MeDirect Bank’s Head of Regulatory Affairs & Sustainability, Cressida Galea, spoke at the first edition of Sustainability Live Malta. This event brought together stakeholders to discuss how Malta’s business community is adapting to the evolving realities around ESG, especially at a time of global uncertainty around how environmental, social and governance reporting is going to be regulated going forward.

Among other discussions and keynote addresses held throughout the event, Galea shared insights on the challenges and opportunities facing companies when it comes reporting on ESG matters. She highlighted the real challenges for reporting institutions, such as the cost of being compliant with EU regulations and the policy and legal uncertainty created by changing political priorities both within the EU and globally. The interoperability gaps and associated risks in terms of data duplication and overlap across different ESG frameworks were also tackled. However, despite these challenges, there is real value added from sustainability reporting as it makes organisations accountable to their customers and employees, ensuring genuine progress and improved competitiveness.

“What came out clearly from this first edition of Sustainability Live Malta was that we are now in a time of action. Embedding sustainability into core strategy should be seen as the most effective and most profitable business strategy. The future of sustainability reporting lies in moving beyond compliance checklists, and companies that recognise this shift can position themselves for long-term success. Although there may be short-term challenges, embracing ESG reporting as a strategic opportunity can help companies future-proof their operations. It is our collective duty, therefore, to ensure we are fully transparent about what we are doing and work with all stakeholders both within our organisations and the broader community we operate in to deliver tangible results,” said Galea.

Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Vivek Paul – Global Head of Portfolio Research and Roelof Salomons – Chief Investment Strategist for the Netherlands all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Upgrading European stocks: We still think U.S. equities can outperform in 2025, led by tech, even as Europe’s start the year strong. Yet we broaden our risk-on view, upgrading Europe stocks.

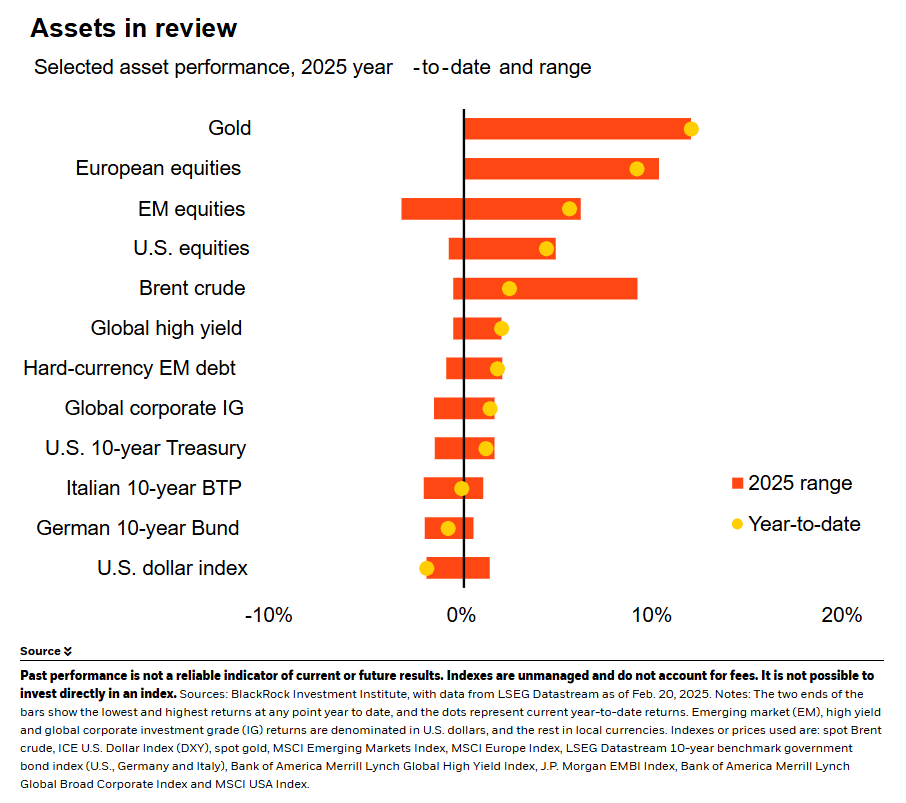

Market backdrop: U.S. stocks tumbled last week – now up about 3% for the year, versus nearly 9% in Europe. We see markets reflecting tariff concerns and an evolving AI story.

Week ahead: This week, we get U.S. PCE for January. Any pickup in inflation would provide more evidence that December’s CPI moderation was an outlier, in our view.

European equity gains have outpaced the U.S. to start 2025. We had said Europe’s stocks needed a catalyst to turn around poor sentiment. We now see several that – if they materialize – could boost cheap valuations, so we close our underweight on Europe’s stocks. Yet we still expect the U.S. to reclaim leadership this year and stay overweight U.S. stocks as corporate earnings strength and the artificial intelligence (AI) theme broaden out. We turn more underweight long-term U.S. Treasuries.

