Wei Li – Global Chief Investment Strategist of BlackRock Investment Institute together with , Glenn Purves – Global Head of Macro, Ben Powell – Chief Investment Strategist for the Middle East and APAC and Nicholas Fawcett – Senior Economist, all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Volatile new regime : Recent swings in U.S. inflation highlight the volatile economic backdrop, even before the full tariff impact. We tap into mega forces that keep driving returns.

Market backdrop : Global stocks slid last week, led by Europe, after Israel launched an attack on Iran’s nuclear infrastructure. Oil future prices jumped more than 11%.

Week ahead : We are keeping an eye on any escalation between Israel and Iran. We think the Fed will hold rates steady again this week as it waits to see the impact of tariffs.

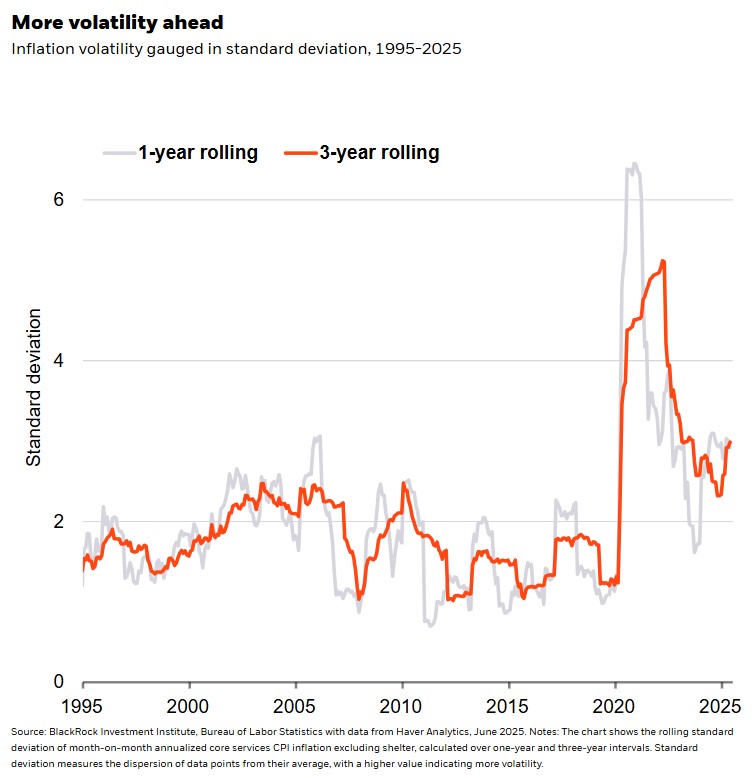

Swings in U.S. CPI data reflect the elevated macro uncertainty we’ve long flagged. Inflation data don’t yet reflect the full tariff impact. Together with renewed conflict in the Middle East, that signals more volatility ahead. We think the Federal Reserve will sit tight this week as it waits for clarity. And ongoing inflation pressures from a tight labor market will limit how much it can cut rates. Looking through the noise, we still see mega forces like AI driving returns, keeping us overweight U.S. stocks.

The May U.S. CPI rose less than expected last week, yet monthly data has been volatile since the pandemic. See the chart. Noisy economic data reflect the volatile new regime we’ve long noted. We expect this to persist. Wage pressures remain too high for inflation to settle at the Fed’s 2% target, with the gap between core and wage inflation near its widest in four years. The data showed signs of tariffs starting to lift consumer prices, like for appliances, but the full impact is still to come. Surveys by the National Federation of Independent Business suggest companies are ready to hike prices in response to tariffs, but they may delay that and workforce changes as they await clarity on tariffs. Longer term, we see ongoing inflation pressure from mega forces like the AI buildout, aging populations and geopolitical fragmentation. Latest example: the Israel-Iran conflict and potential oil price rises.

U.S. growth hasn’t been immune to volatility, with quarterly data going from holding up to contracting in the past year. Evolving U.S. trade policy is one source of uncertainty, yet hard economic rules – like how supply chains cannot be rewired quickly without disruption – act as a constraint, as we’ve seen in U.S.-China trade talks and other tariff rollbacks. That’s why we keep our risk-on stance and an overweight to U.S. stocks on a tactical six- to 12- month horizon, supported by mega forces like AI. The S&P 500 is back near its February record high as trade tensions cool, LSEG data show. We brace for more policy-driven volatility as the U.S. floats plans for setting tariffs unilaterally before the 90-day pause ends on July 9.

Challenges for central banks

We see uncertainty around the economic impact of tariffs and inflation volatility keeping the Fed on hold for now – including at this week’s meeting. Longer term, persistent inflation pressures from tariffs and a tight labor market will likely limit how far the Fed can cut, even if tariff-driven supply disruptions dent growth. We think long-term U.S. bonds yields can rise, keeping us underweight. We prefer inflation-linked bonds, even if they are yet to reflect long-term inflation pressures, in our view. On a strategic horizon of five years and longer, we like private credit as returns for debt with floating interest rates have risen with rates. We favor infrastructure equity, like stakes in airports and data centers: its returns are buffered from inflation and it outperforms amid supply constraints and high inflation. Private markets are complex and not suitable for all investors.

We think tariffs and any sustained oil price rises from the Israel-Iran conflict could leave other central banks facing weaker global growth. Should the conflict affect the security of critical trade routes, supply disruptions could add to inflation pressures. The European Central Bank (ECB) cut rates this month but signaled a pause ahead, even after lowering its 2025 growth projections. Greater fiscal spending could boost growth in time, but execution is key. We think the ECB has more room to cut as wage pressures and energy prices cool, and tariffs likely aren’t inflationary for Europe. We still prefer European to U.S. investment grade and high-yield credit. That preference has served us well, but we keep an eye on relative valuations.

Our bottom line

Volatile economic data, like the CPI, is reinforcing our view that we are in a regime of greater macro volatility. We think the Fed will keep rates steady as it waits for tariff impacts to materialize. Mega forces keep us overweight U.S. stocks.

Market backdrop

Global stocks slid last week after Israel launched a large-scale attack on Iran’s nuclear and missile infrastructure, as well as its military and scientific command. Europe’s Stoxx 600 fell 1.7%, while the S&P 500 and Japan’s Topix index retreated about 0.5%. Crude oil futures surged over 11% last week, briefly hitting a five-month high after news of the attack broke. U.S. 10-year Treasury yields slid about 10 basis points over the week to 4.41% but remain 50 basis points above their April lows.

All eyes are on global central bank meetings this week – but we don’t expect any policy rate changes. We think tariff uncertainty and inflation pressures from labor supply constraints will keep the Federal Reserve on hold. We are watching for comments from the Bank of England on the weak growth outlook. And any escalation in the Middle East will be key to track as potential disruptions to energy supplies or infrastructure could have a bigger market impact.

Week Ahead

June 17 : Bank of Japan policy decision

June 18 : Federal Reserve policy decision; UK CPI

June 19 : Bank of England policy decision

June 20 : Japan CPI

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 16th June, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.