Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Rick Rieder – Head of Fundamental Fixed Income and Michel Dilmanian – Portfolio Strategist,all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Fixed income opportunities : Higher-for-longer interest rates offer solid income sources. We favor short- and medium-term government bonds, mortgage-backed securities and select credit.

Market backdrop : U.S. stocks hit fresh record highs last week, helped by strong economic data. U.S. corporate earnings season kicked off with big tech companies reporting.

Week ahead : This week, we watch the European Central Bank policy decision. We expect it will hold rates steady but monitor for signs of potential easing later in the year.

.

Higher-for-longer policy rates have made this the best backdrop for earning income in bonds in two decades – without taking more interest rate or credit risk. We favor a mix of income sources. We like short-term government bonds: the U.S. budget bill passed last month highlighted a lack of fiscal discipline, while sticky inflation limits rate cuts, keeping us tactically cautious on long-term bonds. In credit, resilient growth has kept corporate balance sheets solid even with tariffs.

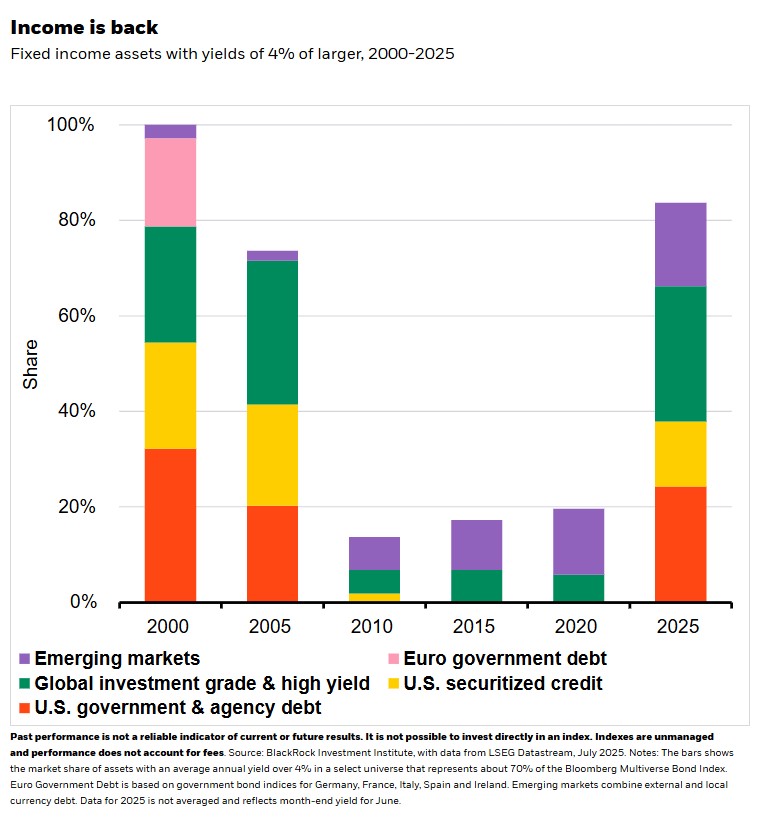

After the global financial crisis (GFC), bond yields slid as central banks slashed policy rates to near zero or below and bought bonds. That left investors starved of income unless they took risk in long-term bonds. In a stark switch-up, some 80% of global fixed income assets now offer yields above 4% as interest rates have settled above pre-pandemic levels. See the chart. That’s made assets like credit, mortgage- backed securities and emerging market debt more attractive. We have seen notable bond market developments this year. Credit spreads have been relatively steady even with sharp equity volatility. And investors are demanding more compensation for the risk of holding long-term bonds, leading to a steepening of global yield curves. The curve between five and 30-year U.S. Treasury yields has more than doubled this year to its steepest levels since 2021, according to LSEG data.

We see abundant opportunities to earn income. We prefer short- and medium-term government bonds given yields near 4%. Markets are pricing in multiple Federal Reserve rate cuts over the next year. Yet we see sticky inflation limiting rate cuts – even as renewed rate hikes are unlikely. Our preference is partly driven by our caution on long-term bonds due to the lack of U.S. fiscal discipline and sticky inflation – though we could see occasional sharp rallies. The U.S. is issuing nearly $500 billion of debt weekly to fund its persistent budget deficits, per Haver Analytics. And the Congressional Budget Office expects the One Big Beautiful Bill to only add to deficits in the near term. Trade tensions could cool foreign demand at a time when sustaining U.S. debt relies on their ongoing buying – as we noted in our 2025 Midyear Outlook. We’re watching the market’s ability to absorb heavy Treasury issuance. Fiscal sustainability is not just a U.S. story: In Japan, 30-year yields hit a record high last week as policymakers floated tax cuts before Sunday’s upper house election.

Where we find income

Higher U.S. policy rates mean interest rate differentials between the U.S. and other countries stay wide, revealing an array of global fixed income opportunities. That’s because hedging foreign bonds back into U.S. dollars boosts the income they offer. Some euro area bonds, like Spain, offer yields above 5% with such hedging – higher than U.S. equivalents. Credit has become a clear choice for quality. Spreads are historically tight, yet credit income remains attractive as balance sheets have held up alongside growth, even with tariff uncertainty. Default rates for U.S. high yield credit remain about half the 25-year average, according to J.P. Morgan data. We prefer European fixed income over the U.S. given a more stable fiscal outlook, especially European bank debt given strong financial earnings and insulation from tariff impacts.

We get selective across and within regions. We went overweight U.S. agency mortgage-backed securities (MBS): spreads are wider than historical averages and we could see some investors switch from long-term Treasuries. We upped local currency emerging market (EM) debt to neutral this month: it has weathered U.S. trade policy shifts, and debt levels have improved.

Our bottom line

We like a mix of income opportunities but stay selective due to fiscal sustainability risks. We favor short- and medium-term government bonds, U.S. agency MBS, currency hedged international bonds and local currency EM debt.

Market backdrop

The S&P 500 hit new record highs last week, helped by signs of U.S. economic resilience in strong U.S. retail sales data. U.S. corporate earnings season kicked off with some big tech companies, putting renewed focus on artificial intelligence and capital spending. The index quickly recovered from reports that U.S. President Donald Trump discussed removing Fed Chair Jerome Powell, which Trump denied. Thirty-year Treasury yields ended the week steady at 4.99%, near May’s two-year high.

This week, we’re watching the European Central Bank’s (ECB) policy decision. We expect it to hold rates steady until September. The central bank now sees policy rates within a neutral range that neither stimulates nor restricts economic activity, inflation remains around its 2% target, and euro area growth shows little change. We watch for signals on whether the ECB will stay cautious or begin laying the groundwork for easing later this year.

Week Ahead

July 23 : Euro area consumer confidence

July 24 : European Central Bank policy decision; global flash PMIs

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 21st July, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.