Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, David Giordano – Global Head of Climate Infrastructure, and Christian Olinger – Portfolio Strategist all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Infrastructure at the fore Mega forces are creating major infrastructure needs. We find the most investment opportunities today in places where multiple mega forces intersect.

Market backdrop: U.S. stocks were flat near record highs last week, with strong results from one key AI-related company helping buoy the market. U.S. 10-year yields rose.

Week ahead: We watch April U.S. PCE data this week for any signs that services inflation is easing. We see it running too hot for inflation to fall to the Fed’s 2% target.

Infrastructure sits at the intersection of mega forces – the structural shifts driving returns now and in the future. Take artificial intelligence (AI): AI is driving capital spending partly due to technological competition among countries, and the buildout of power-hungry data centers is now affecting the energy transition, too. We stay overweight the AI theme. The rewiring of supply chains benefits countries like India and Mexico. In private markets, we like infrastructure equity strategically.

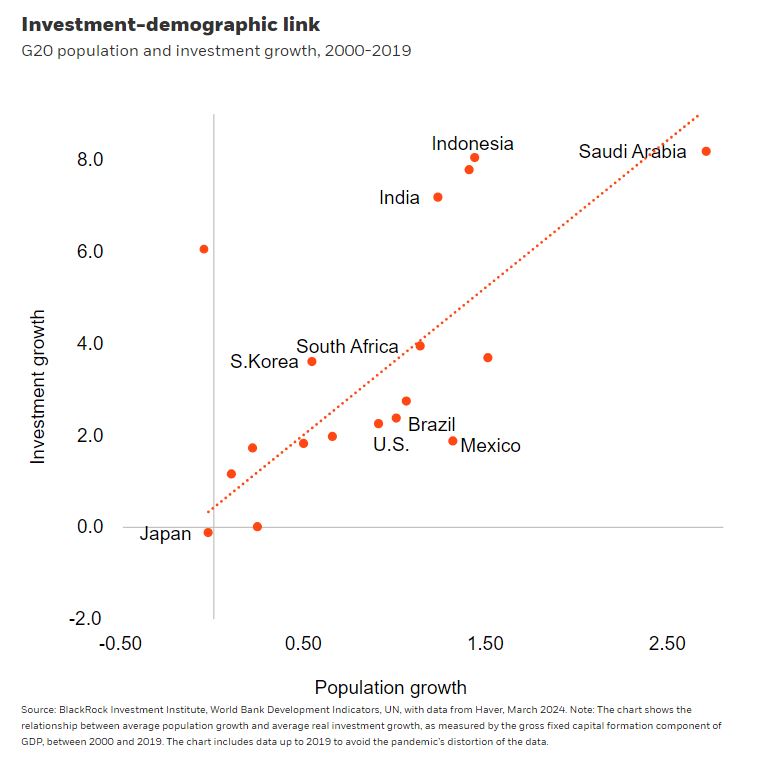

Demographic divergence – a mega force that most investors don’t think about from a capital spending perspective – shapes infrastructure needs across economies. Typically, the faster a population grows, the faster capital investment grows. See the chart. Opportunities arise where investment has not kept up with that growth. Emerging markets (EMs), like Saudi Arabia, will need more capital spending to support their growing working-age populations. In developed markets (DMs), how countries adapt to aging will dictate investment. Many are rolling out measures to help offset stagnating or even shrinking workforces, with countries such as South Korea investing in AI-driven automation. And infrastructure demand could shift away from industries tied to a growing population. We eye potential mispricings as markets can fail to price in even predictable structural shifts – until they hit.

Digital disruption and AI are already creating a massive and immediate need for power and data center infrastructure. AI-related data center investment could grow 60-100% annually in coming years, according to a mix of forecasters including the International Energy Agency. We don’t think broad valuations fully reflect this boom. The investment implications of this buildout extend beyond first-line tech companies – reaching beneficiaries further up the supply chain like utilities, energy, materials, industrial equipment and real estate, as well as those adopting the tech. We are overweight the AI theme broadly.

AI’s energy needs could magnify the already massive investment expected in the low-carbon transition. Many mega-cap tech firms doing the largest AI buildouts have net-zero targets – that could drive up demand for renewable energy. Our BlackRock Investment Institute Transition Scenario estimates energy system investment will hit $3.5 trillion per year this decade – and $4.5 trillion by the 2040s. Low-carbon investment would then account for up to 80% of energy spending, up from 60% now.

The geopolitical story

Geopolitical fragmentation is powering infrastructure demand across sectors and countries. Supply chains are becoming more complex as some countries increasingly act as intermediate trading partners. We get granular in EMs, preferring India and Mexico as they benefit from a rewiring of supply chains or companies bringing production closer to home.

We think private markets play an important role in the new regime marked by greater macro uncertainty and higher inflation. We see them bridging the gap between infrastructure needs and what governments can do on their own, given elevated debt levels in many countries coming out of the pandemic. We are overweight infrastructure equity on a strategic horizon of five years and longer. Compared with other pockets of private markets, infrastructure equity has reasonable valuations at higher interest rates, features steady earnings and offers cash flows often linked to inflation in what we expect will be a world of persistently higher inflation. Private markets are complex, with high risk and volatility, and aren’t suitable for all investors.

Our bottom line

Infrastructure sits at the intersection of mega forces. We stay overweight the AI theme, including beneficiaries of the infrastructure boom on a tactical horizon of six to 12 months. We like infrastructure equity on a strategic horizon.

Market backdrop

U.S. stocks were flat last week near record highs, with upbeat Q1 earnings for one key AI-related company supporting equities. We keep our overweight to the AI theme. Stock market volatility is easing, with the VIX index of S&P 500 implied volatility hitting its lowest levels since 2019. U.S. 10-year Treasury yields ticked up to near 4.45% on a stronger-than-expected services PMI and a drop in weekly jobless claims – but are still down about 30 basis points from this year’s highs.

The release of April U.S. PCE data – the Federal Reserve’s preferred measure of inflation – is the main data event this week. We monitor the data for any signs that services inflation is easing. The U.S. CPI data for April showed core goods prices falling further, so recent upside surprises on the PCE measure may be one-offs. Yet services inflation is proving volatile and remains well above a pace consistent with inflation settling at the Fed’s 2% target in the medium term.

Week Ahead

May 28: U.S. consumer confidence survey; Japan service PPI

May 30: Euro area unemployment data

May 31: U.S. PCE; euro area flash inflation data; China NBS manufacturing PMI

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 20th May, 2024 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.