U.S. equities have long outperformed their global peers. Some pin that on tech’s greater share in its market, bigger fiscal spend in recent years and energy independence, but we would attribute it more to deeper capital markets and relative deregulation that promote risk-taking. We think the U.S. can keep its edge, even if the S&P 500 has lagged so far this year. Yet we believe Europe can close some of the return gap. With a lot of bad news priced into European equities, even prospects of good news could help them push higher. One example: Possible de-escalation in the Ukraine war. Reduced reliance on Russian gas brought European energy prices down from 2022’s highs. See the chart. A form of peace agreement could lower energy prices further, boosting European growth and lowering inflation. This is just one of several catalysts we think could broaden U.S. equity strength to Europe.

We eye other catalysts for European equities as well. We expect more defense spending as the U.S. has stated Europe is no longer a primary security priority. The EU now has an air of urgency that typically spurs action. In Germany, the weekend’s election result could herald fiscal loosening – though it’s a long and uncertain road there. Still sluggish euro area growth and easing inflation gives the European Central Bank room to cut rates more this year, we think. So, we go neutral Europe’s stocks and still favor European financials – a preference that also served us well last year. Yet Europe still faces multiple structural issues, from lagging competitiveness to potential U.S. tariffs – justifying some of Europe’s hefty valuation discount, we think.

Positive on the U.S.

Our assessment of the U.S. is unchanged: we expect mega-cap tech and other AI-linked stocks to keep driving U.S. equity returns, especially as AI adoption grows. But we also see signs of earnings strength broadening beyond tech. Analysts now expect tech to deliver 18% earnings growth this year versus 11% for the broader index, LSEG data show – a smaller gap vs. 2024. We think risk assets could also weather the higher growth and higher inflation mix we see as increasingly possible. New tariffs and U.S. policy shifts aimed at boosting growth, like deregulation, carry inflationary potential. Markets have embraced our higher-for-longer rate view, yet we still see term premium rising more than currently priced as investors demand more return for the risk of holding long-term bonds – even if the administration’s focus on long-term yields and talks of pausing quantitative tightening could delay some of the rise for now. We go further underweight long-term U.S. Treasuries as a result.

In China, apparent efficiency gains by AI startup DeepSeek have driven a surge in China’s tech sector. President Xi Jinping’s recent meeting with private sector business leaders could signal a more supportive regulatory backdrop, yet the broader environment of U.S.-China technology competition may present challenges. We evolve our tactical overweight to Chinese equities as tech excitement could keep driving returns, potentially reducing the odds of much-anticipated government stimulus. Over the longer term, we are more wary given structural challenges to China’s growth and tariff risks.

Our bottom line

We stay overweight U.S. equities, even with their softer start to 2025. Yet we think their lead over global peers could narrow this year. We upgrade European stocks to neutral while going further underweight long-dated U.S. Treasuries.

Market backdrop

The S&P 500 slid nearly 2% last week. The index is up 2.5% this year, but still lagging Europe’s Stoxx 600, which is up 8.5% year to date. Ten-year U.S. Treasury yields ticked down to 4.43%, about 40 basis points below 2025’s high. Hong Kong-listed Chinese stocks shook off a steep fall to rise 4% last week, up 22% in 2025. We think such moves reflect improving sentiment in Europe, concerns about potential U.S. policy changes and disappointing economic data, and the evolving AI theme.

This week, we get U.S. PCE for January. The latest U.S. CPI print came in hotter than expected, indicating that elevated wage pressures are still driving sticky inflation. We watch for whether PCE follows suit, which would point to December’s CPI moderation being an outlier. In Japan CPI data out this week, we expect a pickup due to rising food prices.

UK CPI is the main macro event on tap this week. Markets will be looking for signs of progress in the Bank of England’s (BOE’s) fight against inflation following last week’s 25-basis point policy rate cut. Even as UK inflation remains above the BOE’s 2% target, we think the UK’s weak growth outlook gives the BOE further room to cut policy rates this year. Japan trade data will also be in focus given the Trump administration’s plans to implement reciprocal tariffs, including on Japan.

Week Ahead

Feb. 25: U.S. consumer confidence; Japan service PPI

Feb. 27: U.S. durable goods

Feb. 28: U.S. PCE; Japan CPI

March 1: China manufacturing PMI

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 24th February, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.

This morning, we have eurozone CPI and Germany IFO and we will hear from the BoE’s Lombardelli, Ramsden, and Dhingra on Monday. Germany GDP and US consumer confidence are due on Tuesday. Central bank chatter includes: the ECB’s Nagel, Schnabel and Pill, and Fed’s Logan, Barr and Barkin. Nvidia earnings will likely take centre stage on Wednesday, and we have the US new homes sales print, and comments from the Fed’s Bostic, on the economic outlook, and the BoE’s Dhingra. US GDP, durable goods and initial jobless claims follow on Thursday, we also have the ECB’s policy minutes, and chatter from the Fed’s Schmidt, Hammock and Harker. Inflation prints from key European countries will garner market attention on Friday morning, and later we have US PCE inflation and income and spending figures which may shed some more colour on the state of the US consumers, whose resilience was called to question last week.

