Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist and Paul Henderson – Senior Portfolio Strategist, forming part of the BlackRock Investment Institute and Robert Mitchnick – Head of Digital Assets at BlackRock share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Stablecoin legislation : Recent U.S. law cements the role of stablecoins as a means of digital payment in the future of finance. We still see bitcoin as a potential return diversifier.

Market backdrop : U.S. stocks pushed to all-time highs, partly on signs of big tech companies upping AI investment plans. Japanese stocks also hit record highs.

Week ahead : We expect the Fed will hold rates steady this week. We watch for U.S. trade deals as the Aug. 1 deadline approaches and for tariff impacts in Q2 GDP data.

New U.S. legislation – notably this month’s Genius Act – is cementing the role of stablecoins as a payment method in the future of finance, one of five mega forces we see driving returns. Stablecoins are pegged to major currencies, mainly the U.S. dollar and could solidify its dominance in global markets, though other countries are exploring alternatives. We think rising demand for stablecoins will have little impact on short-term Treasury yields. We still see bitcoin as a distinct return driver.

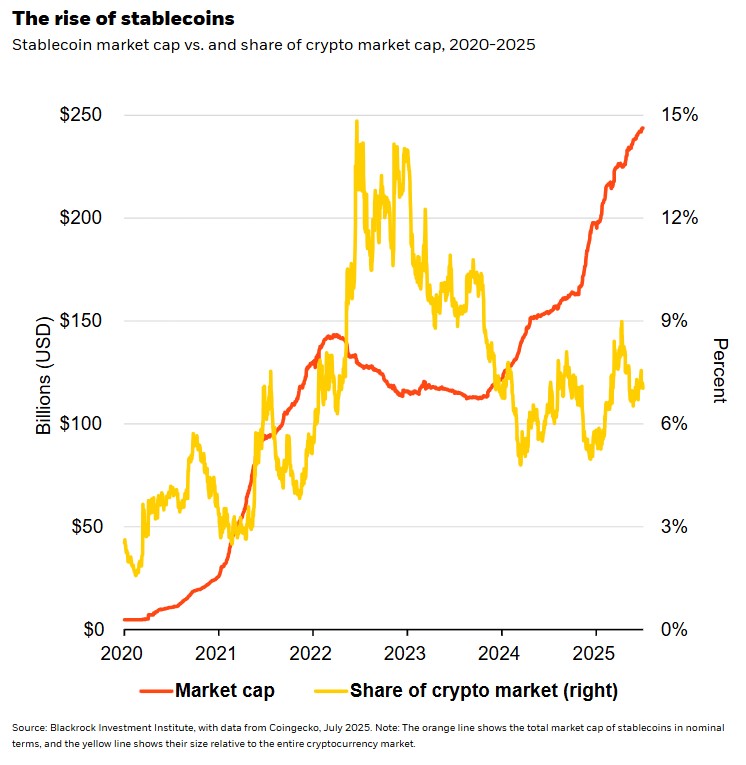

This has been a banner year for bitcoin, up 25% this year as the U.S. is in the process of adopting a couple of key laws aimed at bringing digital payments and assets into the mainstream – and making the U.S. the crypto capital of the world. One determines which financial regulator oversees different digital assets. That bill is still working its way through Congress. Another – the Genius Act, signed into law earlier this month – creates a comprehensive payment stablecoin framework. Stablecoins are digital tokens pegged to a fiat currency and backed by reserve assets. They fuse the frictionless transfer of crypto with the perceived stability of fiat currency. Though stablecoins are small relative to the size of the overall crypto universe at a 7% share, their adoption has grown quickly since 2020 to reach about $250 billion. See the chart.

We see two implications of the Genius Act on the U.S. dollar and Treasury bills. The act defines stablecoins to function as a payment method, not an investment product; prohibits issuers from paying interest; and limits issuance to federally regulated banks, some registered nonbanks and state-chartered firms. This regulation could reinforce dollar dominance by enabling a tokenized U.S. dollar-based ecosystem for international payments. Users in emerging markets may get easier access to the U.S. dollar over volatile local currencies. Yet in major economies, adoption may be limited by the ban on interest payments, which aims to prevent a low-friction rival that could compete with bank deposits and hurt traditional lending.

Implications of the Genius Act

The act also spells out what assets stablecoin issuers may hold in reserve: mostly repurchase agreements, money market funds and U.S. Treasury bills with a maturity of 93 days or less. Leading stablecoin issuers Tether and Circle together hold at least $120 billion in Treasury bills, only about 2% of the Treasury’s roughly $6 trillion bills outstanding. That demand could grow with the stablecoin market and spur new buying of bills – but the impact on yields will likely be limited. First, stablecoin demand for bills is likely to be offset by money shifting from similar assets, so little net new demand. Second, bill issuance is set to keep surging due to the Treasury’s preference to boost the funding of persistent deficits with more short-term debt.

The U.S. is not alone in acting. Hong Kong’s new regulation aims to attract stablecoin innovation. Europe is exploring a digital euro, though its use would be limited to avoid hurting banks. If other countries permit interest-bearing stablecoins or pursue central bank digital currencies, it could weaken the dollar’s role in trade finance, though the U.S. could then permit interest.

This wave of mainstreaming digital assets – through a regulatory framework and U.S. administration support – bodes well for greater adoption, the core investment case we see for bitcoin and helping make it a distinct driver of risk and return in portfolios. Stablecoins are still a relatively small part of the broader crypto universe – and as this evolves it’s not clear how stablecoins will compete with other digital assets.

Our bottom line

We see stablecoins as a new part of the future of finance – and new U.S. legislation is aiming to put the U.S. at the center of digital asset innovation. We still see bitcoin adoption as a distinct driver of risk and return.

Market backdrop

U.S. stocks pushed to fresh all-time highs, with the S&P 500 now up about 8% for the year. Alphabet’s planned increase in capital spending gave another boost to the AI trade. Japanese stocks soared after the U.S. and Japan struck an agreement on trade at tariffs below what the U.S. had been pushing for previously. The Topix index gained 4% on the week. U.S. Treasury yields were mostly steady, with the 10-year yield at 4.40% and now hovering within a range of roughly 4.20% to 4.60%.

We see the Federal Reserve holding rates steady as tariff-related inflation pressures begin surfacing in U.S. inflation data. We expect a modest rebound in U.S. Q2 GDP after it shrank in Q1 but watch for tariff impacts on consumption and investment. We are watching for U.S. trade deals as the Aug. 1 deadline approaches. And we look for signs of a Bank of Japan rate hike within the year given last week’s U.S.-Japan trade deal, though our base case remains early 2026.

Week Ahead

July 29 : U.S. consumer confidence

July 30 : Fed policy meeting; U.S. Q2 GDP; euro area Q2 GDP

July 31 : U.S. PCE and ECI; Bank of Japan policy meeting

Aug. 1 : U.S. payrolls

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 28th July, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.