ŻfinMalta National Dance Company, which is supported by MeDirect, presents Mortal Heroes, a brand new work by choreographer Sita Ostheimer, premiering at at Teatru Manoel on 23, 24 and 25 May 2025, with tickets available here.

Mortal Heroes is a work which is both explosive yet delicate and aggressive yet gentle, taking the audience on a journey in search of the ‘Other’ and provoking deep self-reflection and remembrance. Those who purchase tickets for this performance will also have the opportunity to attend an open rehearsal for free.

More information on ŻfinMalta, including details of the current programme of performances can be found at the Company’s website https://www.zfinmalta.org/

Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Glenn Purves – Global Head of Macro, Vivek Paul – Global Head of Portfolio Research and Nicholas Fawcett – Senior Economist, all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Binding economic rules : We expect a U.S. contraction this year given supply disruptions from tariffs. We stay overweight U.S. stocks as the artificial intelligence theme rolls on.

Market backdrop : Above-consensus U.S. payrolls data helped boost risk assets last week, with U.S. stocks climbing 3%. U.S. 10-year Treasury yields ended the week steady.

Week ahead : The Federal Reserve confronts sharpening policy tradeoff it between weaker activity and sticky inflation at its meeting this week as seen in the Q1 GDP data.

The trade conflict between the U.S. and China is causing major economic disruptions. If tariffs stay at current levels, we expect a supply-driven contraction in U.S. activity this year. Yet this is very different from a typical business cycle recession given Covid-like supply constraints. Hard economic rules binding on policy may limit the damage. The AI mega force keeps us overweight U.S. stocks and positive on developed market stocks, even with more volatility likely.

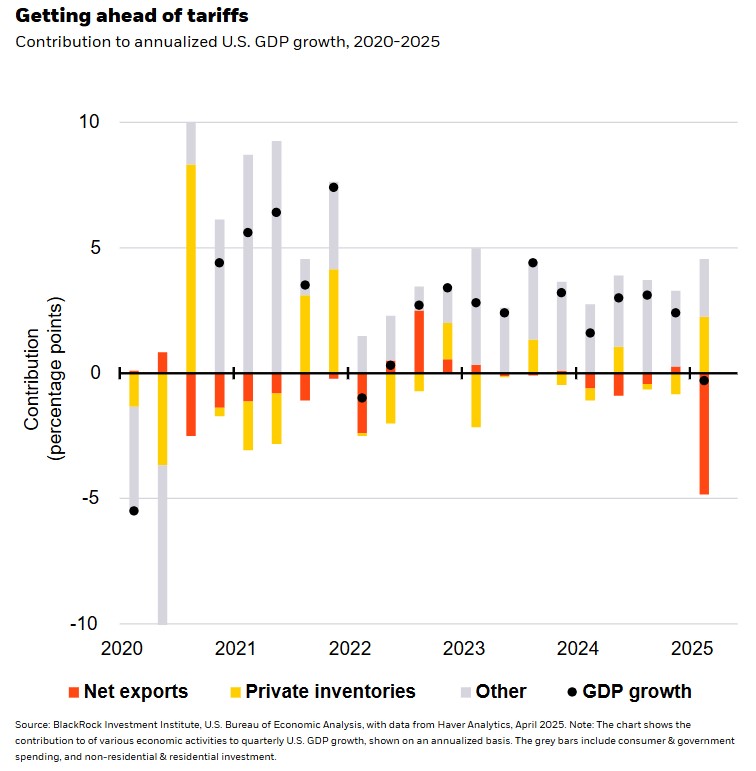

U.S. tariffs and uncertainty initially sparked concerns about waning confidence and declining demand. That’s now evolving into supply-driven disruptions, akin to the difficulties U.S. companies faced getting inputs for goods during the Covid-19 shock. Case in point: Companies rushed to import goods during Q1 to get ahead of tariffs, leading to a record surge in imports. See the orange bar in the chart. Along with a surge in inventories, we expect more volatility in activity data that don’t yet reflect the ensuing disruptions since the April 2 tariff announcement, especially the maximal U.S. stance on China. If current steep tariffs stay in place between the U.S. and China, we see a supply-driven economic contraction tied to trade-related disruptions like the Covid-19 shock. This contraction is not a typical business cycle recession – and one we can look through on a tactical horizon.

