect future energy and industrial policy. And third, rising physical damages could spur interest in a new investment theme: climate resilience.

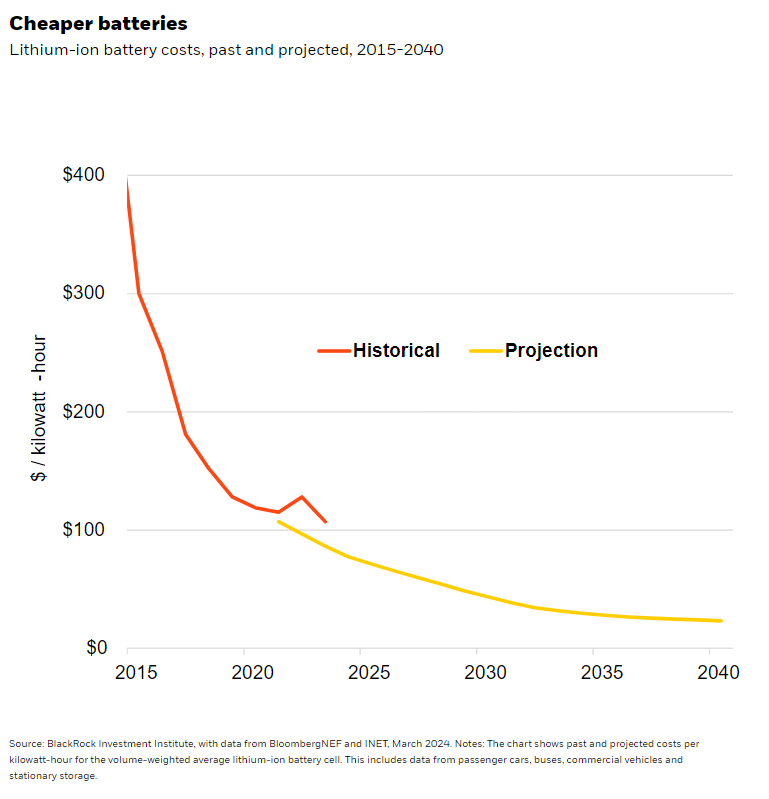

Battery prices make up a third or more of the production cost of some clean technologies, such as energy storage systems for power grids, electric and hybrid vehicles (EVs). They have slid sharply over the past decade. See the chart. The 2022 uptick looks to have been a blip, with battery producers signaling potentially sharp price cuts this year – largely due to an 80% price drop in lithium, a key input, after a surge in supply. Intense competition and rapid technological progress are helping reduce prices, too. Some companies are using artificial intelligence – another mega force – to discover new battery materials that could lower future costs. We’re watching whether a further fall in battery prices will feed through to final purchase prices and boost demand for energy storage, EVs and hybrid autos – especially as their running costs are lower than for traditional internal combustion vehicles.

Elections in focus

This year’s many elections, including in the European Union, U.S. and India, come at a time of increasing geopolitical fragmentation and as governments seek to balance decarbonization, energy security and energy affordability objectives – which can be complementary or competing. The election results could have implications for how that balance is struck – and consequently for the evolution and adoption of clean technology, and the path of the low-carbon transition more broadly.

Several governments are subsidizing their energy and clean tech industries, with non-subsidized competitors facing pricing and margin pressure. Countries could levy trade restrictions on imported tech to shield local industries. U.S. and EU investigations into the Chinese EV industry could have this outcome. We could also see changes to transition-related policy after the elections – potentially accelerating the transition in some places and slowing it in others. In India, the election could result in policy continuity, paving the way for quicker decarbonization and bolstering the country’s efforts to become a bigger clean technology production hub. The U.S. election result could have implications for the Inflation Reduction Act – a 2022 law that has spurred major investment in, and demand for, energy infrastructure and technology. Changes could range from repeal or delays to complementary policy that increases its effectiveness, like land permitting reform.

An emergent investment theme

A third focus: whether 2023’s title as the hottest year on record – as recorded by the World Meteorological Organization – and further extreme weather events this year will spark greater investor interest in climate resilience, or society’s ability to prepare for and withstand climate risks. Think early monitoring systems for floods, air conditioning to cope with heatwaves or retrofitting buildings to better withstand extreme weather. We think markets may underappreciate the prospects for firms creating and adopting resilience-boosting products and services – and see this becoming a more recognized opportunity.

Our bottom line

We think falling battery prices could boost the EV and energy storage industries this year. Much depends on the direction of global transition policy after key elections as we weigh transition-related investment opportunities and risks. As physical climate risks mount, we believe climate resilience could come to the fore as an investment theme.

Market backdrop

The S&P 500 was mostly flat on the week after pushing to new highs. U.S. 10-year Treasury yields edged lower and were about 20 basis points off their 2024 high after remarks by Fed Chair Jerome Powell did little to change expectations for a first rate cut around midyear. U.S. jobs data showed a strong if moderating labor market. Wage growth also moderated but remains at levels not consistent with inflation staying at the Fed’s 2% target. We still see inflation on a rollercoaster.

We’re watching the release of the U.S. CPI data for February this week to gauge how much further inflation will fall in the near term after January showed stubborn inflation. Rapidly falling goods prices look set to drive inflation down near the Fed’s 2% policy target this year. Yet once goods prices stabilize, we see inflation on a rollercoaster ride back up in 2025 as wage growth remains elevated and keeps services inflation higher than before the pandemic.

Week Ahead

March 12: U.S. CPI; UK jobs data

March 13: UK GDP

March 15: University of Michigan consumer sentiment survey

March 11-18: China total social financing

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 11th March, 2024 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.