Portfolio Manager Denny Fish highlights how 2025 is becoming a seminal year for artificial intelligence (AI) as these models’ deployment in the broader economy is being met with robust demand, resulting in monetisation, weighs in on the implications for investors—and why lengthening duration may make sense.

Denny Fish is a Portfolio Manager on the Global Technology and Innovation Team at Janus Henderson Investors, a position he has held since 2016. He also serves as a Research Analyst and leads the firm’s Technology Sector Research Team. Prior to rejoining Janus in 2016, Denny served as a technology equity analyst and co-portfolio manager at RS Investments. From 2007 to 2014, he was an equity research analyst and co-team leader of the Janus technology research sector team. Before he was first employed by Janus in 2007, Denny was director and senior research analyst at JMP Securities covering enterprise software. Earlier in his career, he worked at Oracle Corporation as a technology sales manager.

Denny received his Bachelor of Science degree in civil engineering from the University of Illinois and his MBA from the University of Southern California, Marshall School of Business. He has 21 years of financial industry experience.

For much of the past three years, AI has been the story in global equity markets. Far more than just capturing headlines, AI-related stocks – especially the megacap hyperscalers – have been responsible for a large portion of aggregate market returns over this period.

Despite this remarkable run – and as evidenced by a brief early 2025 dip – many investors are trying to decipher something of a paradox within the AI story: How can a long-duration theme playing out over a multi-decade horizon be also advancing at such a rapid pace that the goal posts seemingly move every few months?

In this instance, both statements are true. It will take years for the AI theme to unfold, but the rapid adoption of this revolutionary technology has surprised even some of AI’s biggest cheerleaders.

“If you build it…”

Reconciling this secular vision and real-time deployment comes to a head in the historic amount of capital expenditure (CapEx) allocated to bring an AI future to bear. The capital investment debate was also behind the early 2025 volatility as the market questioned the scale of the investment, especially in the wake of China’s DeepSeek purportedly achieving impressive results on the cheap.

While the DeepSeek episode ultimately proved to be a head fake – the Chinese model relied heavily upon Western platforms – it came at a time when some in the investment community were expecting incremental CapEx to diminish as AI moved from the training phase to the inference, or reasoning, phase. That has emphatically turned out not to be the case.

One of the revelations of 2025 has been a resetting of expectations for the computing power required for AI reasoning. Behind this recalibrated outlook was test-time inference. Rather than AI’s operational phase riding on the coattails of the computation-heavy training stage, increasingly complex models now exhibit the ability to think through problems, with each iteration producing data that can be referenced for future uses. This process will require a massive amount of additional CapEx.

In 2024, 100,000 graphic processing units (GPUs) would have been considered a large data cluster for AI compute. That number is now a million GPUs, with some estimates calling for double that amount in the near future. Such a concentration of computing power requires a commensurate amount of energy. The electricity generation required to support AI clusters will be measured not in megawatts but gigawatts. The current mismatch between existing power supply and skyrocketing demand has led to an arms race among tech hyperscalers seeking to secure sufficient generation capacity.

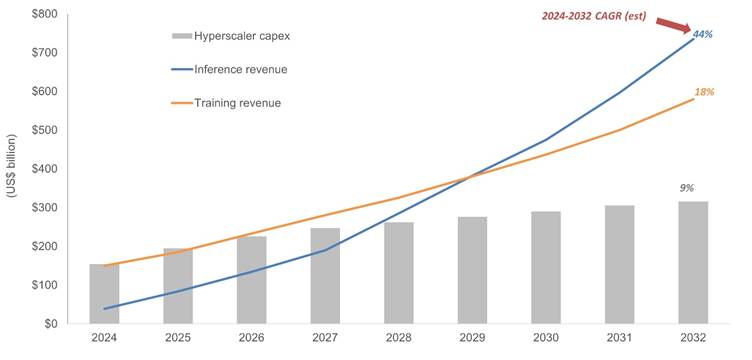

AI-related revenues and CapEx forecasts (2024-2032)

The expectation that the CapEx required to sustain AI models would level off once the training phase matured and has been upgraded as it’s now apparent that inference would require massive investment. Conservative estimates call for roughly $2.5 trillion over the next eight years, with more bullish forecasts calling for three times that amount.

Source: Bloomberg Intelligence, McKinsey, Janus Henderson Investors; as of 31 July 2025. Note: 2025-2032 projections for price levels and growth rates are estimates.

From this perspective, the level of investment slated by the AI heavyweights, in our view, is the downpayment required to reap the economic returns expected from an AI-enabled future. As evidenced by some innovative approaches taken by DeepSeek, efficiencies will no doubt be uncovered. But rather than experience sticker shock at some of the dollar amounts allocated to AI capex, investors should recognise there are two sides to the equation: investment and return. As with any secular theme – especially one so potentially transformative – returns will be measured over a decade-plus horizon. And there is a realistic possibility that many valuation models underestimate the durability of AI’s economic benefits over this horizon.

