Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist and Vivek Paul – Global Head of Portfolio Research all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Leaning against narrative shifts: 2024 reinforced this is an economic transformation, not a business cycle. We lean against market moves driven by other interpretations and expect volatility.

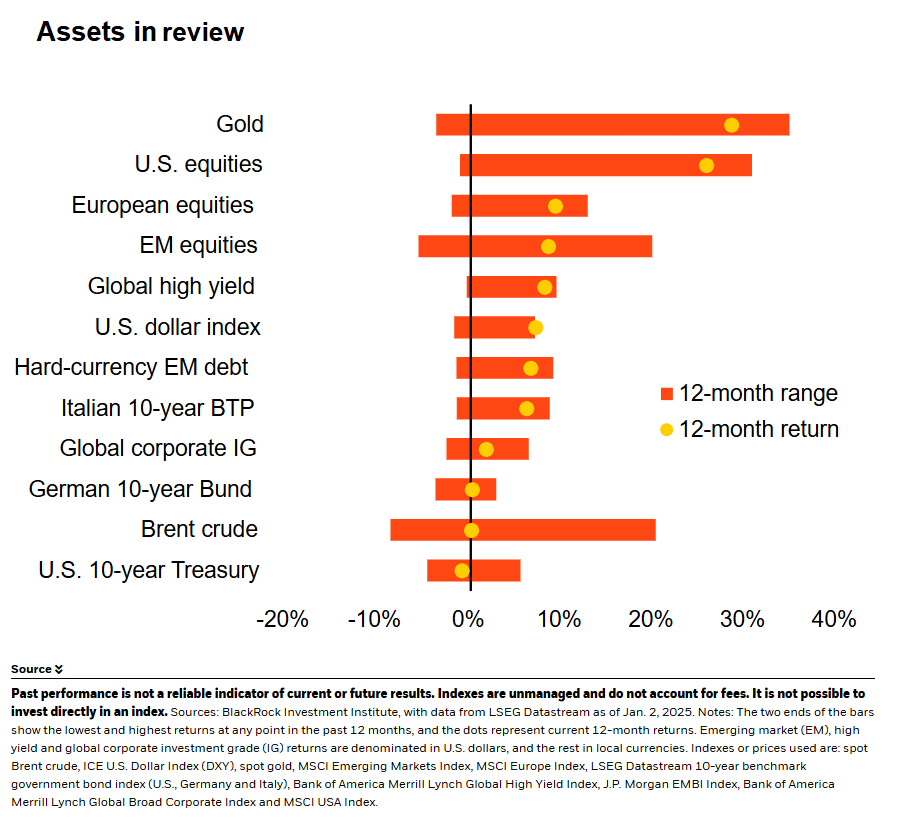

Market backdrop: U.S. stocks surged more than 20% in 2024, driven by major tech stocks. U.S. Treasury yields ended the year above 4.50% as markets priced out Fed rate cuts.

Week ahead: We get U.S. payrolls for December this week. Market expectations of only two Federal Reserve cuts in 2025 seem reasonable given sticky inflation, we think.

Three interconnected lessons from 2024 help shape our 2025 outlook. First, this is an economic transformation, not a business cycle. We hold to that core framing. Second, as markets instead keep trying to interpret macro data as though this were a typical business cycle, that creates opportunities to lean against the resulting market moves. Third: expect the unexpected as transformation and policy changes can also create surprises, volatility – and opportunities – in these choppy waters.

