Wei Li – Global Chief Investment Strategist of BlackRock Investment Institute together with Ben Powell – Chief Investment Strategist for the Middle East and APAC, Axel Christensen – Chief Investment Strategist for Latin America and Serena Jiang – Economist, all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Japanese stocks still favored : Solid growth and ongoing shareholder-friendly reforms are driving Japanese equity gains, keeping us overweight. We see the AI theme playing out globally.

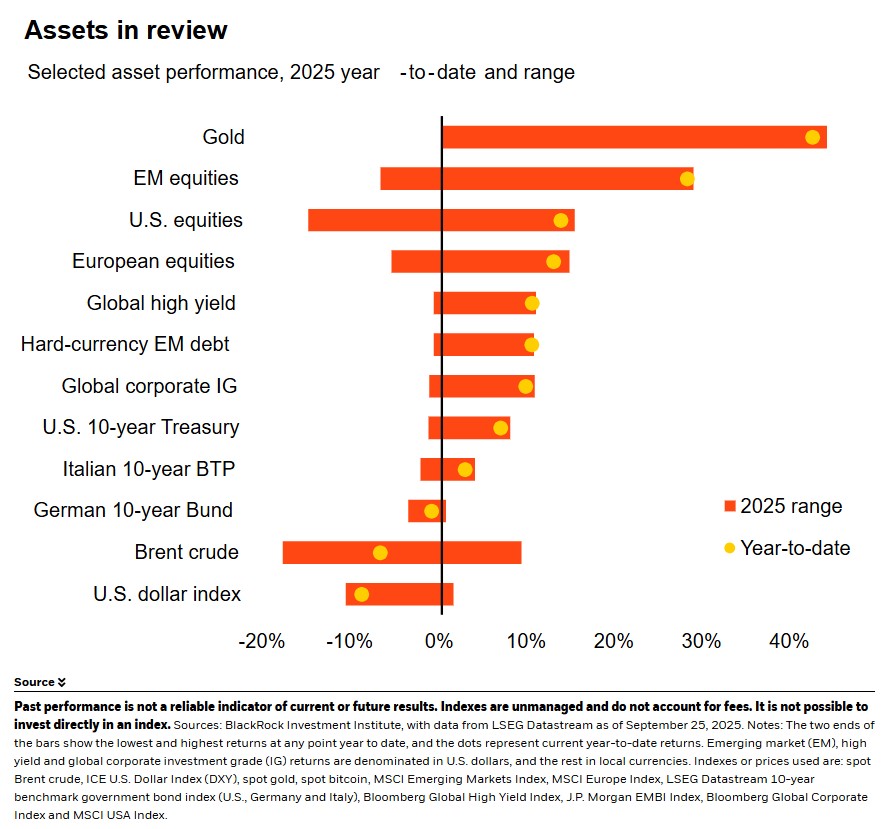

Market backdrop : U.S. stocks hovered near all-time highs, while Japanese stocks pushed to new highs. Emerging market stocks are still among the best performers this year.

Week ahead : We’re watching the U.S. jobs data. We think the labor market would need to weaken far more for the Federal Reserve to deliver market pricing of rate cuts.

The Bank of Japan this month showed its gradual policy normalization is pushing ahead while avoiding the volatility it sparked last year. Japanese stocks are still one of our favorites. Japan’s corporate governance reforms are translating into tangible shareholder gains: improved performance and rising share buybacks. We stay overweight Japanese equities. Recent AI investment developments also reinforce why a mega force lens is key for spotting return opportunities.

