Wei Li – Global Chief Investment Strategist with Roelof Salomons – Chief Investment Strategist for the Netherlands, Bruno Rovelli – Chief Investment Strategist for Italy and Simon Blundell – Head of European Fundamental Fixed Income, all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Bright spots in Europe: Our U.S. equity overweight has played out this year – and so have other preferences in Europe that we stick with, including credit and financial stocks.

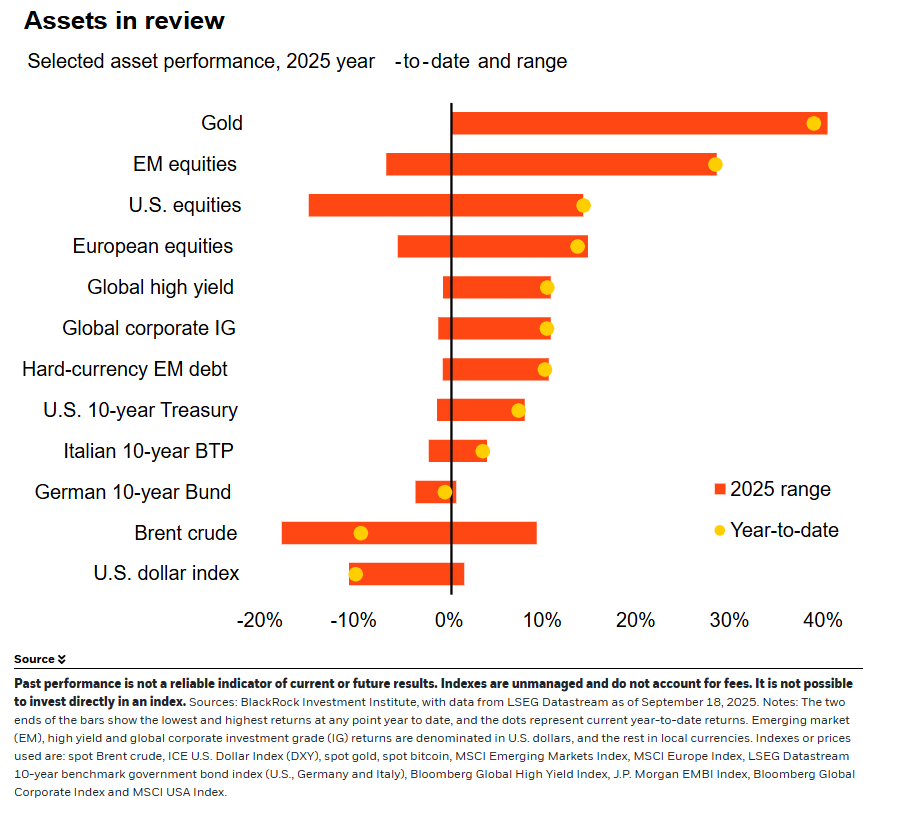

Market backdrop: U.S. stocks surged to all-time highs and U.S. 10-year Treasury yields edged up after the Federal Reserve resumed rate cuts. Gold also surged to new highs.

Week ahead: We eye U.S. PCE inflation data. Cooling services inflation contributed to the Fed’s decision to cut rates. We look to see if it persists or picks back up.

The Federal Reserve’s restart of policy rate cuts supports our tactical upgrade to long-term U.S. Treasuries and risk-on stance. Yet opportunities abound outside the U.S. A weaker U.S. dollar has been a boon to international markets, and we eye opportunities in Europe for dollar-based investors. We still prefer euro area credit over the U.S. but close our preference for peripheral over core government bonds. We also still favor financials and industrials stocks, and Spain at the country level.