Enablers – and early adopters

Another reason behind the market’s early 2025 consternation surrounding AI CapEx was the question of when returns on this investment would begin to materialise. The answer came with the most recent wave of tech-sector earnings reports. Companies like Microsoft revealed that not only are AI investments leading to monetisation, but deployed capacity has been met with robust demand, and managers expect this to continue for the foreseeable future.

In this respect, the tech sector has assumed the dual role of AI enabler – for the broader economy – and early beneficiary within its own operations. While CEOs across sectors have prioritised developing an AI strategy, tech companies have a head start due to their greater familiarity with these novel platforms.

Many tech players are already seeing AI-related productivity gains flow through to margins. In fact, we believe that the market still underappreciates the degree to which the operating leverage inherent in AI will be accretive to margins. Couple that with the ability of front-office AI capabilities to grow revenues, and we see a scenario where long-term aggregate earnings growth resets to a materially higher level. These financial benefits are unfolding today within the tech sector but will invariably spread to other industries as corporate managers solidify their AI strategies.

For a select subset of tech hyperscalers, another prize will be achieving artificial general intelligence (AGI). While this breakthrough won’t be a winner-take-all scenario, it will put those that can deliver AGI to the market in a commanding position. Meanwhile, most AI platforms are concurrently developing their own niches, meaning each is likely to develop a stable customer base that aligns with their particular model’s capabilities.

Beyond the boardroom

This past year has proven that developing an AI strategy is not just a corporate priority. Sovereign AI has become a strategic imperative as countries recognise the significant benefits and manifold risks presented by the advent of this technology. Governments rightly believe that AI will impact their countries’ economic, social, and security interests.

Many countries will want to achieve AI autonomy, while others will seek ways to form partnerships to ensure access to the technology and fortify national initiatives. For example, after initially seeking to block access to the most advanced chips, the U.S. now appears to champion a strategy of getting other countries to utilise its AI infrastructure to cement is leading position.

Schumpeter’s maxim for the twenty-first century

Investors may cheer at AI’s potential to improve global economic growth. But as has been the case with other stages of the ongoing digital revolution, some companies, through thoughtful strategy, will find themselves on the winning side of AI, while others will fail to grasp the magnitude of this sea change and find their business models vulnerable. This bifurcation is playing out today within the tech sector as hyperscalers compete for the most potent models. Over the next several years it will spread to all corners of the global economy and broader society.

The widely anticipated productivity gains are likely to represent a net positive for the economy. But there will be a cost in the form of the “creative destruction” that Joseph Schumpeter foresaw nearly a century ago. Given the breadth of change afoot – and the scale of the economic stakes – investors should be both excited about AI’s promise and clear-eyed about its ability to upend myriad business models, industries, and economic paradigms.

Equity securities are subject to risks including market risk. Returns will fluctuate in response to issuer, political and economic developments.

Technology industries can be significantly affected by obsolescence of existing technology, short product cycles, falling prices and profits, competition from new market entrants, and general economic conditions. A concentrated investment in a single industry could be more volatile than the performance of less concentrated investments and the market as a whole.

Volatility measures risk using the dispersion of returns for a given investment.

Janus Henderson Key risks & Disclaimers:

The views presented are as of the date published. They are for information purposes only and should not be used or construed as investment, legal or tax advice or as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector. Nothing in this material shall be deemed to be a direct or indirect provision of investment management services specific to any client requirements. Opinions and examples are meant as an illustration of broader themes, are not an indication of trading intent, are subject to change and may not reflect the views of others in the organisation. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio. No forecasts can be guaranteed and there is no guarantee that the information supplied is complete or timely, nor are there any warranties with regard to the results obtained from its use. Janus Henderson Investors is the source of data unless otherwise indicated, and has reasonable belief to rely on information and data sourced from third parties. Past performance does not predict future returns. Investing involves risk, including the possible loss of principal and fluctuation of value.

Janus Henderson Investors is the name under which investment products and services are provided by the entities identified in the following jurisdictions in Europeby Janus Henderson Investors International Limited (reg no. 3594615), Janus Henderson Investors UK Limited (reg. no. 906355), Janus Henderson Fund Management UK Limited (reg. no. 2678531), (each registered in England and Wales at 201 Bishopsgate, London EC2M 3AE and regulated by the Financial Conduct Authority), Tabula Investment Management Limited (reg. no. 11286661 at 10 Norwich Street, London, United Kingdom, EC4A 1BD and regulated by the Financial Conduct Authority) and Janus Henderson Investors Europe S.A. (reg no. B22848 at 78, Avenue de la Liberté, L-1930 Luxembourg, Luxembourg and regulated by the Commission de Surveillance du Secteur Financier).

MeDirect Disclaimers:

This information has been accurately reproduced, as received from Janus Henderson Investors. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.