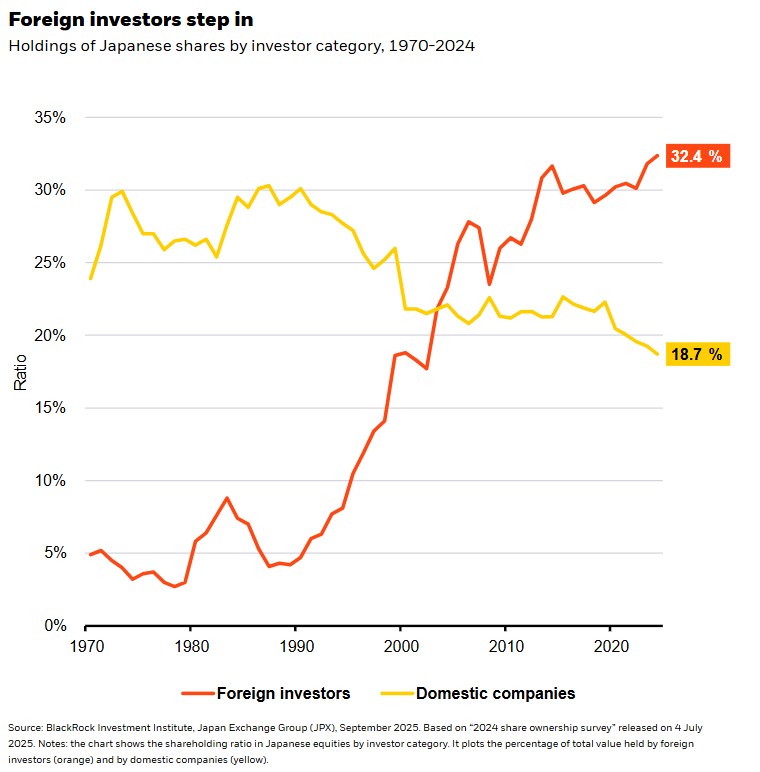

Corporate reform is delivering measurable results for shareholders in Japan. The chart shows the steady decline in corporate cross-shareholdings — once used by Japanese companies to cement ties with peers, but a practice that discouraged outside investors or allowed companies to resist pressure to improve performance. These holdings have fallen sharply. See the chart. The upshot? It is opening the market to more genuine ownership and stronger incentives to boost returns. Share buybacks — one of the earliest and clearest signs of reform momentum taking root — have surged as companies respond to rules pushing them to return cash rather than hoard it. In the first eight months of this year, buybacks already nearly equal last year’s total — which itself was more than double the highest annual level in the decade before 2023, according to corporate data compiled by Nomura.

Our long-held preference for Japanese equities over government bonds has delivered this year: the MSCI Japan is up over 14%, while the Japanese government bond index is down over 4%, according to LSEG data. Corporate return on equity (ROE), or profitability, that has long lagged other developed markets is now near its highest level in four decades, LSEG data show, keeping us overweight on both a tactical and strategic horizon. We think ROE gains will increasingly come from small- and mid-cap firms as reforms spread beyond the largest companies. Our positive view on equities is also predicated on the Bank of Japan (BoJ) being mindful of the risks of tightening too much, too soon. Such risks cannot be ruled out, but we think lessons from last year’s yen surge and stock plunge suggest it will walk back if its tightening sparks volatility. The risk of renewed volatility has also diminished, in our view, as yen-funded carry trades have shrunk sharply compared with last year.

Watching for election policy impacts

We expect greater political clarity after the ruling Liberal Democratic Party’s leadership election on Oct. 4. The two leading candidates, Shinjiro Koizumi and Sanae Takaichi, differ on monetary policy — Koizumi supports further Bank of Japan rate hikes while Takaichi favors fewer hikes or even cuts — but both back looser fiscal policy, which could push long-term bond yields higher. Japan’s public debt already exceeds twice the size of its GDP, according to IMF data. With inflation back and interest rates rising, debt servicing costs are climbing, leading investors to demand more compensation to hold government bonds. That reinforces our underweight to Japanese government bonds.

Japan highlights how a country lens still matters for spotting opportunities, yet we increasingly lean on mega forces and the AI theme to find them. We see the AI theme playing out in Japan: AI is central to addressing demographic challenges and builds on the country’s strengths in robotics, automation and semiconductor materials. The AI theme has been an important driver of returns in China, Taiwan and South Korea this year – each developing models or providing key components of the AI buildout. This comes on top of Nvidia’s key investment agreements, showing how the AI theme is still driving U.S. equities.

Our bottom line

Japan’s ongoing reform progress is boosting corporate performance and returns. We stay overweight Japanese equities and underweight bonds. We also see more signs of the AI theme playing out globally that keep us positive.

Market backdrop

U.S. stocks hovered just below record highs, with the S&P 500 up nearly 13% for the year, led by tech shares. Japan’s Topix pushed to a fresh record high with the Topix now up 14% in yen terms. The MSCI Emerging Markets index is up nearly 25% this year in U.S. dollar terms, making it one of the top performing equity indexes this year. U.S. 10-year Treasury yields edged up slightly to 4.18% after the U.S. August PCE data underscored strong consumer spending.

This week, we’re watching jobs data. A slowing in hiring gave the Federal Reserve room to restart rate cuts in September. We anticipate additional cuts this year, but think the labor market would have to weaken far more for the Fed to implement the cuts markets have priced in for 2026. Rates will, in our view, ultimately settle at higher than pre-pandemic levels.

Week Ahead

Oct. 1 : U.S. durable goods

Oct. 2 : Euro area unemployment

Oct. 3 : U.S. employment report; Japan unemployment

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 29th September, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.