Jean Bovin – Head of BlackRock investment institute, together with Wei Li – Global Chief Investment Strategist, Alex Brazier – Deputy Head, Ben Powell – Chief Investment Strategist for APAC, and Vivek Paul – Head of Portfolio Research all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Positive developments: China’s reopening, lower energy prices and cooling inflation reinforce our long-term positive view on equities. Yet we think market optimism has come too soon.

Market backdrop: Stocks paused their rally and bond yields steadied after recession worries returned. We think we are starting to see damage from policy overtightening.

Week ahead: We’re watching global flash PMIs this week for signs of recession and look to the U.S. PCE report to see how services spending is affecting core inflation.

Markets have leapt ahead this year, driven by China’s reopening, falling energy prices and slowing inflation. This has spurred hopes of a soft economic landing, plummeting inflation and interest rate cuts. We see markets vulnerable to negative surprises – and unprepared for recession. This is why we underweight developed market (DM) stocks in the near term. Yet the developments reinforce our long-term views and the importance of an investor’s time horizon.

Horizon matters

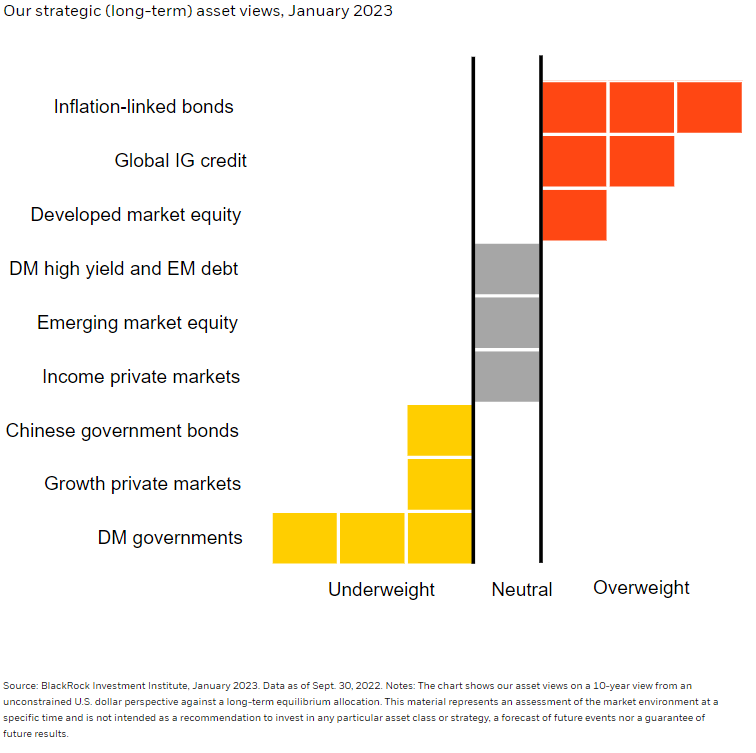

An investor’s time horizon is key when gauging how 2023 developments so far affect investments. These events have upped our confidence in our strategic views on a horizon of five years and more. Economic risks like a closed China and ultra-high inflation have lessened, further underpinning our strategic overweight of stocks, as the chart shows. Equity valuations look reasonable versus our long-term expectations. The stock rally hints at how markets will likely react once inflation eases and rate hikes pause, buoying prospects for long-term corporate earnings. Yet before this outlook becomes reality, we see DM stocks falling when recessions we expect manifest. We think the U.S. economy’s 2023 calendar year growth will then be positive. Investors with a longer-term investment horizon can position for the rebound now but could see more pain to come in the near term.

We may turn more positive on stocks when the damage we see ahead is priced or our assessment of market risk sentiment shifts. For now, the fading risks after this year’s positive developments are key to our strategic views. Case in point: inflation. We have always expected it to fall as pandemic drivers – like consumer spending’s shift from services to goods – reversed. What’s key is our view of U.S. inflation landing closer to 3% than the Federal Reserve’s 2% target. Markets aren’t pricing that in. Plus, longer-term trends like aging demographics, geopolitical fragmentation and the energy transition mean inflationary pressures will be higher than in the past. Treasury yields are falling further away from where we think they’ll climb to in the long term as investors demand more term premium, or compensation for the risk of holding them amid persistent inflation and heavy debt loads. We don’t think nominal sovereign bonds can diversify portfolios anymore, and our preference for inflation-linked bonds is stronger given 2023 events. We see stock returns offering more compensation for risk than bonds

Near-term risks

Yet investors with shorter investment horizons should be wary, in our view. Falling inflation has raised market hopes for rate cuts this year but that optimism may be built on shaky ground. We don’t see rate cuts even once recessions hit. The reason: Central banks are deliberately causing them to try to push inflation down to a tolerable level, we believe. We see them keeping rates higher for longer as a result. We think recessions are more likely in developed economies given the lagged effect of rate hikes. China’s reopening could support global growth. We see China’s economic growth above 6% in 2023 despite its shrinking trade activity. But this cushioning of global growth would temper DM central banks’ efforts to crush economic activity to try to get inflation down to target, in our view. DM recessions should be the key focus tactically. Yet markets don’t appear to price in that outcome. We think that makes them vulnerable to more negative surprises – and volatility – in 2023.

Our bottom line

Time horizons matter – a lot. We’re strategically overweight DM stocks because we think downside risks have lessened, boosting potential long-term returns. Yet we see near-term risks tilted against DM stocks, with earnings growth forecasts not fully reflecting the recessions ahead. So we’re underweight tactically and prefer emerging market equities. We like public equities over private growth assets and expect entry points to grow more attractive. We’re underweight long-term government bonds tactically and strategically as we expect fewer diversification benefits and a rise in yields. Our expectation for persistent inflation is why we like inflation-linked bonds on both horizons. We like high-quality credit for income in both short- and long-term allocations. Look out for a quarterly update to our strategic views soon.

Market backdrop

Global stocks paused from their rally this year and government bond yields steadied from their drop. Surprisingly weak U.S. retail sales and industrial production revived concerns about recession. Still, Federal Reserve and European Central Bank officials made the case for further rate hikes. We think investors betting on Fed rate cuts later in the year are likely to be disappointed – even as a recession is foretold and we start to see more economic damage from their policy overtightening.

We’re looking at flash PMIs for signs of recession in the U.S. and Europe. We will also be watching the U.S. PCE report for more signs of the spending shift back to services from goods and how that is affecting the Fed’s favored gauge of core inflation, as well as the overall strength of household spending.

Week Ahead

Jan. 24: Global flash PMIs

Jan. 25: Germany Ifo survey

Jan. 26: U.S. Q4 GDP

Jan. 27: U.S. PCE inflation and consumer spending

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 23rd January, 2023 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.