Wei Li – Global Chief Investment Strategist of BlackRock Investment Institute together with Alex Brazier – Deputy Head, Vivek Paul- Head of Portfolio Research and Nicholas Fawcett – Macro Research all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Future of finance: Tectonic shifts in the U.S. financial sector are changing the markets for deposits and credit. This is a mega force we see affecting returns now and in the future.

Market backdrop: U.S. stocks hit five-month lows and 10-year Treasury yields rose above 5% last week. Q3 GDP was stronger than expected, but we don’t see that continuing.

Week ahead: The Federal Reserve takes center stage this week. We see the Fed holding policy tight as an aging population constrains the workforce and fuels wage pressure.

The future of finance is one global mega force we see affecting returns. It includes a changing U.S. corporate funding landscape, with less reliance on bank lending. That long-term trend has been bolstered by higher interest rates: Interest paid on bank deposits has lagged rate hikes, igniting competition for deposits. These shifts are good for savers, we believe. A more diversified funding pool makes the financial system safer and benefits borrowers overall, even if it means higher funding costs.

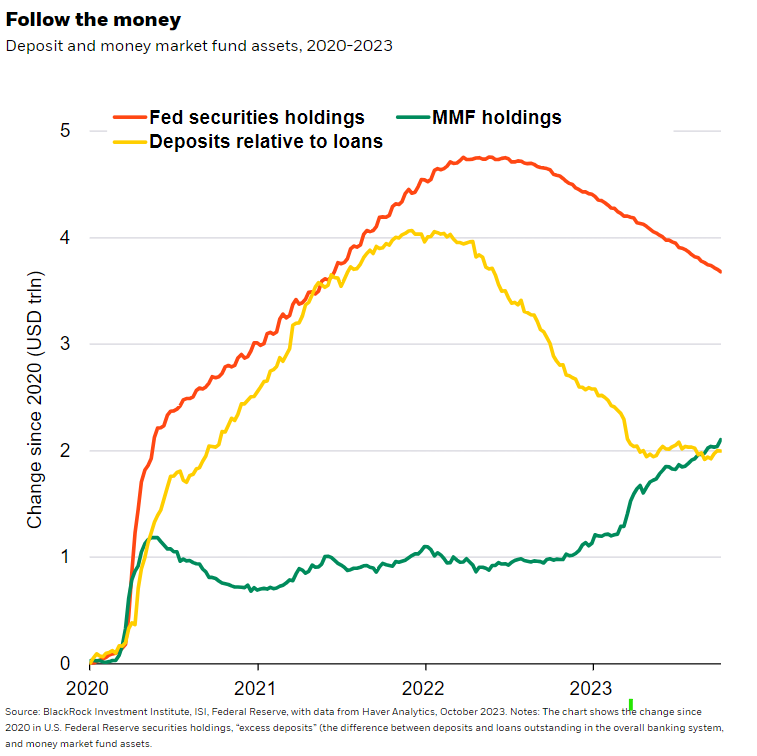

Higher interest rates are a key tenet of the new regime of greater macro and market volatility, in our view. The end of zero interest rates has brought back competition for bank deposits. The interest rate U.S. banks pay on deposits has lagged Fed rate hikes since 2022. By contrast, other parts of the financial system, such as U.S. money market funds, have quickly offered higher rates. Savers have moved cash from banks to money market funds as a result: The Fed has injected $4 trillion into the economy since 2020 (orange line in chart), yet the banking system only has an additional $2 trillion of deposits over and above the loans it has made (yellow line) – still a comfortable buffer for now, but likely to run down as the Fed’s quantitative tightening progresses. The rest is in rising U.S. money market fund holdings (green line). We think higher rates are here to stay as the Fed keeps policy tight to fight inflation – likely to be confirmed at the Fed’s policy meeting on Wednesday.

The flight of deposits from banks sped up after the collapse of three U.S. regional banks in March, but this shift was already in motion. With more competition, banks can no longer cheaply fund loans by paying depositors rates well below the Fed policy rate as that would mean losing more depositors. We expect to see U.S. banks paying higher interest rates to savers as a result. Smaller banks have already started doing that this year. That, in turn, likely means higher interest rates on bank loans, which could crimp demand. Banks could choose not to pass on the extra cost of their deposits to borrowers. That would hurt their profit margins and reduce the profitability of lending, potentially discouraging them from lending as much. We see banks consolidating to reduce the need to support loans on their balance sheets. Overall, we expect a reduction in lending activity on bank balance sheets. U.S. regulatory proposals – partly in response to the U.S. bank turmoil – could reinforce the process.

The combined pressure on bank profitability from lending less and paying higher deposit rates is already visible in the net interest margins of small banks. They have fallen by more than those of large banks this year, according to September 2023 data from the Federal Deposit Insurance Corp. Small to mid-sized banks are also feeling more earnings pressure, with Q3 results reported so far showing declines versus both last quarter and last year. Bigger banks are holding up better so far.

Non-banks stepping in

The higher rate regime is catalyzing longer-run changes in the U.S. financial landscape – like the expanding role of non-bank credit providers. Bank loans now account for around one-fifth of non-financial corporate borrowing, according to Fed data. That is about half their share in the early 1970s. We think companies will keep diversifying their funding towards non-bank sources. Take private credit: It could appeal to small to mid-sized firms who face high barriers of entry to accessing public markets. Private credit lending spreads have widened over the past 12-18 months, and we find them attractive. Plus, private credit loans tend to have floating interest rates, insulating their returns from being eroded by higher policy rates. We are overweight on a strategic horizon of five years and beyond. But private markets are complex and not suitable for all investors. We think private credit requires selectivity and a focus on how much of the opportunity and risks are already in the price.

Bottom line

Greater diversification is good for borrowers, higher rates benefit savers, and such shifts create a more stable system – even as financing costs rise, in our view. Savers are benefiting from the higher returns in U.S. money market funds and regulatory reforms that made them more resilient. The higher interest rate environment has also broadened the potential ways of making income in the new regime. We see investment opportunities in alternative funding sources like private credit.

Market backdrop

U.S. stocks hit five-month lows and 10-year Treasury yields reached 16-year highs above 5%. Tech stocks underperformed on some disappointing earnings, while regional bank shares broadly hit new lows for the year. U.S. core PCE data, the Fed’s preferred inflation gauge, slowed further in September on falling goods prices. Strong consumer spending drove a stronger-than-expected rise in Q3 GDP. Yet we don’t see that as sustainable as consumers exhaust their savings.

The Fed takes center stage this week. We see the Fed holding policy tight as inflationary pressures persist, with an aging workforces keeping the labor market tight. U.S. payrolls are also in focus. We think the demographic shift in the labor force means the economy will soon only be able to sustain a fraction of recent job growth without stoking further wage pressure.

Week Ahead

Oct. 31: U.S. consumer confidence; Euro area inflation, Q3 GDP; Bank of Japan policy decision

Nov. 1: Fed policy decision

Nov. 2: Bank of England policy decision

Nov. 3: U.S. payrolls report; Euro area unemployment

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 30th October, 2023 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.