We expect a contraction marked by production shutdowns, bottlenecks and shortages like during the pandemic – though spending on services won’t be as directly affected. Activity may also restart quickly as it did during the pandemic. These supply-driven elements could bolster the inflationary pressure from tariffs, building on already high inflation. That presents the Fed with a sharper trade-off between protecting growth by coming to the rescue with rate cuts and reining in inflation. We track a range of indicators – like port traffic, capital spending plans and high-frequency financial and consumer spending data – to monitor how the supply-driven shock ripples out. This reinforces the hard economic rule that supply chain dependencies can’t be rewired quickly without disruption. If these rules constrain negotiations, damage could be limited.

A sectoral story

Some sectors are more exposed to tariffs than others – with sectoral differences already at play in Q1 earnings reports. The companies at the forefront of the AI mega force have largely kept driving U.S. equity strength, while policy uncertainty weighs more heavily on the rest of the market. Some big tech companies have beat Q1 earnings expectations, noted surging AI-driven demand and announced plans to increase AI-related investment. That underscores how the AI mega force persists, even with major supply-driven disruptions – keeping us positive on developed market (DM) stocks, especially the U.S. On the flip side, automakers are among the most exposed to key supply inputs from China, with some flagging the impact of tariffs in their full-year earnings guidance. The longer policy uncertainty lasts, the deeper the damage could be.

We have evolved our views as markets have adjusted to uncertainty. Just two days after April 2, we reduced risk by cutting our tactical horizon to three months. Yet the 90-day tariff pause showed economic rules can spur changes in policy. That led us to return our tactical horizon to six to 12 months to dial up exposure to developed market stocks. On a longer-term horizon, key questions remain about the best way to tap into an economic transformation, if investor bias for domestic assets will prevail, the outlook for the U.S. dollar’s haven status, and investing in private markets amid structurally higher interest rates.

Our bottom line

We expect tariffs at current levels to spur a supply-driven contraction this year, while supply disruptions boost inflation. The AI theme keeps us positive on DM stocks, especially the U.S., though more volatility is likely ahead.

Market backdrop

The above-consensus U.S. payrolls data helped boost risk assets and offset a drop in some tech shares on concerns about the tariff impact. The S&P 500 climbed 3% last week, closing the gap with where it was before April but still down 8% from the February all-time highs. U.S. 10-year Treasury yields ended the week at 4.31%, up about 40 basis points from their April lows. Markets have priced out some Federal Reserve rate cuts and now see a first quarter-point cut coming as soon as July.

The Federal Reserve takes center stage this week. Last week’s U.S. Q1 GDP report showed major disruptions to activity even before the April 2 tariff announcement, sharpening the tradeoff the Fed faces between lower growth and higher inflation. Even with the contraction of activity we expect, we don’t see the Fed cutting rates as much as the market is pricing in. U.S. and China trade data for March will reflect some of the frontloading of U.S. imports before the tariffs.

Week Ahead

May 6 : U.S. trade data

May 7 : Federal Reserve policy decision

May 8 : Bank of England policy decision

May 9 : China trade data

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 5th May, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.

You are leaving medirect.com.mt

Please be aware that the external site policies, or those of another MeDirect website, may differ from this website’s terms and conditions and privacy policy. The next website will open in a new browser window or tab.

Note: MeDirect is not responsible for any content on third party sites, nor does a link suggest endorsement of those sites and/or their content.

We strive to ensure a streamlined account opening process, via a structured and clear set of requirements and personalised assistance during the initial communication stages. If you are interested in opening a corporate account with MeDirect, please complete an Account Opening Information Questionnaire and send it to corporate@medirect.com.mt.

For a comprehensive list of documentation required to open a corporate account please contact us by email at corporate@medirect.com.mt or by phone on (+356) 2557 4444.