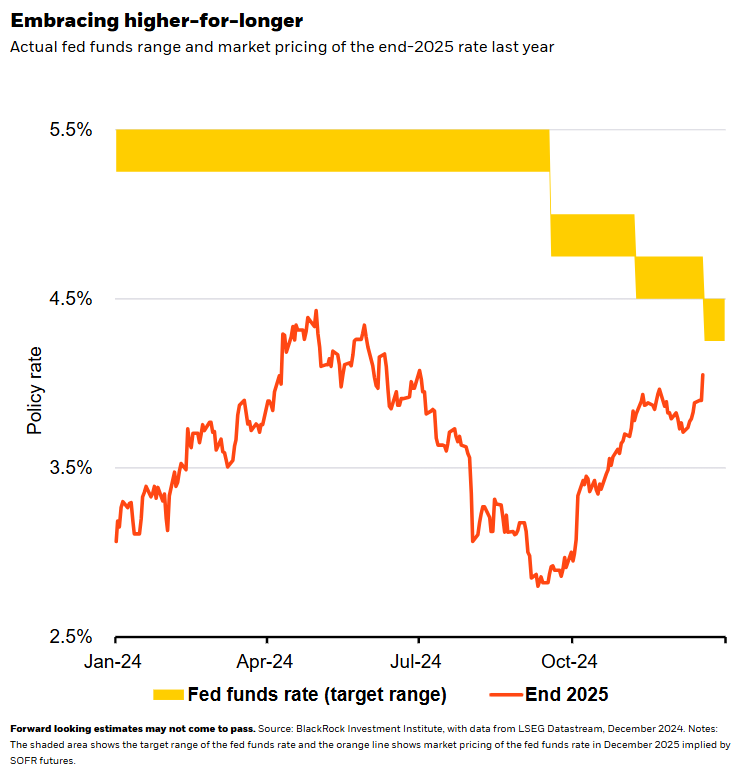

We enter 2025 against an unusual macro backdrop. In 2024, time-tested recession indicators failed, inflation fell even as growth stayed above the historical trend and the Federal Reserve cut rates by 100 basis points even though financial conditions were already easy. Incoming data that didn’t fit with a business cycle led to outsized market responses and abrupt shifts in narratives. This heightened market volatility creates plentiful investment opportunities, we think. Take fixed income. Fed rate cut expectations went on a historic round trip last year. See the chart. The Fed itself pivoted from talk of an easing cycle a year ago to a mere recalibration now. By year end, markets had come around to our higher-for-longer rate view. We expected inflation to cool some – as it did. Yet we long believed that sticky inflation would prevent sharp Fed rate cuts and leaned against market pricing for most of the year.

2024’s round trip in rate cut pricing shows this is not a business cycle but a transformation – our first lesson. We see mega forces, or structural shifts, reshaping economies and markets. This transformation could keep shifting the long-term activity trend, making a wide range of outcomes possible. Last year, we focused on key stock drivers: strengthening corporate earnings and free cash flow growth. This led us to stick with companies delivering on earnings even when valuation concerns flared up. We stay risk-on as we think U.S. corporate strength is the scenario most likely to play out next year. Yet we eye signposts, including greater trade protectionism, to change our view if other scenarios appear more likely. Structural changes mean rethinking long-held investment principles – like the assumption growth will eventually revert to its historical trend.

Leaning against a cyclical view

We lean against markets interpreting data through a business cycle lens, our second lesson. Such an interpretation last year spurred recession fears and brief stock selloffs. That played out in December, too, with the sharpest stock slide in decades to follow a Fed cut during a bull market, our analysis shows. Our U.S. equity overweight isn’t shaken by the Fed’s signal of fewer rate cuts – we had expected that. Our overweight is grounded in the artificial intelligence (AI) theme, robust economic growth and broadening earnings growth. Soaring tech valuations and the concentration of returns in just a few tech companies caused some market jitters. Yet we see market concentration as a feature, not a flaw, of transformation.

Transformation can happen quickly. That is why our third lesson is to expect more volatility and surprises than usual as transformation widens the range of market outcomes in real time. A year ago, the word “hyperscalers” – or large tech firms investing billions in AI – had barely entered the public lexicon. Public policy is another area we expect to see swift change. We think policymaking could itself become a source of disruption and surprises – in an already more fragile world given heightened strategic competition between the U.S. and China. Trade protectionism is shaping up to be a key risk in 2025.

Our bottom line

We carry 2024’s lessons into 2025. We got clear evidence this is a transformation, not a business cycle. And we found it helps to lean against markets adopting a business cycle lens, eyeing more surprises as the transformation unfolds.

Market backdrop

U.S. stocks surged more than 20% over the course of 2024. Mega cap tech names led the way on the AI theme – even as stocks finished the year on a down note overall after the Fed signaled a slower pace of cuts ahead at its December meeting. Markets have brought up their year-end 2025 rate expectations to nearly 4%, in line with our higher-for-longer view. U.S. 10-year Treasury yields swung in a range of nearly 100 basis points during the year, closing out 2024 near 4.58%.

We get U.S. payrolls for December this week. Wage growth remains elevated due to an unexpected rise in immigration, in our view. While wage pressures have cooled some as immigration has slowed, they remain above the level that would allow inflation to fall to the Fed’s 2% target. Given the risk of resurging inflation from potential trade tariffs and the immigration slowdown continuing, market expectations of only two more Fed policy rate cuts in 2025 now seem reasonable, we think.

Week Ahead

Jan. 6: Global PMIs

Jan. 7: U.S. trade data; euro area CPI

Jan. 10: U.S. payrolls; University of Michigan sentiment survey

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 6th January, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.