Following the weaker-than-expected retail sales figures, disappointing Walmart forecasts and the Uni. of Michigan prints, markets had a broadly risk-off week. The Uni. of Michigan consumer sentiment reading for February declined further to 64.7, while inflation expectations skyrocketed, with the 5-10 year figure to the highest level since 1995 at 3.5%. The preliminary S&P Global US services PMI also shocked, falling into contraction, to 49.7, versus expectations of 53. The yield on the 10-year UST closed 5bps stronger, closing at 4.43% on the week. Meanwhile, the S&P Index fell 1.66%. The dollar also closed marginally lower, for the third-straight week. Brent crude closed 0.41% lower on the week amid the prospect of Iraq increasing oil flow.

Elsewhere, China’s tech stocks rallied following President Xi’s meeting with private entrepreneurs and new supportive policies, while the country’s yield curve flattened due to rising short-term rates. The People’s Bank of China maintained its Loan Prime Rates despite persistent disinflation risks, though housing prices showed signs of recovery, particularly in tier-one cities. Meanwhile, US-China tensions escalated with the White House’s new ‘America First Investment Policy,’ which primarily targets Chinese investments and threatens to suspend the 1984 US-China Income Tax Convention.

EPIC Global Equity Fund (the “Fund”) is a sub-fund of EPIC Funds p.l.c. (the “Company”), which is an open-ended umbrella fund authorised in Ireland as a UCITS fund and regulated by the Central Bank of Ireland. This marketing material has been approved in the UK by EPIC Markets (UK) LLP, trading as EPIC Investment Partners, which is a limited liability partnership incorporated and registered in England and Wales under partnership OC306260 with its registered office at Audrey House, 16-20 Ely Place, London EC1N 6SN. EPIC Markets (UK) LLP is regulated by the Financial Conduct Authority. Distribution of this material and the offer of the Fund are specifically restricted in certain jurisdictions. In particular, but without limitation, neither this material nor shares in the Fund are available to US persons.

This document is for general information purposes only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. It is not a personal recommendation and it should not be regarded as a solicitation or an offer to buy or sell any shares in the Fund. This document represents the views of EPIC Investment Partners at the time of writing. It should not be construed as investment advice. Any person interested in investing in the Fund should conduct their own investigation and analysis of the Fund and should consult their own professional tax, accounting or other advisers as to the risks involved in making such an investment. Full details of the Fund’s investment objectives, investment policy and risks are set out in the Fund’s Prospectus and Supplement which, together with the Key Information Document (“KID”), are available on request and free of charge from Maples Fund Services (Ireland) Limited, 32 Molesworth Street, Dublin 2, Ireland and, in the UK, from EPIC Markets (UK) LLP, Audrey House, 16-20 Ely Place, London EC1N 6SN. Any offering of the Fund is only made on the terms of the current Prospectus, Supplement and KID. A subscription in the Fund can only be made after the provision of the KIID and should be made solely upon the information contained in the Prospectus, Supplement and KID.

An investment in the Fund is not suitable for an investor who cannot sustain a loss on their investment. There is no guarantee of the Fund’s future performance and past performance is not a reliable indicator of future performance. The value of your investment and the income derived from it can go down as well as up, and you may not get back the money you invested. The risks associated with making an investment in the Fund are described in the Prospectus and Supplement but investors should note, in particular, the following: 1) Foreign currency denominated investments are subject to fluctuations in exchange rates that could have a positive or an adverse effect on an investor’s returns. There is also a risk that currency hedging transactions for one share class may in extreme cases adversely affect the net asset value of the other share classes within the same sub-fund since there is no legal segregation between share classes; 2) The Fund is subject to the risk of the insolvency of its counterparties; and 3) Emerging market securities are subject to greater social, political, regulatory, and currency risks than developed market securities. This may impact the liquidity and value of such securities and, consequently, the value of the Fund.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from EPIC Investment Partners. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.

You are leaving medirect.com.mt

Please be aware that the external site policies, or those of another MeDirect website, may differ from this website’s terms and conditions and privacy policy. The next website will open in a new browser window or tab.

Note: MeDirect is not responsible for any content on third party sites, nor does a link suggest endorsement of those sites and/or their content.

We strive to ensure a streamlined account opening process, via a structured and clear set of requirements and personalised assistance during the initial communication stages. If you are interested in opening a corporate account with MeDirect, please complete an Account Opening Information Questionnaire and send it to corporate@medirect.com.mt.

For a comprehensive list of documentation required to open a corporate account please contact us by email at corporate@medirect.com.mt or by phone on (+356) 2557 4444.