Wei Li – Global Chief Investment Strategist of BlackRock Investment Institute together with Beata Harasim – Senior Investment Strategist, Tom Walsh – Head of U.S. Credit, Fundamental Fixed Income, and Devan Nathwani – Portfolio Strategist forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Finding yield: Total income has returned to credit thanks to higher-for-longer interest rates. We prefer pockets of credit where investors are better compensated for risk.

Market backdrop: U.S. stocks ticked up to fresh all-time highs last week. U.S. PCE for May was flat month over month, the latest measure showing decelerating price growth.

Week ahead: We’re monitoring this week’s U.S. payrolls data to see if rapid job gains will continue and if wage pressures remain elevated.

The higher-for-longer rate environment has restored income in a range of different bonds. Total yields on offer in credit – in investment grade, mortgage-backed securities and high yield – provides long-term investors relatively attractive yield returns to risk, especially in shorter-term bonds. We favor areas where investors are more compensated for risk, preferring Europe over the U.S. and private credit over public. From a whole portfolio perspective, we prefer taking risk in equities.

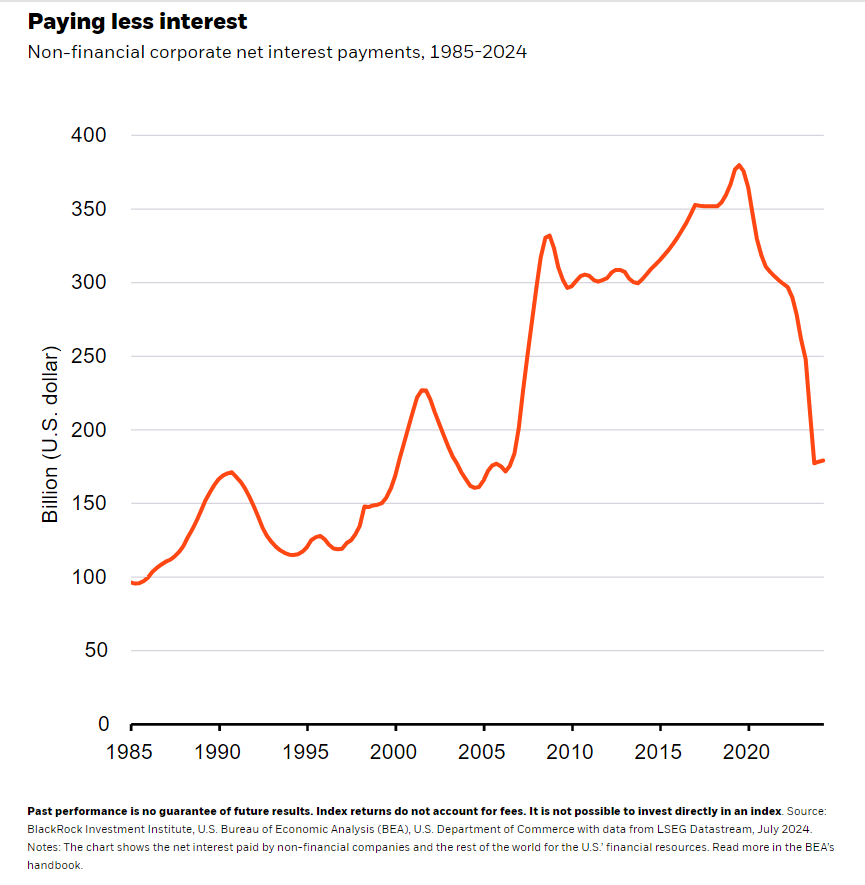

Today is a different world for fixed income investing compared with pre-pandemic. After a historic string of central bank rate hikes, 86% of global fixed income assets are now yielding 4% or more, versus less than 20% in the decade leading up to the pandemic, LSEG Datastream data show. This means long-term investors no longer need to take on extra risk to generate solid income. And U.S. companies are proving resilient to higher rates. U.S. investment grade companies have less than 10% of outstanding debt coming due annually through 2030, Bloomberg data show. We don’t see a maturity wall ahead that could raise questions about companies refinancing at higher rates. Many companies took advantage of low rates early in the pandemic, converting short-term debt to long-term. As a result, U.S. corporate net interest payments have plunged even after sharp rate hikes. See the chart.

While the total income on offer is attractive for fixed income investors, we stay selective in credit. Spreads have tightened, largely a function of strong demand relative to supply and resilient corporate balance sheets. Spreads for U.S. investment grade companies are near their tightest levels in two decades – keeping us underweight. Within credit, we prefer the income from short- and intermediate-term bonds and pockets that compensate investors for risk-taking. We are neutral high yield credit globally on both a tactical and strategic horizon. The income cushion makes high yield more attractive on a total return basis relative to investment grade, in our view. We get granular by region, preferring European longer-term credit over the U.S. – spreads in Europe are not as tight relative to the U.S. or to their own history. We are keeping an eye on the French parliamentary election heading into the second-round vote on July 7. France makes up almost 20% of the European corporate bond universe, Bloomberg data show.

Sticking with equities tactically

In a whole portfolio context, we prefer taking risk in equities – where expected returns are more attractive – over credit on a tactical horizon of six to 12 months. We stay overweight stocks and the AI theme.

On strategic horizons of five years and longer, we like private credit over public – even as U.S. direct lending default rates have risen, according to Lincoln International data. Defaults could be even higher if not for lender flexibility on companies breaching credit agreements. This factors into our conservative default assumptions for private credit – twice those of public high yield. Yet even after accounting for those potential losses, we remain positive. Defaults are still relatively limited. Private credit should also play a key role in the future of finance: We see rising appetite for non-bank lending driving steady demand for private credit. Private markets are complex, with high risk and volatility, and aren’t suitable for all investors.

Bottom line

The fastest rate hikes in decades have put total income back into fixed income. We like pockets of credit where investors are more compensated for risk – like Europe over U.S., high yield over investment grade and private over public. Yet in a whole portfolio context, we prefer taking risk in equities.

Market backdrop

U.S. stocks rose to fresh all-time highs last week. U.S. PCE for May was flat monthly as expected, the latest inflation measure showing decelerating price growth. We watch for whether inflation ultimately cools enough to settle near the Fed’s 2% goal. French assets came under pressure heading into the first round of the snap election. Spreads on French 10-year government bonds over German bunds pushed back to their widest level since the euro area crisis. French stocks hit five-month lows.

We’re keeping an eye on the U.S. payroll report out this week to gauge if recent rapid job gains will continue, boosted by bumper immigration flows. We’re also watching whether pay growth remains elevated: It’s currently running too hot for inflation to settle near the Fed’s 2% target, in our view.

Week Ahead

July 2: Euro area flash inflation and unemployment data

July 3: U.S. trade data; Caixin services PMI

July 5: U.S. payrolls data

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 2nd July, 2024 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.