Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Paul Henderson – Senior Portfolio Strategist and Nicholas Fawcett – Senior Economist all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Tracking AI’s evolution: Recent developments in artificial intelligence (AI) have forced markets to rethink their AI assumptions. We use our three-phase framework to track AI’s progress.

Market backdrop: U.S. stocks were flat last week. Tech shares slid on AI concerns, only to reverse on solid Q4 earnings. U.S. 10-year Treasury yields fell near five-week lows.

Week ahead:This week we watch for any initial disruptions from the U.S. imposing 25% tariffs on Canada and Mexico, as well as a further 10% tariff on China.

Last week’s volatility in AI-related stocks shows markets are learning in real time about the transformation underway. We see having a framework as key for tracking mega forces, or big structural shifts, given a widening range of market outcomes. We use our three-phase framework – buildout, adoption, transformation – to track AI. Recent AI developments raise questions about AI investment and revenue. We see a broadening set of AI beneficiaries and stay overweight U.S. stocks.

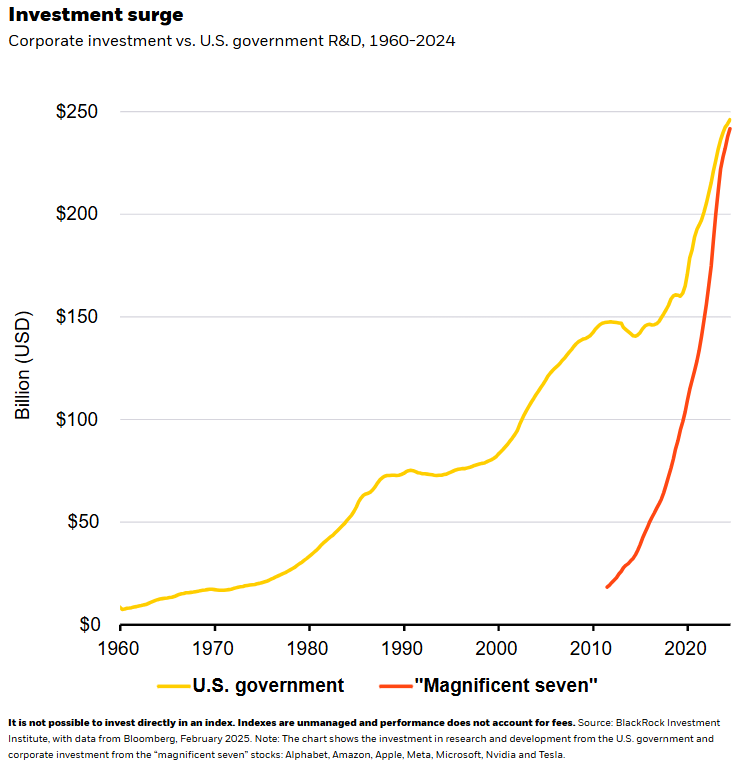

We have said artificial intelligence could reshape economies and markets even as big questions remain about what exactly that will look like – in particular, who will generate the profits. We are in the AI buildout, with total capital investment by the “magnificent seven” mostly mega cap tech stocks on par with government R&D. See the chart. The release of a seemingly more efficient AI model by Chinese startup DeepSeek has renewed questions about AI capex. While these questions are valid, more spending is likely needed to unlock AI innovation – recent developments don’t change our view. Broad AI adoption is still to come, and we have barely scratched the surface of all the potential AI use cases. Yet AI advances mean these models could be evolving faster than expected. That could push AI into the adoption phase sooner and is why the AI narrative and the market’s reaction could change quickly.

We are still in AI’s buildout phase – and even with potential model efficiency gains, big capital spending might still be needed to unlock further innovation, like artificial general intelligence. Strong results and guidance from the magnificent seven show they can support heavy AI capex. Q4 management commentary reveals these companies are comfortable with their AI spend and have long-term conviction in the theme and expect ongoing demand. As the buildout progresses, it opens the door for the set of AI winners to broaden further beyond the magnificent seven, expanding the total AI opportunity set, in our view.

Evolving our views

Beyond the buildout phase, we have yet to see the adoption phase begin in earnest, even with more players in the mix. Yet the rise of new AI models signals we could move through AI’s phases quicker than anticipated, especially if efficiency gains from those models are indeed significant. Efficiency gains could ease earlier market fears that AI capacity won’t keep up with rising demand. The spread of simpler, cheaper AI models could spur wider adoption by companies that need greater transparency over AI’s output. To gauge adoption, we track sectors with a high share of jobs prone to AI-driven efficiency gains. AI’s final phase may bring long-run, economy-wide productivity benefits – but only after AI tools have been built and broadly adopted.

We believe AI will generate significant revenue streams, yet how those revenues will be sliced up is the big question to track. One possible outcome: the big tech players now powering the AI buildout could reap most of the benefits. Yet last week’s developments show there is another path: cheap, efficient and commoditized AI models that could benefit AI’s end users instead of big tech. Across all three phases, following the revenue helps us to uncover investment opportunities.

AI is at the center of the U.S.-China strategic competition. The U.S. strategy has been to protect and extend its AI lead, in part by denying China access to advanced tech and hardware. DeepSeek’s apparent breakthrough has raised questions for some about the effectiveness of this approach. The new administration has emphasized AI leadership is key for U.S. economic and national security. We expect a continued focus on export controls, data security and concentrating the AI buildout in the U.S.

Our bottom line

We keep our broad U.S. equity overweight. The emergence of new AI models shows the AI transformation could be accelerating, in our view. Across AI’s three phases, we track revenue generation for identifying AI investment opportunities.

Market backdrop

U.S. stocks were flat last week. Tech shares slid, led by Nvidia, on concerns about whether the AI buildout was overdone – only to reverse on solid Q4 mega cap tech earnings, leaving the Nasdaq little changed on the week. U.S. 10-year Treasury yields fell to around 4.51%, near five-week lows. The Federal Reserve opted to hold rates steady at last week’s policy meeting, while the European Central Bank cut rates 25 basis points – both moves widely expected.

Markets will focus on any disruptions resulting from the U.S. imposing 25% tariffs on Canada and Mexico (10% for Canadian oil), and an extra 10% tariff on Chinese goods, all due to be implemented this week. This marks an escalation in trade protectionism, and we think that some level of tariffs is likely to remain in place over time. Uncertainty is high on how the trade dispute will play out on supply chains, growth and inflation. U.S. payrolls are also due this week.

Week Ahead

Feb. 3: Euro area inflation data

Feb. 5: U.S. trade data

Feb. 7: U.S. payrolls; University of Michigan sentiment survey

Feb. 8: China CPI and PPI

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 3rd February, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.