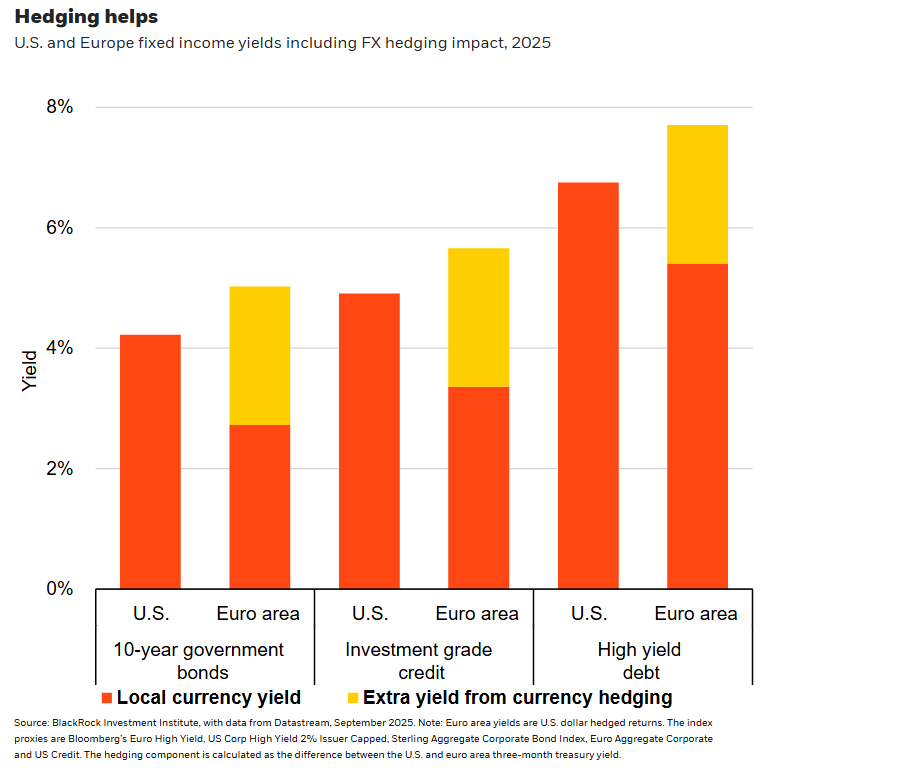

Our core risk stance has leaned on U.S. equities and the AI theme. Yet a weaker U.S. dollar has unlocked international opportunities for dollar-based investors – both in emerging markets and in Europe. Higher U.S. policy rates keep the gap with euro area rates wide, even after the Fed resumed rate cuts. The European Central Bank is set to hold rates at 2%, well below the Fed’s 4.00-4.25% even if it cuts more. That large interest rate differential benefits U.S. investors. Why? Hedging foreign bonds back into U.S. dollars captures this differential and boosts the income they offer. That raises the income on offer in Europe even above the U.S. – euro investment grade credit yields are near 6% – and contributed to our relative preference for fixed income in Europe. See the chart. Yet granularity is key. We stay neutral euro area government bonds overall and keep favoring credit and select equity sectors.

We close our long-held relative preference for peripheral euro area government bonds over the core. Stronger growth in Spain and Greece and relative political stability in Italy had driven yields down relative to French and German yields more than a decade after the region’s debt crisis. But yields and spreads now reflect that stability, in our view. France is facing political gridlock stymying efforts to trim debt, while Germany has embraced looser fiscal policy this year. But we think a lot of the risks in French bonds are priced in with its 10-year yields above those in Spain by the most since the euro was launched.

Credit over government bonds, Europe over U.S.

We prefer credit to government bonds globally and Europe over the U.S. Globally, the corporate sector has demonstrated greater creditworthiness than the public sector. Yes, defaults have increased since the pandemic, but the stress is concentrated among smaller issuers rather than larger companies, according to Moody’s. Wider spreads meant European credit offered investors better compensation for risk than U.S. credit. That view has since paid off: spreads in Europe have tightened sharply relative to the U.S. European high yield credit outperformed European government bonds by almost 3% year-to-date, whereas U.S. high-yield credit has outperformed U.S. Treasuries by less than 2%, Bloomberg data show.

In equities, Europe’s outperformance over the U.S. peaked in late March – but we still see granular opportunities we have liked since the start of 2025. Selectivity is essential. We favored three European sectors that have outperformed the U.S.: industrials (21% return, LSEG data show), utilities (19%) and financials (32%). European financials still benefit from healthy balance sheets, a stronger fee business and improving profitability. Industrials are getting a boost from Europe’s focus on defense, Germany’s infrastructure push and the AI buildout. By country, we prefer Spanish equities where these sectors are well represented. Another plus? Spanish equities have greater exposure to emerging markets, especially Latin America, that can benefit from easier Fed policy and potential further U.S. dollar weakness. We think relative valuations still do not reflect the country’s stronger economic growth and earnings compared with the rest of Europe – and see further upside.

Our bottom line

U.S. rate cuts support our risk-on stance, but we see ample – if select – opportunity in Europe. We favor EU credit and the income boost from currency hedging, as well as equity sectors including financials, industrials and utilities.

Market backdrop

U.S. stocks pushed to new all-time highs last week, with tech shares again leading the way and taking the S&P 500’s gains to 13% for the year. Gold prices also hit record peaks to take gains to 40% this year. U.S. 10-year Treasury yields edged up to around 4.15% after the Fed resumed rate cuts but signaled fewer cuts ahead than the market is pricing in. We think a further softening of the labor market will be key for the Fed to keep cutting rates.

We’re tracking U.S. August PCE this week after headline CPI inflation met expectations and jobless claims ticked higher. Tariffs are reviving goods inflation just as services inflation is proving sticky. But the recent easing in core services inflation could be more than temporary if the labor market cools further. That makes understanding the drivers of a weaker labor market and future productivity key to gauging the outlook for inflation and Federal Reserve policy.

Week Ahead

Sep. 23: Global flash PMIs

Sep. 25: U.S. durable goods

Sep. 26: U.S. PCE

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 22nd September, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.