Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist and Nicholas Fawcett – Senior Economist, forming part of the BlackRock Investment Institute and Tony DeSpirito – Global Chief Investment Officer of BlackRock Fundamental Equities share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Resilient U.S. earnings : U.S. corporate earnings resilience persists as tariff impacts become clearer. We stay overweight U.S. stocks but get granular while assessing the tariff fallout.

Market backdrop : U.S. stocks fell and bond yields slid after soft U.S. jobs data suggested slowing activity. We see many macro crosscurrents at play, muddying the outlook.

Week ahead : U.S. trade data will show how much tariffs are impacting imports. The Bank of England is expected to cut policy rates.

We see risk assets in a tug-of-war between solid U.S. corporate earnings, powered by the artificial intelligence (AI) theme, and tariffs hurting growth while lifting inflation. Q2 earnings results suggest the AI theme is winning, but questions remain about who will pay for tariffs. Early signs indicate a mix of consumers and companies. We think U.S. corporate strength could cushion the blow and stay overweight the AI theme and U.S. stocks. We get granular when eying the tariff hit.

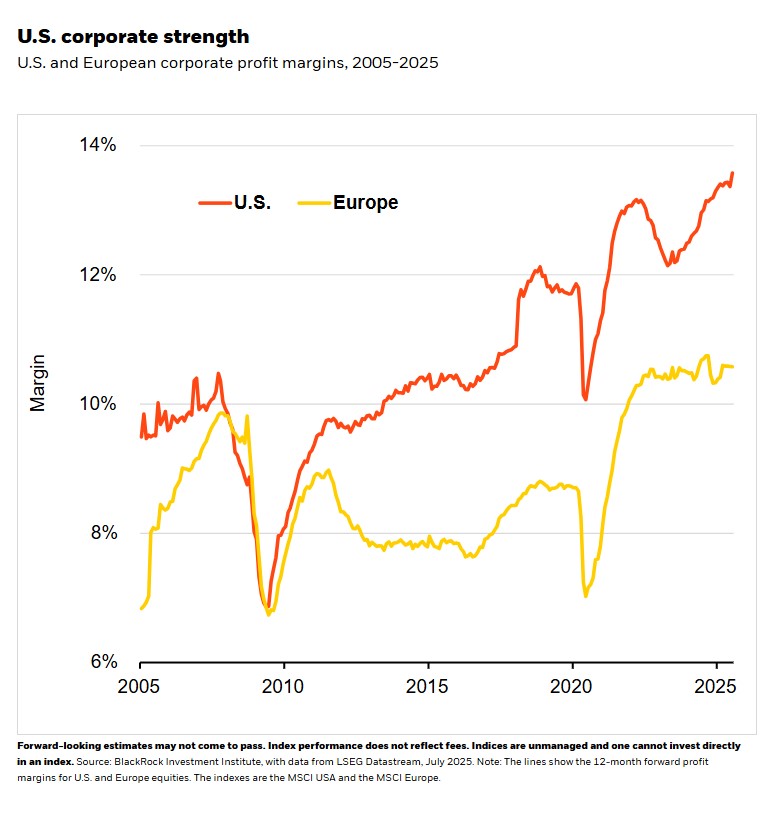

The U.S. “reciprocal” tariffs announced on April 2, which stoked historic market volatility, are now taking shape as the U.S. reaches agreements or imposes higher levies. U.S. tariffs on imports are now ending up at an effective rate around 15-20%, higher than we expected earlier this year, and generated revenues of $27 billion in June, Treasury data show. That means someone is paying the tariffs – and how much they hurt growth and stoke inflation will depend on who pays. Ultimately it is some mix of foreign suppliers, U.S. companies via profit margins and consumers via inflation. Yet U.S. corporate earnings are robust: Q2 U.S. earnings are up about 8% year-over-year even with tariffs, LSEG data show. U.S. profit margins are at record highs relative to flat margins in Europe. See the chart. U.S. mega cap tech is lifting AI investment as seen with Microsoft and Meta last week.

The slew of trade agreements announced in recent weeks removes some of the uncertainty of the ultimate effective landing zone for tariffs – even if they’re several times higher than where they were at the end of 2024. The tariff impact on U.S. consumers has been slow to show up in part because companies rushed to import goods before expected tariffs in April. Tariffs do not apply to ships that left the port, shipping can take several weeks and companies can delay payments even when goods arrive. Many have not yet raised prices until they have greater clarity. Yet that offset is fading: second quarter U.S. inflation data showed durable goods prices rising at the fastest pace since 1991 outside the pandemic. So consumers are starting to pay some of the tariff costs, especially in household appliances and electronics. And companies have also started paying: global automakers, some of the most exposed to tariffs, are reporting large earnings writedowns.

Why earnings resilience matters

Automakers highlight how complicated the tariff story is. U.S. automakers like General Motors and Ford are among those taking the large profit hits as tariffs are implemented – and chose to eat the tariffs. Japanese and South Korean automakers are absorbing tariff costs by cutting the prices of the vehicles they sell to the U.S. This pressure on pricing is especially acute in Europe where automakers battle with China’s cheaper electric vehicles and are constrained in raising prices. By contrast, quality producers like Ferrari are lifting prices – highlighting the importance of pricing power.

This is why corporate earnings resilience matters, in our view. Automakers are manufacturers. The industrials sector – where supply chains are among the most integrated globally – is dominated by manufacturers and is likely feeling the biggest impact of tariffs. And yet the industrials sector is the best-performing S&P 500 sector this year, up some 15% compared with 6% for the index, according to LSEG data. Why? Industrials benefit from the AI buildout and other key themes driven by mega forces, such as geopolitical fragmentation and the boost to defense spending this year. That’s why this environment favors getting granular with views below the sector level and favors an active approach to achieving returns.

Our bottom line

We see a tug-of-war between the economic drag of tariffs and U.S. corporate earnings strength driven by AI. The latter is winning so far, in our view, but getting granular views is key as companies and consumers each eat tariff costs.

Market backdrop

U.S. stocks retreated for the week after pushing to new all-time highs, with the S&P 500 down about 2% for the week. Surprisingly weak payrolls data put stocks under pressure and pushed down Treasury yields on expectations for Federal Reserve rate cuts. We think the payrolls data shows activity slowing but that there are several crosscurrents at play when it comes to inflation (sticky wage growth, tariffs) and for risk assets (the AI theme holding up even as activity has slowed).

The Bank of England (BoE) is expected to cut interest rates by a quarter-point this week. We think sluggish economic growth and some signs of softening inflation pave the way for a rate cut. Yet persistent inflation pressures will keep interest rates higher for longer and limit how far the BoE can cut rates. U.S. trade data for July will show how much tariffs are slowing imports, with early data showing a sharp drop during the month.

Week Ahead

Aug. 4 : China Caixin services PMI

Aug. 5 : U.S. trade data

Aug. 7 : Bank of England policy decision

Aug. 8 : China July CPI

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 4th August, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.