Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Vivek Paul – Global Head of Portfolio Research and Raffaele Savi – Head of Systematic, all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Alpha abounds : U.S. tariffs may drive more dispersion in market and security returns, creating yet more opportunity to earn alpha. We stay risk on and overweight U.S. equities.

Market backdrop : U.S. stocks ticked down and European stocks rose 1% last week after the U.S. tariff pause was extended. U.S. 10-year Treasury yields edged higher.

Week ahead : We’re eyeing global inflation data this week. We see early signs of tariff impacts in some parts of U.S. CPI but watch for more price hikes as inventories run out.

.

The muted market reaction to last week’s extension of the U.S. tariff pause shows what we’ve long argued: immutable economic laws limit how fast the world can change. We stay overweight U.S. stocks, but don’t rule out more sharp near-term market moves. Uncertainty on who will bear tariff costs means yet more dispersion in returns – and more opportunity to earn alpha, or above-benchmark returns. Two ways to do so: dynamically managing macro risk and taking security-specific risk.

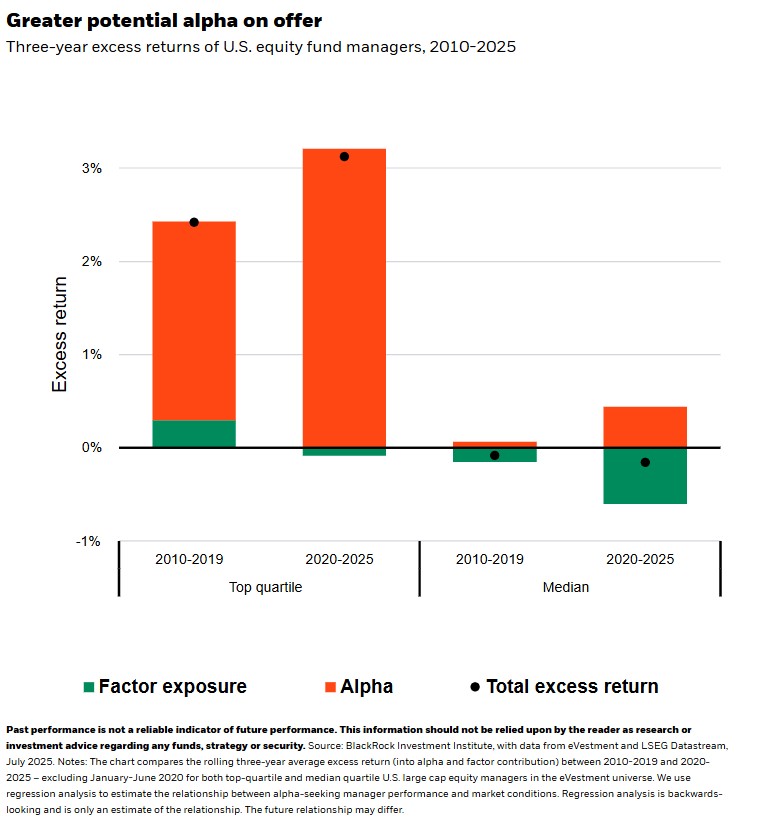

We’ve long said that immutable economic laws – like supply chains can’t be rewired fast without major disruption – will prevent U.S. tariffs rising back to April 2 levels. The extension of the tariff pause to August supports that thesis. Yet wherever tariffs land, it’s not yet clear who will bear the cost: companies, consumers or exporters. That uncertainty will heighten already elevated dispersion. Before the pandemic, when the macro environment was more stable, persistent factor exposures – such as to growth, value or inflation – typically didn’t hurt portfolios. That’s no longer so. For investors, we think this requires watching for unintended static factor exposures and deploying active strategies to capture the additional alpha on offer. Since 2020, top-performing portfolio managers have delivered more alpha. For median managers, static factor exposures now drag more on returns. See the chart.

One way to capture that alpha? Reduce the potential drag from static factor exposures by deliberately managing macro risk. That requires assessing the current macro environment. If your assessment of it changes, it means pivoting quickly. And if it hasn’t changed, it means looking through the noise and leaning against sharp market swings – a particularly rewarding strategy this year, as macro fundamentals are little changed so far. In both cases, it is about being decisive about whether to “stick or twist” with current allocations. Our approach now is to “stick.” Though the joint drop in U.S. stocks, bonds and the dollar in April spurred questions about the long-term appeal of U.S. assets, we think the current economic setup still supports U.S. outperformance. We’ve seen volatility in markets, but it hasn’t shown up in U.S. earnings. That consistency still counts.

Taking security-specific risk

Another approach to capturing alpha: avoiding macro factor risk in favor of security-specific risk. We see the AI mega force continuing to power U.S. earnings growth – yet think some sectors and companies within that theme are positioned to perform better than others. After ChatGPT emerged, virtually any stock aligned with the AI theme got a boost – but now, we’re seeing outperformance concentrated among an increasingly small group of companies. The “Magnificent Seven” of mostly big tech companies are expected to post 14.8% growth in the second quarter, versus just 1.9% for other S&P 500 companies. And even within the Mag 7, we’re starting to see increased dispersion as certain companies capture the greatest benefits from the AI buildout (the race to build the infrastructure it needs) while others lead the way on AI adoption (with AI packaged into different apps and software). This creates alpha opportunities for those with insight into potential winners.

More broadly, we believe these mega forces are transforming the global economy. But no one yet knows the end state of that transformation. So, it will be key to quickly adapt portfolios – on both the tactical and longer-term, strategic horizon – as we learn more about that future world. Based on what we know now, and applying a granular lens, we like EU and U.S. financials, EU and U.S. industrials as domestic production and defense spending increase and U.S. healthcare given population aging.

Our bottom line

U.S. tariffs could intensify already elevated dispersion, making this a more rewarding environment for alpha. Dynamically managing macro risk and taking security-specific risk can help capture it. We eye selective global opportunities.

Market backdrop

The S&P 500 ticked down last week. Tech stocks and U.S.-EU trade deal hopes had briefly driven the index to new highs even after the U.S. tariff pause extension. Europe’s Stoxx 600 rose over 1%, near three-month highs. U.S. 10-year Treasury yields ticked up to 4.42% after easing earlier in the week due to a strong bond auction. We’re watching the market’s ability to absorb heavy bond supply, as the U.S. “Big Beautiful Bill” could widen fiscal deficits and trade tensions could cool foreign demand.

This week, we’re watching inflation data across the world, focusing on the U.S. Core CPI rose slightly less than expected in May but showed some signs of tariffs feeding through to some consumer prices, like in appliances. We believe most of the impact is yet to come and will build up after companies run through the inventories they imported before tariffs were set.

Week Ahead

July 14 : China trade balance

July 15 : U.S. CPI; China GDP

July 16 : UK CPI

July 18 : Japan CPI

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 14th July, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.